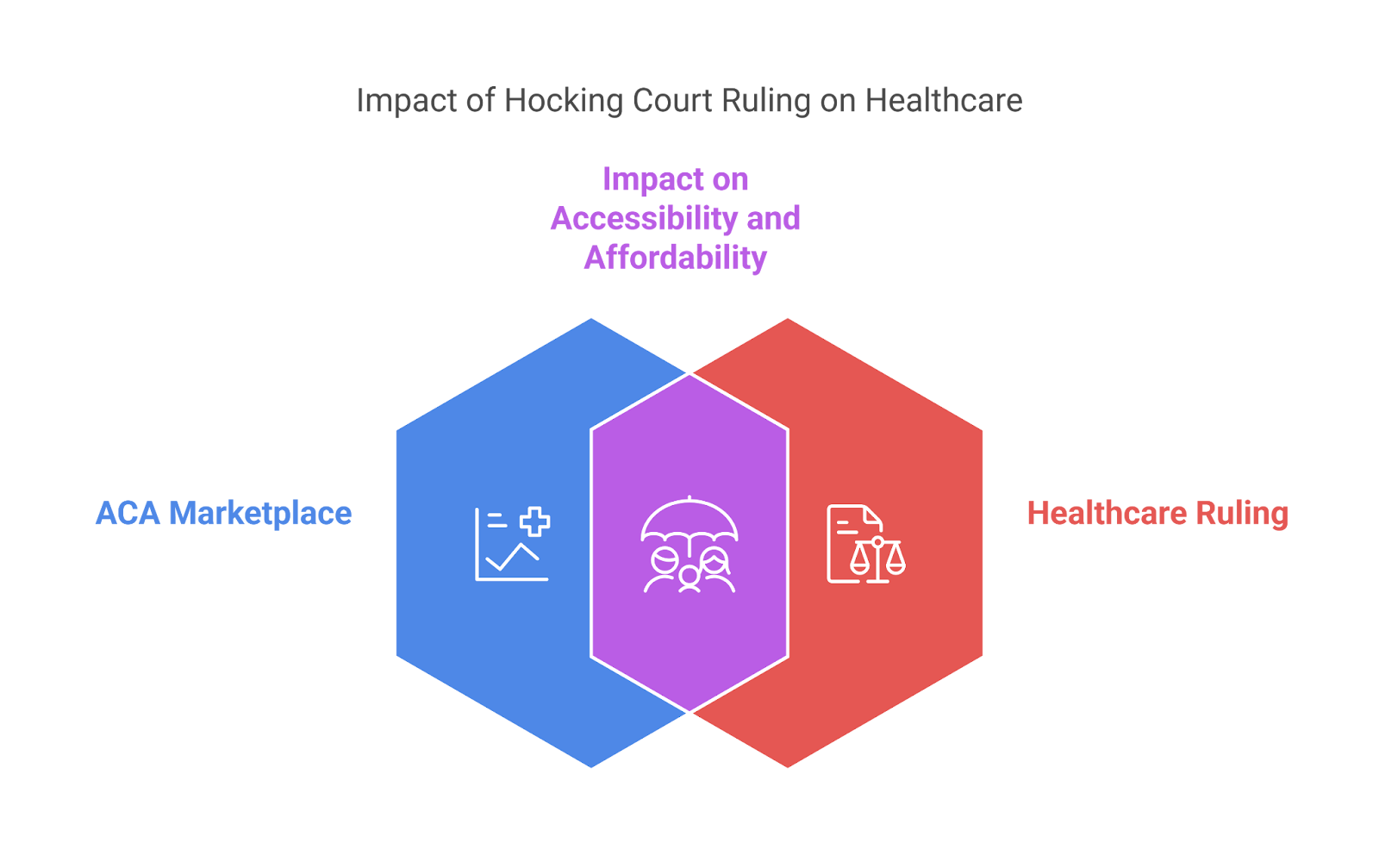

The Affordable Care Act (ACA) has significantly transformed health insurance in the United States, striving to make affordable health coverage accessible to millions. As of January 2025, the ACA Marketplace has witnessed record-breaking enrollment numbers, with nearly 24 million consumers selecting health plans for the 2025 coverage year. This surge underscores the critical role of the Marketplace in providing affordable health coverage to individuals and families nationwide.

Court Decisions on Nondiscrimination

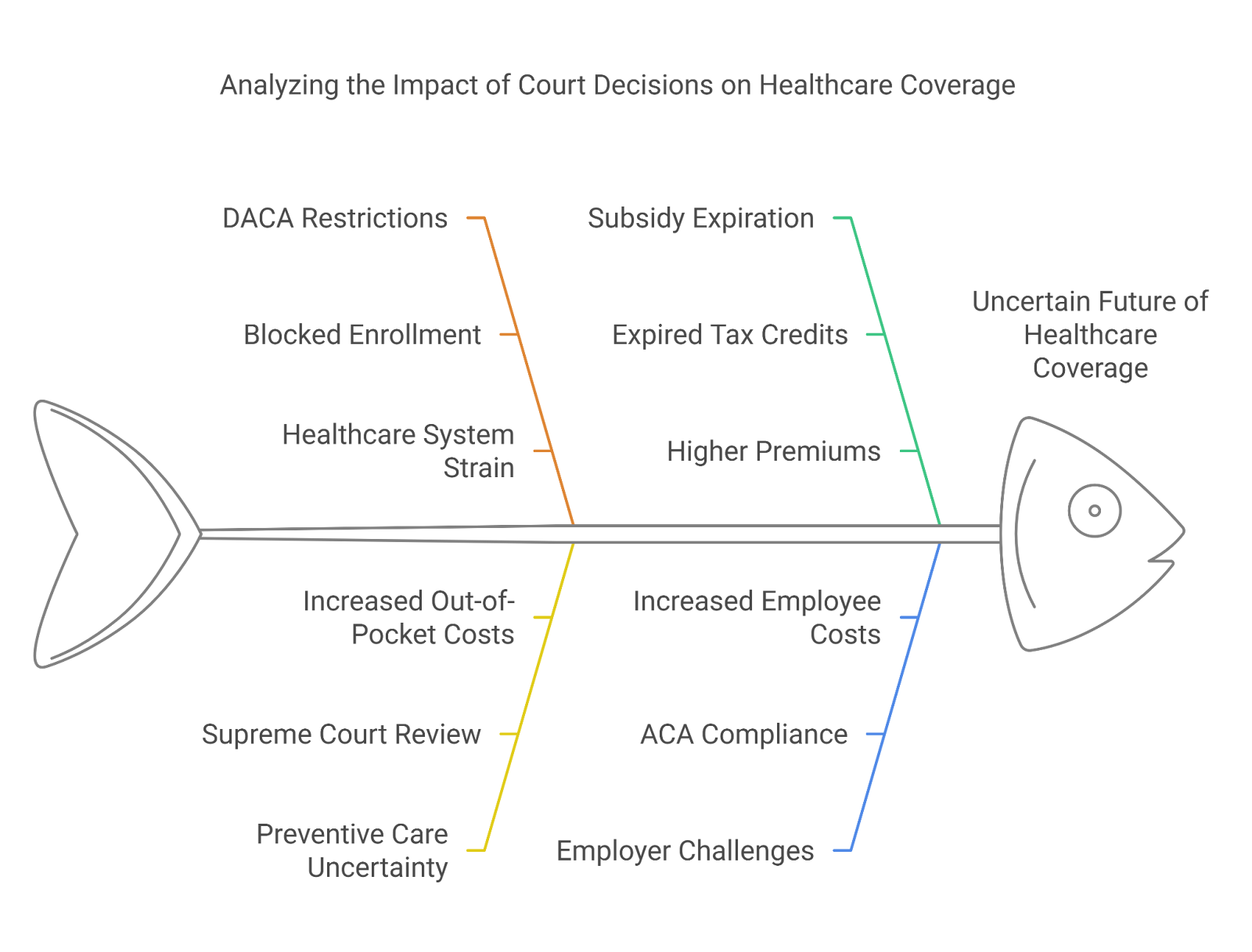

Recent legal developments have impacted the ACA’s nondiscrimination policies, particularly concerning Deferred Action for Childhood Arrivals (DACA) recipients. On December 9, 2024, the U.S. District Court for the District of North Dakota issued a preliminary injunction in Kansas v. United States of America, partially blocking the implementation of a rule that allowed DACA recipients to enroll in qualified health plans through the Health Insurance Marketplace. This injunction affects 19 states involved in the lawsuit, temporarily preventing DACA recipients in these states from accessing Marketplace coverage.

Additionally, the Supreme Court has agreed to review cases challenging the ACA’s preventive services mandate, which requires insurers to cover certain services, such as cancer screenings and HIV prevention medication, without cost-sharing. Employers have raised religious and procedural objections to this mandate, leading to legal battles that could reshape the scope of preventive healthcare coverage under the ACA.

Current State of Medical Care

The ACA Marketplace continues to offer a variety of health plans, enabling consumers to select options that best suit their medical needs and financial situations. The availability of new medical plans has expanded, providing comprehensive coverage with several key benefits:

Affordability and Tax Credits

Enhanced premium tax credits remain in place through 2025, making Marketplace plans more affordable.

About four out of five consumers on HealthCare.gov can find plans for $10 or less per month after financial assistance.

Essential Health Benefits

All ACA-compliant plans must cover 10 essential health benefits, including:

Preventive care (annual check-ups, vaccinations, cancer screenings)

Prescription drugs

Mental health and substance abuse services

Maternity and newborn care

Emergency services and hospitalizations

New Coverage Options

The introduction of new medical plans includes expanded telehealth services and lower-cost generic prescription options.

More insurers are offering high-deductible health plans (HDHPs) paired with Health Savings Accounts (HSAs) to give consumers greater flexibility.

Rising Enrollment Numbers

The 2025 Open Enrollment Period has seen record-breaking participation, with nearly 24 million Americans selecting health plans.

More rural areas and underserved populations are accessing ACA Marketplace plans than ever before.

Increased Focus on Preventive Care

With preventive services mandated by the ACA, insurers must cover screenings and wellness visits without cost-sharing.

However, upcoming Supreme Court cases could impact the range of services covered, making legal developments crucial to watch.

Network and Provider Availability

The expansion of new medical plans ensures a wider provider network, but out-of-network coverage remains limited for some enrollees.

Consumers should verify whether their preferred doctors and hospitals are included before selecting a plan.

Previously, DACA recipients were eligible for new medical plans through the ACA Marketplace across all 50 states.

This provided thousands of individuals with affordable health coverage, including preventive care and prescription benefits.

Preventive Services Mandate

Before legal challenges, insurers were required to cover services like cancer screenings, contraception, and HIV prevention medication without cost-sharing.

Millions benefited from free or low-cost early disease detection and management.

Expanded Coverage for Vulnerable Populations

More individuals, including low-income families and gig workers, could enroll in new medical plans with significant premium tax credits.

Federal subsidies played a crucial role in keeping Marketplace insurance costs low.

After Recent Court Decisions

Restrictions on DACA Recipients

As of December 9, 2024, a court injunction has blocked DACA recipients from enrolling in new medical plans in 19 states (Alabama, Arkansas, Florida, Idaho, Indiana, Iowa, Kansas, Kentucky, Missouri, Montana, Nebraska, New Hampshire, North Dakota, Ohio, South Carolina, South Dakota, Tennessee, Texas, and Virginia.).

This ruling affects thousands of individuals who previously relied on ACA coverage for medical care.

Legal Uncertainty Around Preventive Care

The Supreme Court has agreed to review cases that could remove mandatory preventive service coverage, potentially increasing costs for policyholders.

If the ruling changes, individuals may need to pay out-of-pocket for services previously covered at no cost.

Possible Changes to Subsidies and Premiums

The expiration of enhanced premium tax credits in 2025 could increase monthly costs for many enrollees.

If Congress does not extend these benefits, millions may see higher premiums for new medical plans in 2026.

Uncertainty for Employers Offering ACA Plans

Businesses providing ACA-compliant insurance may need to reassess coverage options based on upcoming court rulings.

This could lead to modifications in employer-sponsored benefits and potential cost increases for employees.

What This Means for Consumers

Individuals should stay informed about potential coverage changes due to ongoing court decisions.

Checking Marketplace plan details and ensuring network providers are covered is crucial before enrolling in a new medical plan.

Consumers should anticipate possible premium increases in 2026 if federal subsidies are not renewed.

Organizations like PEO4YOU can help businesses and individuals navigate these changes by offering tailored health insurance solutions.

Adapting to Change: How PEO4YOU Helps You Navigate Healthcare.

Navigating the complexities of health insurance can be daunting, especially with the dynamic nature of healthcare policies and legal decisions. Organizations like PEO4YOU play a vital role in assisting individuals, families, and small businesses in finding suitable health care plans. By offering tailored group health plans that include essential benefits such as preventive care, specialist visits, and prescription coverage, PEO4YOU ensures that clients have access to comprehensive and affordable health coverage. Their expertise as intermediaries between clients and health insurance companies simplifies the process of selecting and enrolling in new medical plans, providing valuable support in an ever-changing healthcare environment.

People find receiving medical bills confusing and frustrating even when they are insured. While many health insurance policyholders expect complete coverage for medical costs their insurance might still result in unexpected bills due to numerous reasons. This section provides insight into typical situations when you receive a medical bill and guidance on how to handle them.

Out-of-Network Providers

When you visit an in-network hospital or clinic they may employ specialists like anesthesiologists and radiologists who are not covered by your network. Your insurance covers just a part of their bill so you must cover the rest of the total cost. Balance billing happens when your healthcare provider bills you for the gap between their overall charges and what your insurance covers.

Example: During surgery at an in-network hospital you find your anesthesiologist is not included in your insurance network. Your insurance covers part of your medical expenses but you will receive another bill for the outstanding balance.

Solution:While the No Surprises Act offers protection from specific out-of-network billing charges you still need to confirm provider network status before non-emergency care.

Insurance Deductibles and Copayments

Within your healthcare insurance plan you’ll find a deductible which represents the portion you pay yourself before insurance starts covering expenses. Many insurance plans require patients to cover a portion of medical expenses via copayments or coinsurance payments even after fulfilling their deductible obligations.

Example: The deductible for your healthcare insurance coverage stands at $1,500. You must pay $1,500 from your pocket for a $2,000 medical bill if you haven’t reached your annual deductible yet with insurance covering the rest according to your plan’s specifics.

Solution: Study your healthcare insurance coverage documents to learn about your deductible amounts as well as your copayments and upper limits for out-of-pocket expenses.

image

Services Not Covered by Your Insurance

Every insurance plan does not provide coverage for all types of medical services. Certain medical procedures as well as treatments and medications need pre-approval from insurance providers before they can be used and might not be covered by standard insurance plans.

Example: A number of health insurance policies exclude alternative treatments including acupuncture and fertility treatments like in-vitro fertilization (IVF) from their coverage. You may need to pay for these services fully if you decide to receive them.

Solution: Check with your insurance provider to find out if your healthcare insurance plan covers the procedure you plan to undergo.

Prior Authorization Was Not Obtained

Healthcare insurance coverage plans often stipulate that pre-authorization must be obtained before they will pay for certain treatments and specialist visits. Your insurance company is likely to reject your claim if your healthcare provider did not get prior approval.

Example: Your doctor orders an MRI for a non-emergency condition without getting prior approval from your insurance company. The denial of your insurance claim leaves you responsible for the entire amount of the bill.

Solution: You should verify if prior authorization is required before scheduling procedures and make sure that this authorization has been received.

Claim Denial or Coding Errors

Healthcare provider documentation shortcomings and billing code mistakes alongside administrative errors often lead to insurance companies denying claims.

Example: Your healthcare insurance coverage rejects payment when a routine lab test receives a coding error that labels it as a more expensive procedure.

Solution: Request an itemized bill regularly and ensure it matches your Explanation of Benefits (EOB) before appealing any claims that were denied.

Who Is Responsible for Medical Bills Not Covered by Insurance?

Different parties become responsible for unpaid medical bills depending on specific circumstances when healthcare insurance coverage does not fully pay charges. This breakdown points out which parties are accountable and provides steps to handle your medical expenses.

The Patient – Primary Responsibility

As the health insurance policyholder you hold the responsibility for settling medical bills not covered by your insurance plan. This includes:

Your medical insurance begins to pay after you pay a certain amount of money called a deductible.

Specific healthcare services such as doctor visits require you to pay a standard fee of $25 as co-payments.

Your portion of healthcare costs shared with your insurance provider is reflected in coinsurance as a percentage.

Non-Covered Services refer to medical treatments and procedures that your healthcare insurance policy does not cover at all.

What You Can Do With Huge Medical Bills Insurance

Check your Explanation of Benefits (EOB) for any errors.

Reach out to your healthcare provider to verify the charges and ask for a detailed bill.

Inquire about available payment plans or financial assistance programs if you need to do so.

The Healthcare Provider – Willing to Negotiate

Healthcare providers including hospitals and doctors may offer reduced charges on bills or establish payment plans for patients. Financial assistance programs exist at many medical providers to help patients who struggle to pay their bills.

Your Employer (If You Have Employer-Sponsored Insurance)

If your job provides healthcare insurance coverage you may find your employer is available to explain benefits details or help resolve disputes and possibly offer extra benefits.

Certain employers provide health reimbursement arrangements (HRAs) to assist their employees with paying medical expenses directly.

Contact the billing department to inquire about available financial aid options or full payment discounts.

Inquire about spreading your payment across multiple installments through a payment plan.

Patients without insurance or those paying their medical bills personally should attempt to negotiate reduced costs.

Contact your HR or benefits department to discuss any denied insurance claims.

Inquire with your employer about available HRA, HSA, or FSA options (tax-advantaged accounts to manage medical expenses).

The Insurance Company – Can Reverse Denied Claims

Insurance companies often reject claims because of coding mistakes or missing documentation as well as wrong eligibility assessments. Many denied claims are successfully appealed.

Government Assistance & Non-Profit Organizations

Submit an appeal when you believe that the denial decision was incorrect.

Ask for claim evaluation while submitting extra supporting documents.

Should your appeal fail to overturn the denial, seek help from your state insurance commissioner.

Government programs including Medicaid and hospital charity programs along with nonprofit financial assistance options may be available to people who face difficulties paying medical bills.

What You Can Do

Find out whether your hospital offers a charity care program.

Research state and federal assistance programs including Medicaid to find possible help.

Non-profit organizations provide necessary support to people dealing with medical debt relief.

Final Thoughts

When you receive a medical bill that your healthcare insurance doesn’t cover remember that you still have multiple options available to you. Examine your bill thoroughly before attempting to negotiate the charges and research assistance programs offered by employers as well as government and non-profit organizations.

Mastering Medical Bills: Navigate Insurance Like a Pro

It’s important to determine the cause behind medical billing after insurance coverage to prevent paying costs you shouldn’t. Understanding your healthcare insurance specifics along with reviewing billing mistakes and payment assistance programs enables you to manage medical costs effectively.

PEO4YOU provides small businesses and individuals with affordable healthcare insurance coverage options by helping them find optimal health plans.

Businesses and employees receive necessary coverage through employer-based and individual health plans from experts who eliminate surprise medical costs. PEO4YOU assists both small business owners who offer health benefits and individuals searching for complete healthcare plans by simplifying the process and connecting them with suitable insurance options.

Choosing the best health insurance plan is a critical decision that directly impacts both your healthcare access and financial security. For individuals and families, the challenge is finding a plan that balances cost, coverage, and flexibility. Understanding the key elements of the best health insurance and following a structured selection process can help you make the most informed choice.

Understanding the Basics of Health Insurance

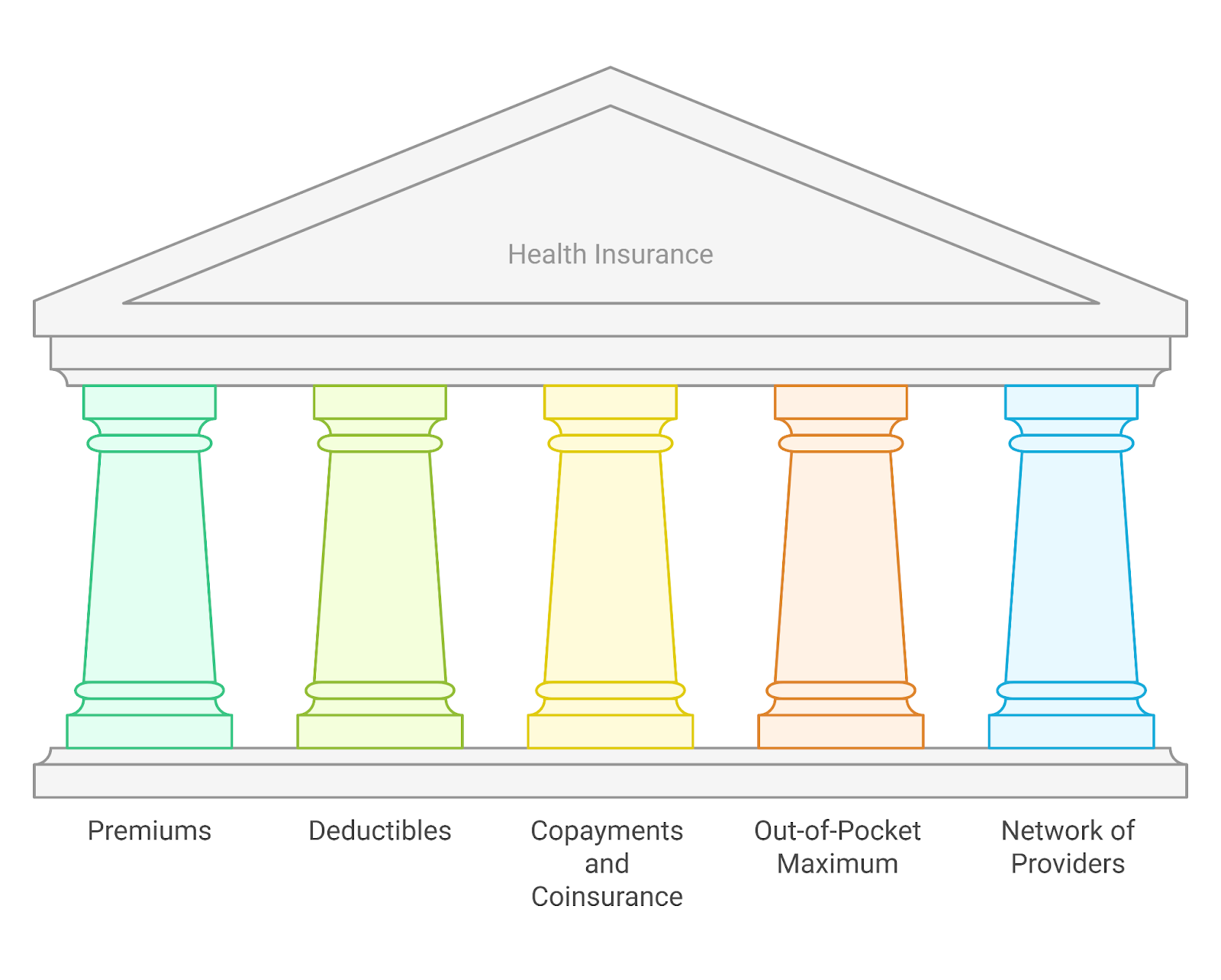

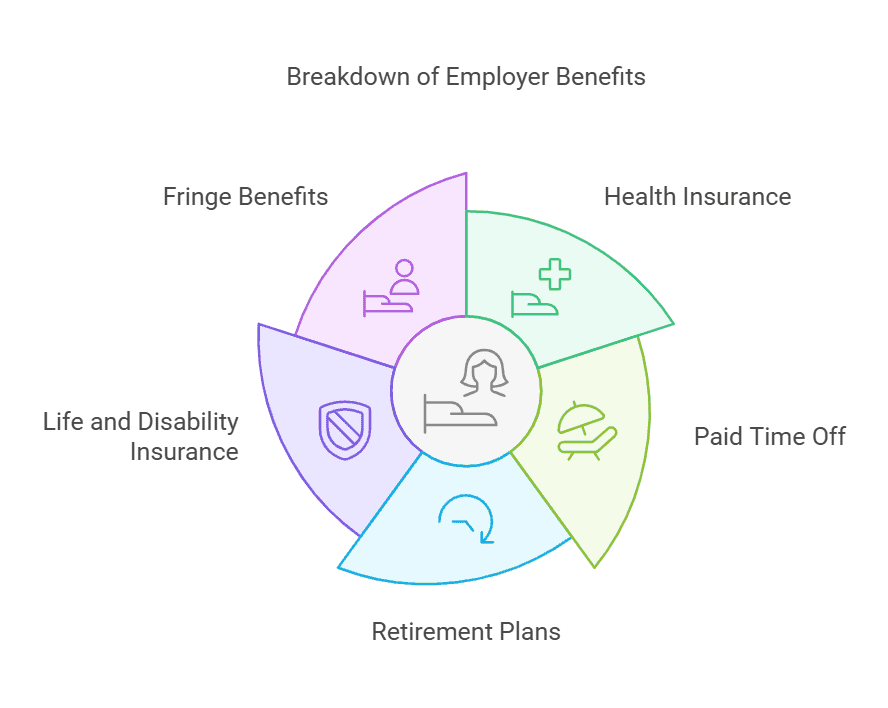

The best health insurance is designed to reduce out-of-pocket medical expenses by covering a portion of healthcare costs. A well-chosen plan ensures financial protection against unexpected medical emergencies and routine healthcare expenses. To select the best health insurance, it is essential to understand the fundamental components that influence costs and coverage. These include:

Premiums: This is the fixed monthly amount you pay to maintain your health insurance coverage, regardless of whether you use medical services. Choosing the best health insurance with an affordable premium can significantly impact your budget.

Deductibles: The deductible is the amount you must pay out-of-pocket before your insurance coverage begins. The best health insurance offers a balance between reasonable deductibles and comprehensive coverage.

Co-payments and Coinsurance: These are your share of medical costs after your deductible is met. Co-payments are fixed amounts paid for specific services (e.g., $25 for a doctor’s visit), while coinsurance is a percentage of the total service cost (e.g., 20% of a hospital bill). Understanding these costs ensures that you choose the best health insurance plan that aligns with your needs.

Out-of-Pocket Maximums: This represents the maximum amount you will have to pay in a given year for covered medical services, including deductibles, co-payments, and coinsurance. The best health insurance provides financial relief by capping these expenses.

Network Providers: The best health insurance plans often have extensive networks of preferred doctors, specialists, and hospitals. Choosing a plan with a broad network ensures greater access to healthcare facilities and minimizes out-of-pocket expenses.

Prescription Drug Coverage: Different plans have varying levels of prescription drug coverage. Reviewing a plan’s formulary (list of covered medications) ensures that your necessary prescriptions are included at an affordable cost. The best health insurance plans include comprehensive medication coverage.

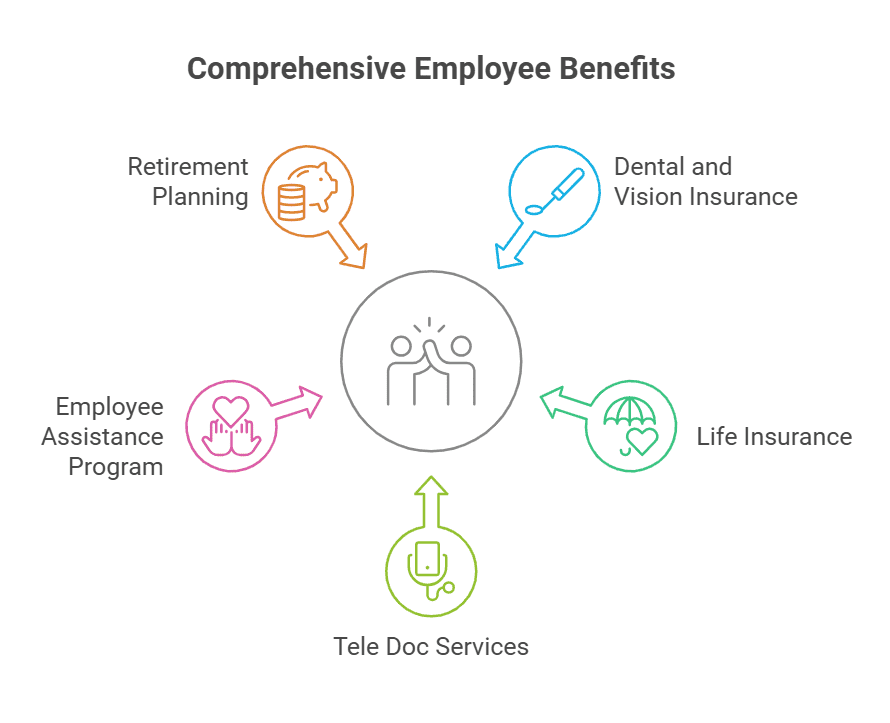

Additional Benefits: Some insurance plans offer added perks such as telemedicine services, wellness programs, dental and vision coverage, and mental health support. The best health insurance enhances overall healthcare access and convenience.

By understanding these critical aspects of health insurance, individuals can make informed decisions and choose the best health insurance plan that aligns with their healthcare needs and financial situation.

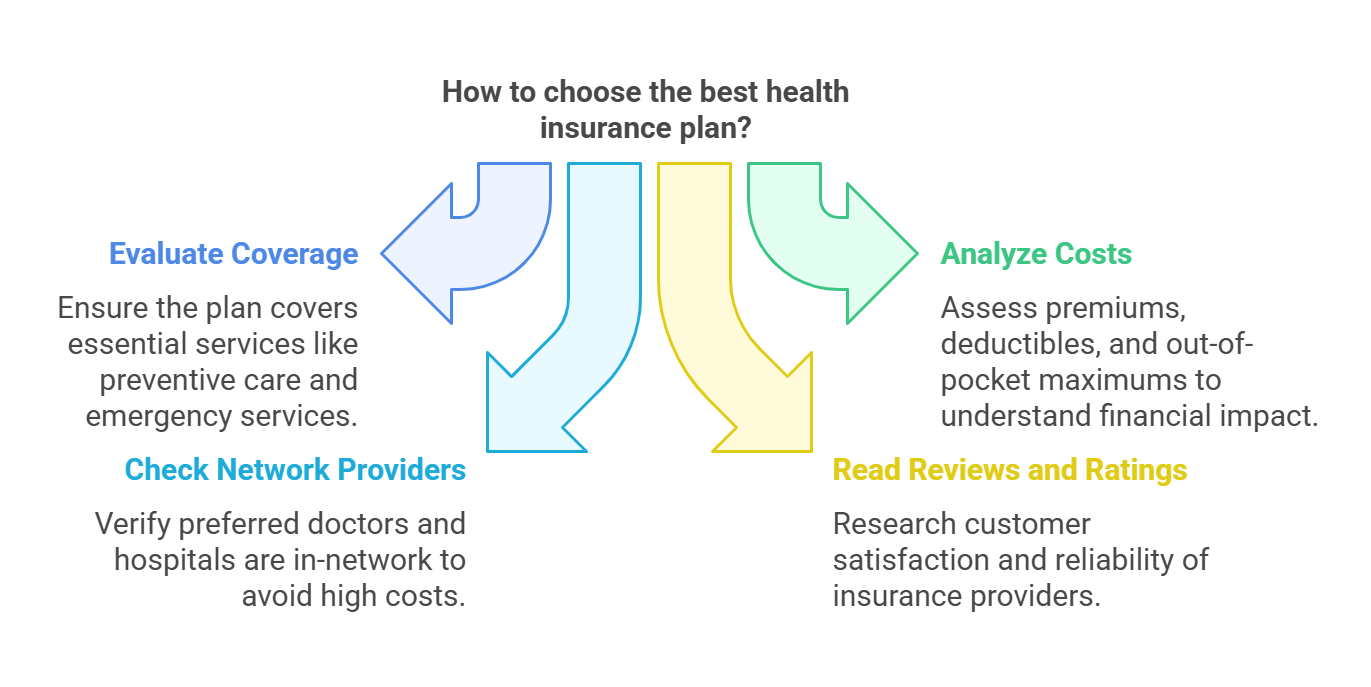

Step-by-Step Guide to Choosing the Best Health Insurance Plan for Individuals

Assess Your Healthcare Needs Evaluate past medical expenses and anticipate future healthcare requirements. Consider factors such as routine checkups, ongoing treatments, and potential emergencies. Understanding your specific health needs can help select the best health insurance plan that offers comprehensive benefits.

Compare Different Plan Types

Health Maintenance Organization (HMO): Requires using network providers and obtaining referrals for specialists. The best health insurance for those seeking lower premiums and coordinated care.

Preferred Provider Organization (PPO): Provides flexibility in choosing doctors and doesn’t require referrals. Ideal for individuals who want broader provider access and the best health insurance coverage.

Exclusive Provider Organization (EPO): Similar to HMOs but without the need for referrals. Out-of-network care is not covered, so selecting the best health insurance with a strong network is essential.

Point of Service (POS): Combines features of HMOs and PPOs; requires referrals but allows out-of-network care at higher costs.

Evaluate Provider Networks Ensure that your preferred doctors, hospitals, and specialists are in-network to avoid high out-of-pocket expenses. The best health insurance plan will provide access to quality care providers without excessive limitations.

Analyze Costs Carefully Finding the best health insurance means balancing costs and benefits. Consider:

Lower premiums often come with higher deductibles and vice versa.

Co-payments and coinsurance can significantly affect out-of-pocket spending.

Individual plans with tax advantages, like Health Savings Accounts (HSAs), can help offset costs while securing the best health insurance for your needs.

Check Prescription Drug Coverage If you take regular medications, review the insurance plan’s formulary to ensure your prescriptions are covered. The best health insurance will include affordable prescription drug benefits.

Look for Additional Benefits Some plans offer perks like telemedicine, wellness programs, or mental health services. These extras can make a plan more valuable, ensuring you get the best health insurance coverage for a well-rounded healthcare experience.

Review Plan Ratings and Customer Satisfaction Researching plan ratings and customer reviews can provide insights into service quality, claim processing speed, and overall satisfaction. The best health insurance should come from a reputable provider with positive user feedback.

Best Health Insurance Options for Individuals

For individuals and families, selecting the best health insurance involves evaluating multiple options based on personal healthcare needs and financial considerations. Some of the most popular choices include:

Marketplace (ACA) Plans

Available through government exchanges with potential subsidies.

Offer comprehensive benefits, including essential health services. The best health insurance includes a full range of preventive and emergency coverage.

Individuals can compare different metal-tier plans (Bronze, Silver, Gold, Platinum) to find the best health insurance that matches their financial situation and expected healthcare usage.

Short-Term Health Insurance

A temporary solution but not as comprehensive as the best health insurance plans.

Best for those in between jobs or waiting for permanent coverage.

Can be an affordable option for healthy individuals who need minimal coverage but still want protection in case of emergencies.

High Deductible Health Plans (HDHPs) with HSAs

Lower premiums with tax-advantaged savings accounts.

Ideal for those who want to save on premiums while having emergency coverage under the best health insurance policy.

HSAs allow tax-free contributions and withdrawals for medical expenses, making them a cost-effective way to manage healthcare costs while maintaining the best health insurance coverage.

Catastrophic Health Insurance

Designed for individuals under 30 or those with hardship exemptions.

Covers essential benefits but with high deductibles.

The best health insurance choice for young, healthy individuals who want protection against major medical expenses while keeping premiums low.

Private Health Insurance Plans

Available outside of ACA marketplaces, often offering more flexibility in coverage options.

Can be customized to include additional benefits like dental and vision care.

The best health insurance choice for individuals looking for tailored plans that better fit their specific healthcare needs.

By carefully assessing these options, individuals can find the best health insurance plan that provides comprehensive coverage at an affordable price.

Final Thoughts: Finding the Best Health Insurance Made Simple

Selecting the best health insurance involves evaluating healthcare needs, comparing plan types, assessing costs, and considering provider networks. Small businesses and self-employed individuals must balance affordability with quality care access. Working with organizations like PEO4YOU can simplify the process, ensuring access to comprehensive coverage without administrative challenges.

By following these steps, small business owners and independent professionals can confidently choose the best health insurance plan that meets their needs and provides peace of mind for the future.

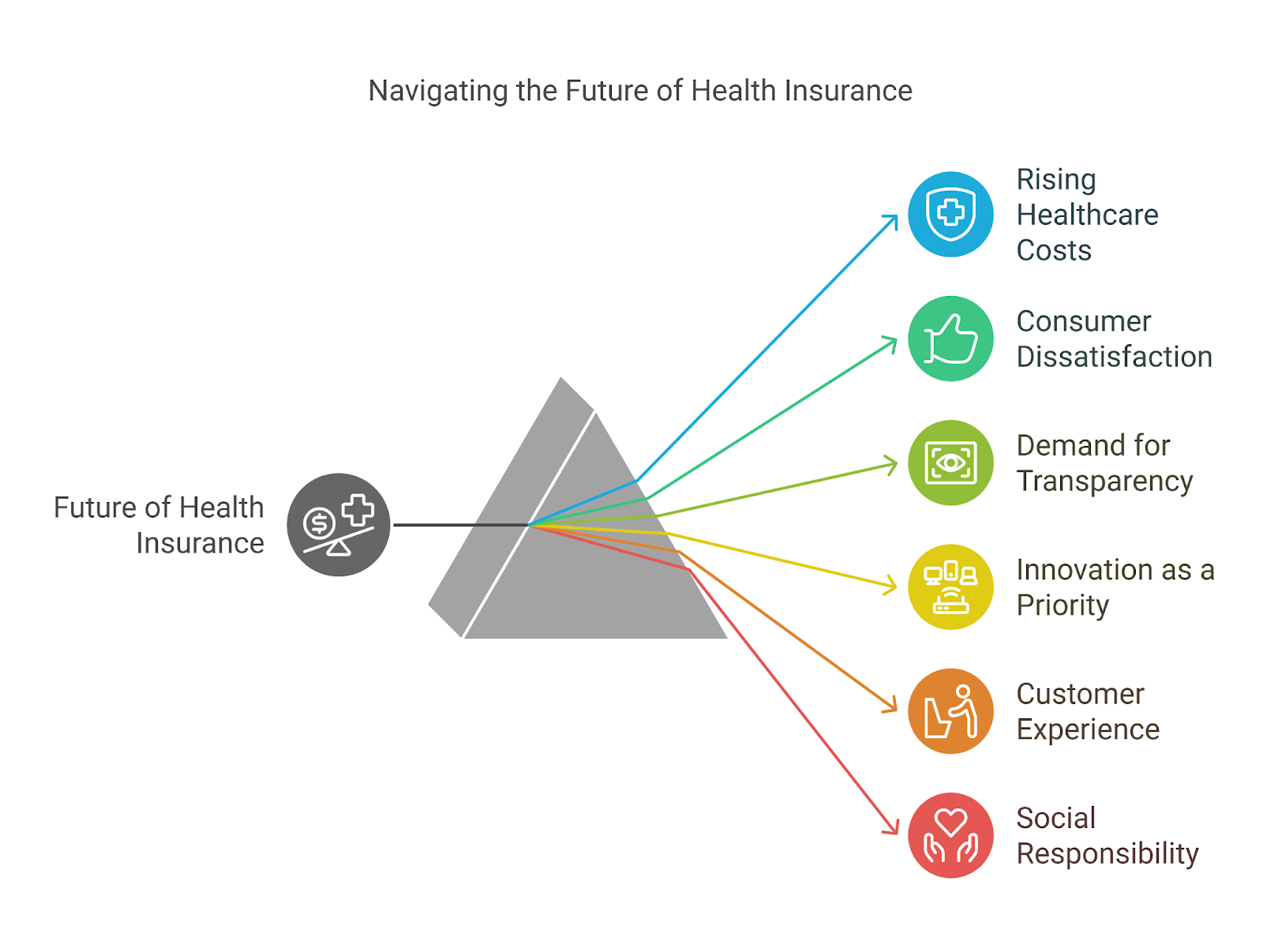

The health insurance industry is at a critical turning point, facing increasing pressure to evolve and adapt to modern challenges. From rising healthcare costs to consumer dissatisfaction with claim denials, the demand for a more transparent and efficient US insurance policy framework is higher than ever. To navigate this landscape successfully, insurance leaders must adopt forward-thinking strategies that prioritize innovation, customer experience, and social responsibility.

Strategic Themes for Insurance Leaders

1. Enhancing Customer Experience

The traditional US insurance policy model often frustrates consumers with complex claim processes, delayed approvals, and a lack of transparency. To improve customer experience, insurance companies must:

Simplify claim approvals: By leveraging artificial intelligence (AI) and automated processing, insurers can reduce claim approval times and enhance patient access to timely care.

Provide proactive communication: Real-time updates on claims, benefits, and cost estimates help customers make informed decisions.

Develop self-service platforms: Mobile apps and online portals should allow users to check coverage details, track claims, and access telehealth services with ease.

Reduce administrative burdens: By eliminating excessive paperwork and bureaucratic hurdles, insurers can make it easier for patients and healthcare providers to interact with their plans.

2. Promoting Transparency in Pricing and Coverage

Many individuals and businesses struggle to understand the true cost of healthcare services under their US insurance policy. Insurance leaders should:

Offer upfront pricing tools: Cost estimator tools should be widely available so customers can anticipate expenses before seeking medical care.

Clarify benefits and limitations: Policyholders should clearly understand what their plan covers, including exclusions and out-of-network charges.

Enhance provider transparency: Insurers should partner with healthcare providers to ensure patients receive clear pricing information before receiving treatment.

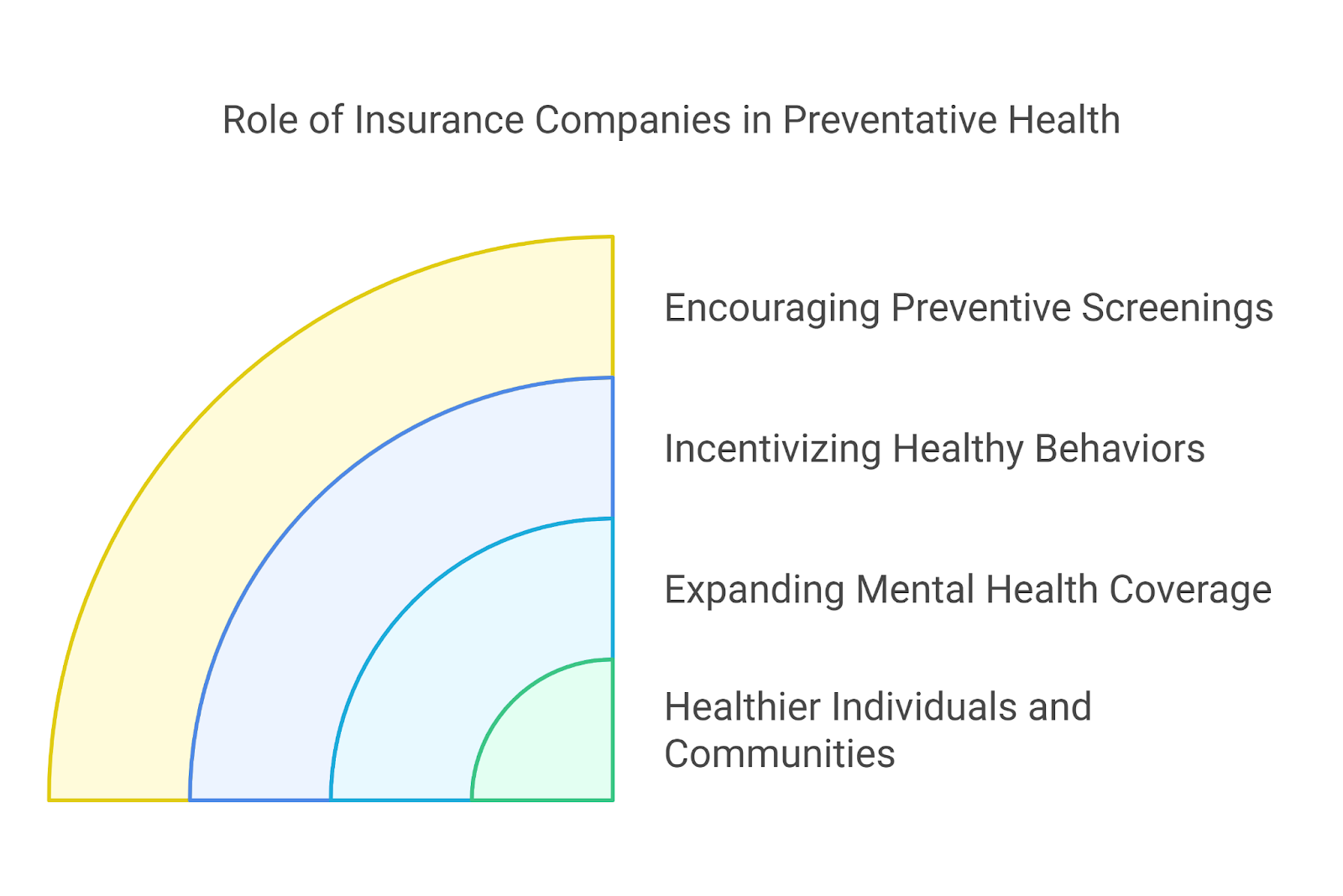

3. Focusing on Preventative Health and Wellness Programs

A shift from reactive to proactive healthcare can significantly reduce costs and improve population health. Insurance companies must:

Encourage preventive screenings: Routine screenings for diseases such as cancer, diabetes, and heart disease can lead to early detection and better outcomes.

Incentivize healthy behaviors: Some US insurance policy models already reward individuals who engage in physical activity, maintain healthy diets, or undergo wellness checkups.

Expand mental health coverage: Addressing mental well-being is just as important as physical health. Insurers should increase access to therapy, counseling, and stress management programs.

4. Embracing Technological Innovation

Technology is revolutionizing healthcare, and insurance companies must keep pace by integrating digital tools into their US insurance policy frameworks. Key innovations include:

AI-driven claims processing: Automated claim approvals can reduce fraud, speed up reimbursements, and improve efficiency.

Telehealth expansion: Virtual doctor visits should be seamlessly integrated into insurance networks, offering patients convenience and cost savings.

Wearable health tracking: Devices that monitor heart rate, blood pressure, and activity levels can be used to tailor health plans and reward positive lifestyle choices.

5. Aligning Insurance with Social Purpose

The future of the US insurance policy landscape requires a greater commitment to social well-being. This means:

Expanding access to underserved populations: Insurance companies must work to make healthcare coverage more affordable and accessible to low-income individuals and small businesses.

Investing in community health initiatives: Collaborating with local organizations to promote education, vaccination programs, and chronic disease management can have a lasting positive impact.

Ensuring ethical business practices: Companies must prioritize fair pricing, ethical claim management, and corporate responsibility to gain public trust.

The Largest Health Insurance Company in the U.S.

As of 2024, UnitedHealth Group is the largest health insurance provider in the United States. The company, which operates through UnitedHealthcare, holds a dominant position in the US insurance policy market with a 15.7% share and generates over $215 billion in revenue annually.

Why is UnitedHealth Group the Largest?

Nationwide Coverage: UnitedHealth Group offers plans in all 50 states, ensuring broad accessibility.

Diverse Insurance Products: The company provides individual, employer-sponsored, Medicare, and Medicaid plans, appealing to a wide customer base.

Technological Investment: Through its Optum subsidiary, UnitedHealth integrates data analytics, AI, and telehealth solutions to enhance patient care and insurance efficiency.

While UnitedHealth Group leads the industry, other major players include Anthem (Elevance Health), Aetna, Cigna, and Humana, each competing in different segments of the US insurance policy landscape.

Evaluating the Best Healthcare Systems

Determining the best healthcare system depends on factors like affordability, access, and overall health outcomes. Here’s how some top-ranking systems compare:

Switzerland – Universal health care with private and public insurance options. It has low wait times, high-quality care, and strict cost regulation.

United Kingdom – The National Health Service (NHS) provides government-funded healthcare, ensuring accessibility for all citizens.

Germany – A multi-payer system where both private and public insurance coexist, offering competitive pricing and broad access.

United States – While it leads in medical innovation, the US insurance policy structure creates barriers due to high costs and coverage limitations.

Choosing a Good Insurance Plan

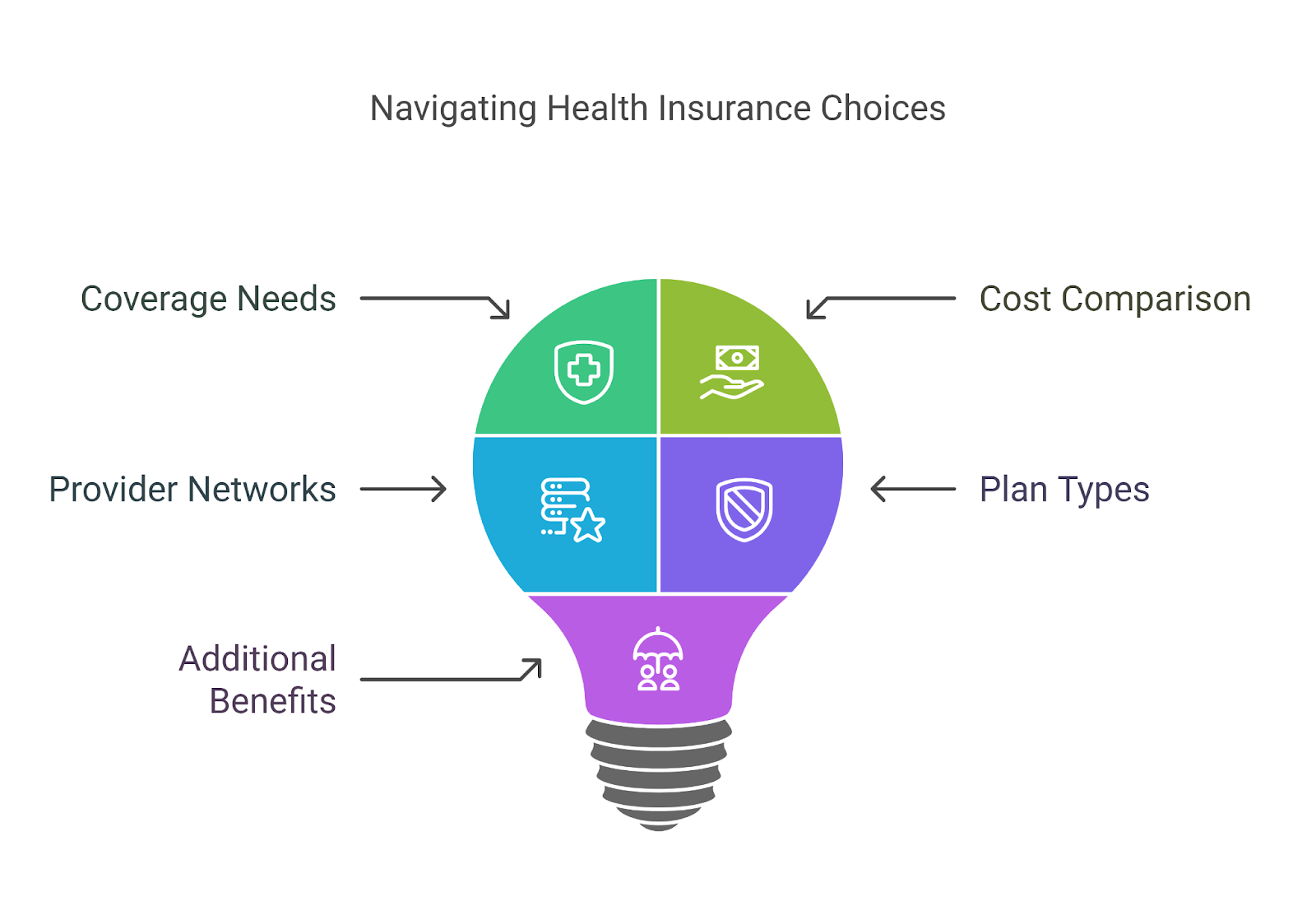

Selecting the right health insurance plan can be overwhelming. To make an informed decision, consider these essential factors:

1. Assess Your Coverage Needs

Think about how often you visit doctors, whether you need specialty care, and if you require regular prescriptions. A strong US insurance policy should cover these essentials.

2. Compare Costs

Premiums: The amount you pay monthly.

Deductibles: The cost you must pay before insurance covers services.

Copays & Coinsurance: Additional out-of-pocket expenses for medical visits or prescriptions.

3. Check Provider Networks

Some US insurance policy plans restrict which doctors and hospitals you can use. Make sure your preferred providers are in-network to avoid extra costs.

4. Understand Plan Types

HMO (Health Maintenance Organization): Requires referrals for specialists, typically lower costs.

PPO (Preferred Provider Organization): More flexibility in choosing doctors, but higher premiums.

EPO (Exclusive Provider Organization): No out-of-network coverage but lower premiums than PPOs.

POS (Point of Service): A mix of HMO and PPO features.

5. Consider Additional Benefits

A comprehensive US insurance policy should include:

Telehealth services for virtual doctor visits.

Mental health coverage for therapy and counseling.

Wellness incentives like discounts on gym memberships.

Conclusion

The US insurance policy is going under significant transformation, with a greater emphasis on transparency, affordability, and innovation. As the industry moves forward, businesses and individuals must stay informed to choose the best healthcare plans.For those seeking expert guidance, PEO4YOUserves as a trusted option, helping clients navigate the complexities of the US insurance policy market. Whether you’re a small business owner looking for employee coverage or an individual seeking personalized insurance solutions, PEO4YOU connects you with cost-effective, high-quality healthcare plans. By partnering with reputable insurance providers, PEO4YOU ensures access to the best coverage options tailored to your needs.

Insurance in healthcare serves as a crucial safeguard, providing access to medical services and protecting individuals from exorbitant healthcare costs. Without insurance in healthcare, individuals face significant financial burdens, limited access to care, and poorer health outcomes. In the United States, healthcare expenses can be overwhelming, and having insurance in healthcare can mean the difference between getting timely medical attention and suffering long-term consequences due to delayed treatment.

Financial Implications

One of the most immediate risks of not having health insurance is the potential for high out-of-pocket medical expenses. If you get sick or injured and need to visit the doctor, go to the emergency room, or undergo surgery, you’ll be responsible for paying the full cost of care. Without insurance in healthcare, these expenses can quickly accumulate, leading to substantial debt or even bankruptcy.

Key Financial Risks of Being Uninsured:

High Medical Bills: A single emergency room visit can cost thousands of dollars, even for relatively minor health issues. More serious conditions, such as heart attacks or broken bones, can result in bills exceeding tens of thousands of dollars.

Lack of Preventive Care: Without insurance in healthcare, many people avoid regular check-ups and screenings due to cost concerns, leading to undiagnosed and untreated medical conditions that become more expensive to treat later.

Medical Debt and Bankruptcy: Medical expenses are one of the leading causes of bankruptcy in the U.S. A study found that over 60% of all bankruptcies in 2007 were significantly influenced by illness and medical bills.

Limited Access to Prescription Medications: Without insurance in healthcare, prescription medications can be prohibitively expensive, leading many to skip doses or avoid taking necessary medications altogether.

Access to Health Insurance in Healthcare

Uninsured individuals often delay or forgo necessary medical care due to cost concerns. This includes skipping routine check-ups, preventive services, and treatments for chronic conditions. Delaying or avoiding healthcare can worsen illnesses or injuries, leading to more severe health issues and higher medical costs in the long run.

How Being Uninsured Limits Access to Care:

Avoidance of Preventive Services: Routine health screenings, vaccinations, and wellness visits are essential in detecting and preventing diseases early. Without insurance in healthcare, many individuals skip these crucial check-ups.

Delayed Diagnosis and Treatment: Individuals without insurance in healthcare may wait until their condition worsens before seeking medical attention. This can lead to more advanced diseases, requiring more aggressive and costly treatments.

Limited Access to Specialists: Many uninsured individuals have difficulty accessing specialist care, such as cardiologists, oncologists, or endocrinologists, due to high costs.

Higher Out-of-Pocket Costs for Emergency Care: Hospitals are legally required to provide emergency care regardless of insurance status. However, uninsured patients often receive hefty bills that can be financially devastating.

Reduced Access to Mental Health Services: Mental health treatment, including therapy and medications, can be expensive without insurance in healthcare, preventing many from seeking necessary support.

Health Outcomes

Lack of insurance in healthcare is associated with poorer health outcomes. Studies show that uninsured individuals are:

Less likely to receive preventive care, leading to late-stage diagnoses of serious conditions like cancer and diabetes.

More likely to experience complications from chronic illnesses due to inadequate disease management.

At a higher risk of mortality due to delayed treatment, particularly in cases of cardiovascular diseases, strokes, and other severe conditions.

More likely to have extended hospital stays because they often seek medical attention later in the course of their illness, requiring more intensive treatment.

For example, uninsured stroke patients suffer from greater neurological impairments, longer hospital stays, and higher risk of death compared to similar patients with adequate coverage.

Legal and Policy Considerations

Under the Affordable Care Act (ACA) of 2010, all Americans were initially required to carry health insurance or face a penalty known as the “individual mandate.” However, in 2019, the federal government eliminated the enforcement of this mandate, leaving it up to individual states to decide whether to require health insurance. Some states still enforce penalties for not having insurance in healthcare, making it essential to understand the specific requirements in your location.

Even though there is no longer a federal mandate, staying insured remains a crucial step toward financial and medical security.

Low-Income Families: Many uninsured individuals come from lower-income households that may not qualify for Medicaid but also cannot afford private insurance in healthcare.

Working Adults Without Employer-Sponsored Insurance: Many people work jobs that do not offer health benefits, leaving them without affordable coverage options.

Young Adults: Some younger adults opt out of health insurance in healthcare, believing they don’t need coverage. However, accidents and unexpected illnesses can happen at any age.

Racial and Ethnic Disparities: Studies show that Hispanic, Black, and Indigenous populations are disproportionately uninsured compared to white Americans.

Why Does Health Insurance in HealthcareMatter?

Health insurance in healthcare is not just about avoiding medical debt—it plays a vital role in maintaining long-term health and financial stability.

Key Benefits of Having Health Insurance

Access to Preventive Care: Insured individuals are more likely to receive vaccines, cancer screenings, and wellness exams, catching diseases early when they are easier to treat.

Lower Prescription Drug Costs: Insurance in healthcare helps cover medication costs, making it easier to afford necessary treatments.

Better Management of Chronic Conditions: People with insurance in healthcare are more likely to manage conditions such as diabetes, heart disease, and high blood pressure, reducing complications.

Protection from Catastrophic Medical Expenses: Serious accidents or illnesses can lead to overwhelming medical bills. Health insurance in healthcare helps cover these expenses, preventing financial ruin.

Improved Mental Health Access: Many insurance plans provide coverage for mental health services, including therapy and psychiatric care, which are crucial for overall well-being.

The Financial and Health Impact of Being Insured

Uninsured individuals with heart disease and stroke have higher mortality rates than those with adequate insurance in healthcare.

Medical bills are responsible for a significant portion of bankruptcies in the U.S., and nearly 80% of those who filed for medical bankruptcy had insurance but were underinsured.

Insured individuals receive more consistent and timely care, leading to better overall health outcomes and quality of life.

Conclusion:The Critical Need for Reliable Health Coverage

The absence of insurance in healthcare poses significant risks, including financial hardship, limited access to care, and adverse health outcomes. Without coverage, individuals may face crippling medical debt, struggle to access necessary healthcare services, and suffer from poorer long-term health.

Securing adequate insurance in healthcare is essential for protecting both health and financial well-being. Organizations like PEO4YOU assist individuals and small businesses in finding suitable health coverage options. Their services help mitigate the risks associated with being uninsured, ensuring access to necessary healthcare services.If you or your employees need help navigating the complexities of insurance in healthcare, consider reaching out to PEO4YOU to explore your coverage options and safeguard your future.

In a landmark decision, Suffolk County Superior Court Judge Helene Kazanjian has ordered three UnitedHealth-owned insurance companies to pay over $165 million for engaging in deceptive sales practices that misled thousands of Massachusetts consumers into unknowingly purchasing supplemental health insurance.

Unmasking Deceptive Practices: A Deep Dive into Misleading Tactics

Between 2012 and 2016, HealthMarkets and its subsidiaries marketed bundled major medical and supplemental insurance policies in a manner that deceived consumers. Sales agents were trained to obscure the costs of individual policies, leading consumers to purchase supplemental coverage without their knowledge. This practice particularly targeted financially vulnerable individuals, causing them to buy unnecessary or unaffordable products.

Court Ruling and Penalties

The court’s decision includes nearly $50.1 million in restitution to affected consumers and $115.1 million in civil penalties, marking the largest civil penalty ever awarded under Massachusetts’ consumer protection law. Attorney General Andrea Campbell emphasized that the ruling holds the companies accountable for preying on vulnerable individuals and provides meaningful restitution to consumers across the Commonwealth.

Government Measures and Impact on Massachusetts Health Insurance

In response to such deceptive practices, the Massachusetts government has implemented stricter regulations to enhance transparency and protect consumers. These measures include increased reporting requirements for insurance companies, enhanced oversight by regulatory bodies, and higher penalties for non-compliance. The aim is to ensure that consumers have access to accurate information, enabling them to choose the best health plan that suits their needs.

These regulatory changes are expected to foster a more transparent and competitive health insurance market in Massachusetts. Consumers will benefit from clearer information, aiding them in selecting the best health plan. Insurance companies are now under greater scrutiny, which may lead to improved business practices and a focus on customer satisfaction.

Health Insurance in Massachusetts

Massachusetts has long been a leader in health insurance reform, striving to provide comprehensive coverage to its residents. The state’s health insurance market offers a variety of plans to individuals and small groups, categorized into metallic levels—Platinum, Gold, Silver, Bronze, and Catastrophic—each providing different levels of coverage and cost-sharing.

However, residents are facing rising health insurance costs. In 2025, premiums are expected to increase at a faster rate than in previous years, with the state’s largest insurers projecting average hikes of 8% to 10%. Some businesses and their employees may experience increases as high as 15%, adding financial strain to consumers seeking the best health plan.

Tips for Selecting the Best Health Plan

Choosing the best health plan requires careful consideration of several factors:

Assess Your Health Care Needs: Evaluate your medical history, anticipated health care needs, and preferred providers to determine the level of coverage required.

Understand Plan Types: Familiarize yourself with different plan types, such as Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), and Exclusive Provider Organizations (EPOs), to identify which aligns with your preferences.

Compare Costs: Analyze premiums, deductibles, copayments, and out-of-pocket maximums to understand the financial implications of each plan.

Check Provider Networks: Ensure that your preferred doctors and hospitals are included in the plan’s network to avoid additional out-of-network charges.

Review Prescription Drug Coverage: Confirm that any medications you require are covered under the plan’s formulary.

Consider Additional Benefits: Look for plans that offer extra services, such as dental, vision, or wellness programs, which may be important to you.

Evaluate Plan Ratings: Research plan ratings and consumer reviews to gauge satisfaction and quality of care provided.

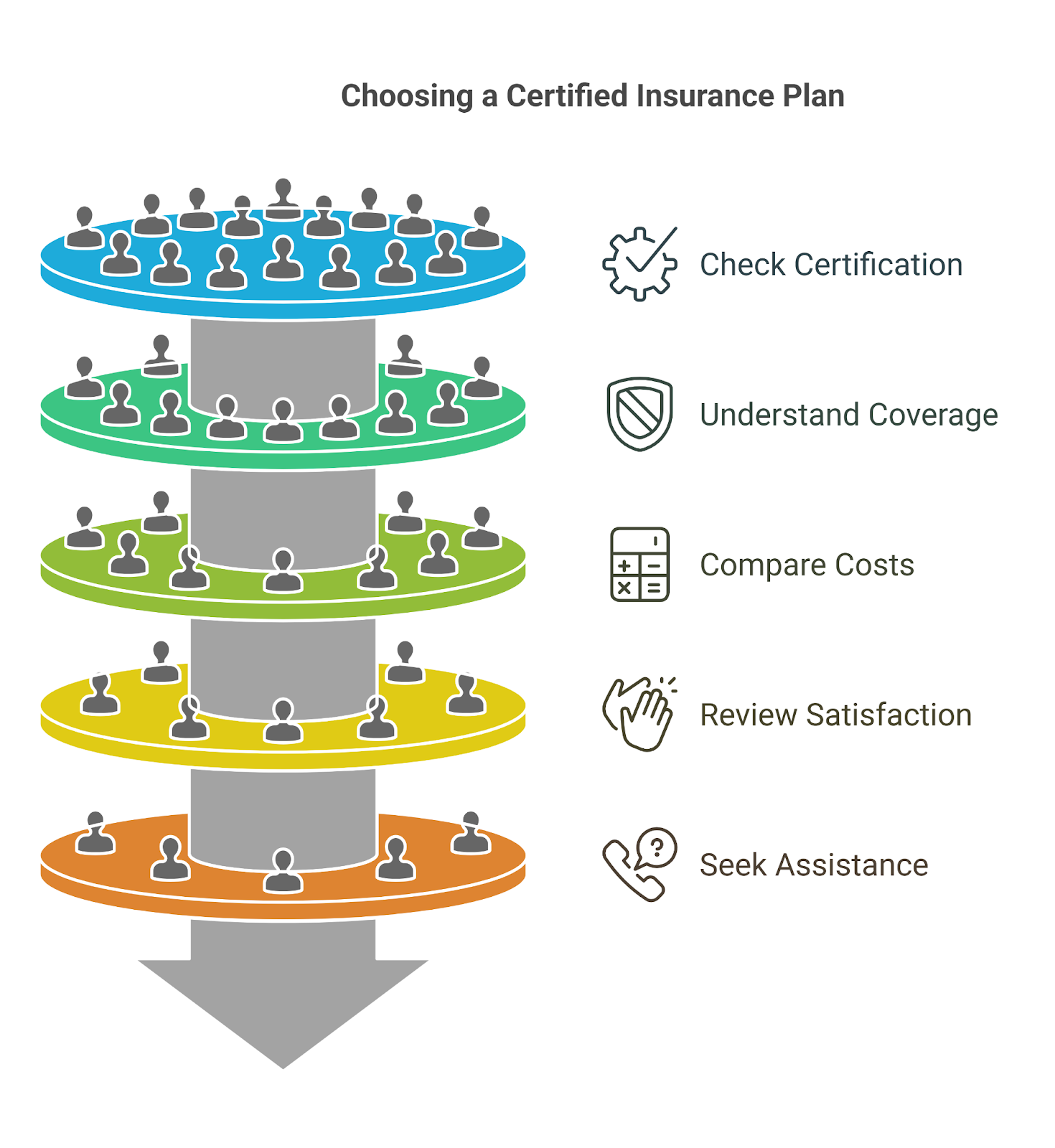

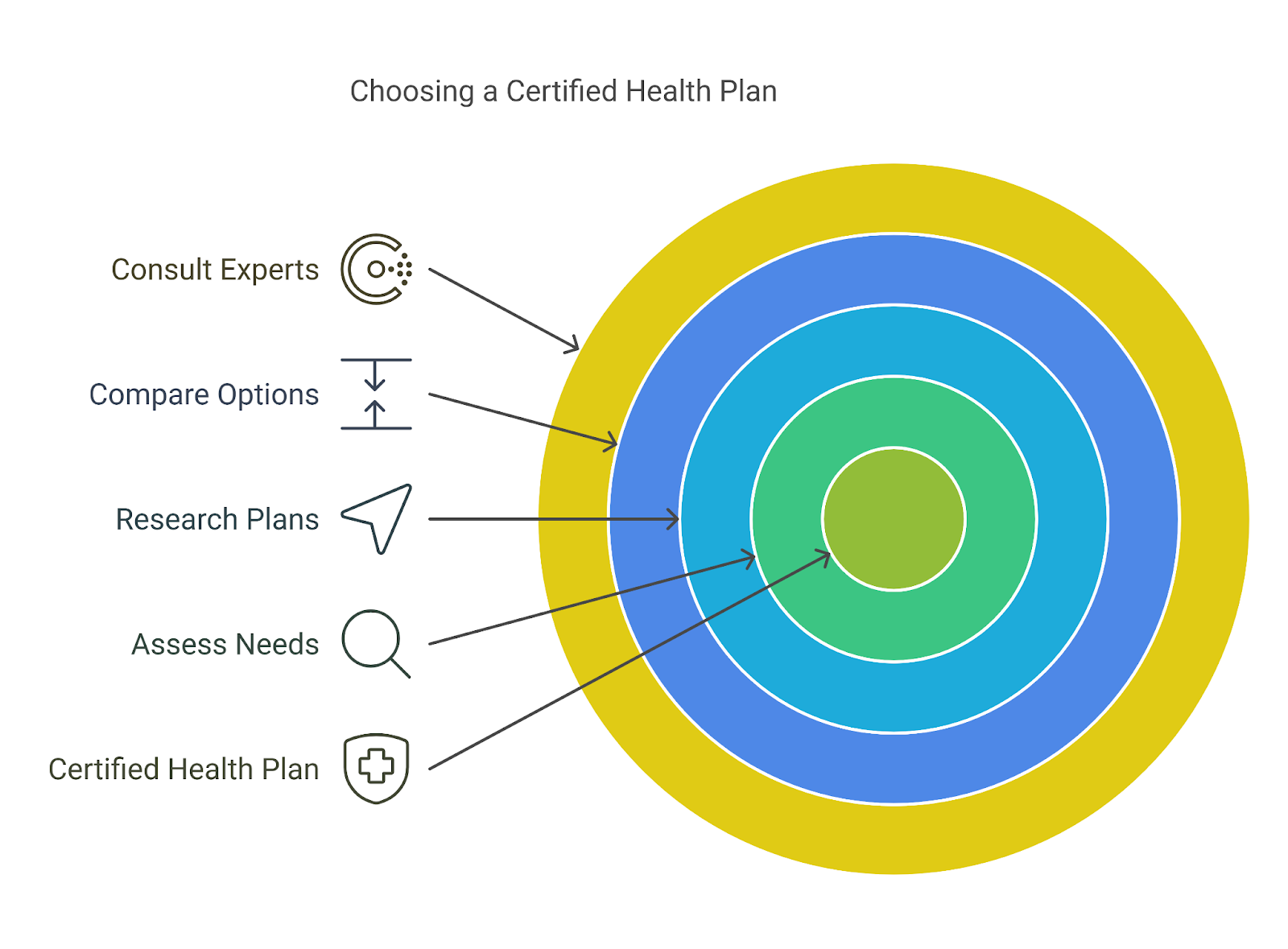

Selecting a Certified Insurance Plan

When choosing the best health plan, ensuring that it is certified is a crucial step. A certified health insurance plan meets specific standards set by government agencies, guaranteeing that it provides comprehensive and legally compliant coverage. Here’s how you can verify and select a certified insurance plan in Massachusetts:

1. Check for Certification by the Massachusetts Health Connector

Massachusetts has a state-run health insurance marketplace, the Massachusetts Health Connector, where individuals and small businesses can purchase health plans that meet both federal and state requirements. Plans listed on the Health Connector are certified Qualified Health Plans (QHPs) and comply with Affordable Care Act (ACA) regulations.

How to Verify

Visit the Massachusetts Health Connector and browse available plans.

Look for labels such as Qualified Health Plan (QHP) or Massachusetts Seal of Approval.

Confirm that the plan covers essential health benefits like hospitalization, prescription drugs, maternity care, and preventive services.

2. Confirm Compliance with State and Federal Standards

Certified plans must follow Massachusetts’ strict insurance laws, which often exceed federal ACA requirements. A certified plan should:

Cover pre-existing conditions with no extra charges.

Include comprehensive benefits such as mental health services and pediatric care.

Ensure network adequacy, meaning a sufficient number of doctors and hospitals accept the plan.

Follow rate review policies, where the state regulates how much insurers can increase prices.

3. Differentiate ACA Marketplace Plans vs. Off-Market Plans

Not all insurance plans sold in Massachusetts are certified. Some insurers sell plans outside of the official Health Connector, known as off-exchange plans. While these may be legitimate, they do not always meet the same strict regulations.

Key Considerations

If you qualify for subsidies or financial assistance, purchase a certified plan through the Massachusetts Health Connector to access potential cost savings.

If you’re buying directly from an insurer, confirm that their plan meets MCC (Minimum Creditable Coverage) and ACA standards before enrolling.

4. Verify the Insurance Carrier’s Accreditation

Reputable insurance companies typically undergo accreditation from national health insurance oversight organizations, such as:

National Committee for Quality Assurance (NCQA) – Assesses provider network quality and customer service.

URAC – Evaluates care management and compliance with consumer protection laws.

Accreditation by Blue Cross Blue Shield, UnitedHealth, or other well-established insurers – Ensures strong financial backing and provider access.

How to Check Accreditation

Visit the insurer’s website to check for accreditation badges.

Search for customer complaints on the Better Business Bureau (BBB) or Massachusetts Attorney General’s Consumer Protection Division.

5. Seek Professional Assistance from Licensed Brokers or Intermediaries

If you’re unsure which certified health plan fits your needs, working with an independent insurance broker or intermediary can be helpful. Organizations like PEO4YOU specialize in helping individuals and businesses find certified insurance plans that offer the best value.

By following these steps, you can ensure that you select a certified insurance plan that meets both your healthcare needs and legal compliance requirements.

How PEO4YOU Helps

–Provides access to certified, ACA-compliant plans from multiple insurers.

–Offers personalized guidance to match your budget and healthcare needs.

–Assists small businesses in selecting group health plans that comply with Massachusetts regulations.

Why Choosing a Certified Plan Matters

A certified insurance plan ensures that you receive the best health plan possible—one that is legal, comprehensive, and financially sound. Whether you are an individual seeking personal coverage or a small business looking for employee benefits, selecting a certified plan means you are protected under Massachusetts and federal health laws. By following these steps, you can confidently choose the best health plan for yourself or your employees.

Conclusion

The recent court ruling against UnitedHealth’s subsidiaries underscores the importance of transparency and consumer protection in the health insurance industry. As Massachusetts residents navigate a landscape of rising premiums and numerous plan options, selecting the best health plan becomes increasingly critical.

Companies like PEO4YOU play a vital role in assisting individuals and small businesses in finding suitable health care coverage. By offering access to comprehensive health plans, PEO4YOU helps clients make informed decisions tailored to their unique needs. Their commitment to cost transparency, affordable renewals, and human-centered claims management ensures that consumers receive the support they need in selecting and managing their health insurance plans.

In an environment where choosing the right health plan is paramount, leveraging the expertise of trusted intermediaries can provide peace of mind and financial security, ensuring that consumers obtain the coverage that best suits their circumstances.

Insurance in healthcare serves as a crucial safeguard, providing access to medical services and protecting individuals from exorbitant healthcare costs. Without insurance in healthcare, individuals face significant financial burdens, limited access to care, and poorer health outcomes. In the United States, healthcare expenses can be overwhelming, and having insurance in healthcare can mean the difference between getting timely medical attention and suffering long-term consequences due to delayed treatment.

Financial Implications

One of the most immediate risks of not having health insurance is the potential for high out-of-pocket medical expenses. If you get sick or injured and need to visit the doctor, go to the emergency room, or undergo surgery, you’ll be responsible for paying the full cost of care. Without insurance in healthcare, these expenses can quickly accumulate, leading to substantial debt or even bankruptcy.

Key Financial Risks of Being Uninsured

High Medical Bills: A single emergency room visit can cost thousands of dollars, even for relatively minor health issues. More serious conditions, such as heart attacks or broken bones, can result in bills exceeding tens of thousands of dollars.

Lack of Preventive Care: Without insurance in healthcare, many people avoid regular check-ups and screenings due to cost concerns, leading to undiagnosed and untreated medical conditions that become more expensive to treat later.

Medical Debt and Bankruptcy: Medical expenses are one of the leading causes of bankruptcy in the U.S. A study found that over 60% of all bankruptcies in 2007 were significantly influenced by illness and medical bills.

Limited Access to Prescription Medications: Without insurance in healthcare, prescription medications can be prohibitively expensive, leading many to skip doses or avoid taking necessary medications altogether.

Access to Healthcare Services

Uninsured individuals often delay or forgo necessary medical care due to cost concerns. This includes skipping routine check-ups, preventive services, and treatments for chronic conditions. Delaying or avoiding healthcare can worsen illnesses or injuries, leading to more severe health issues and higher medical costs in the long run.

How Being Uninsured Limits Access to Care

Avoidance of Preventive Services: Routine health screenings, vaccinations, and wellness visits are essential in detecting and preventing diseases early. Without insurance in healthcare, many individuals skip these crucial check-ups.

Delayed Diagnosis and Treatment: Individuals without insurance in healthcare may wait until their condition worsens before seeking medical attention. This can lead to more advanced diseases, requiring more aggressive and costly treatments.

Limited Access to Specialists: Many uninsured individuals have difficulty accessing specialist care, such as cardiologists, oncologists, or endocrinologists, due to high costs.

Higher Out-of-Pocket Costs for Emergency Care: Hospitals are legally required to provide emergency care regardless of insurance status. However, uninsured patients often receive hefty bills that can be financially devastating.

Reduced Access to Mental Health Services: Mental health treatment, including therapy and medications, can be expensive without insurance in healthcare, preventing many from seeking necessary support.

Health Outcomes

Lack of insurance in healthcare is associated with poorer health outcomes. Studies show that uninsured individuals are:

Less likely to receive preventive care, leading to late-stage diagnoses of serious conditions like cancer and diabetes.

More likely to experience complications from chronic illnesses due to inadequate disease management.

At a higher risk of mortality due to delayed treatment, particularly in cases of cardiovascular diseases, strokes, and other severe conditions.

More likely to have extended hospital stays because they often seek medical attention later in the course of their illness, requiring more intensive treatment.

For example, uninsured stroke patients suffer from greater neurological impairments, longer hospital stays, and higher risk of death compared to similar patients with adequate coverage.

Legal and Policy Considerations

Under the Affordable Care Act (ACA) of 2010, all Americans were initially required to carry health insurance or face a penalty known as the “individual mandate.” However, in 2019, the federal government eliminated the enforcement of this mandate, leaving it up to individual states to decide whether to require health insurance. Some states still enforce penalties for not having insurance in healthcare, making it essential to understand the specific requirements in your location.

Even though there is no longer a federal mandate, staying insured remains a crucial step toward financial and medical security.

The Uninsured Population

Despite coverage gains under the ACA, millions of Americans remain uninsured. In 2023, an estimated 25.3 million people ages 0-64 lacked health insurance.

Who Are the Uninsured?

Low-Income Families: Many uninsured individuals come from lower-income households that may not qualify for Medicaid but also cannot afford private insurance in healthcare.

Working Adults Without Employer-Sponsored Insurance: Many people work jobs that do not offer health benefits, leaving them without affordable coverage options.

Young Adults: Some younger adults opt out of health insurance in healthcare, believing they don’t need coverage. However, accidents and unexpected illnesses can happen at any age.

Racial and Ethnic Disparities: Studies show that Hispanic, Black, and Indigenous populations are disproportionately uninsured compared to white Americans.

Why Does Coverage Matter?

Health insurance in healthcare is not just about avoiding medical debt—it plays a vital role in maintaining long-term health and financial stability.

Key Benefits of Having Health Insurance

Access to Preventive Care: Insured individuals are more likely to receive vaccines, cancer screenings, and wellness exams, catching diseases early when they are easier to treat.

Lower Prescription Drug Costs: Insurance in healthcare helps cover medication costs, making it easier to afford necessary treatments.

Better Management of Chronic Conditions: People with insurance in healthcare are more likely to manage conditions such as diabetes, heart disease, and high blood pressure, reducing complications.

Protection from Catastrophic Medical Expenses: Serious accidents or illnesses can lead to overwhelming medical bills. Health insurance in healthcare helps cover these expenses, preventing financial ruin.

Improved Mental Health Access: Many insurance plans provide coverage for mental health services, including therapy and psychiatric care, which are crucial for overall well-being.

The Financial and Health Impact of Being Insured

Uninsured individuals with heart disease and stroke have higher mortality rates than those with adequate insurance in healthcare.

Medical bills are responsible for a significant portion of bankruptcies in the U.S., and nearly 80% of those who filed for medical bankruptcy had insurance but were underinsured.

Insured individuals receive more consistent and timely care, leading to better overall health outcomes and quality of life.

Conclusion:The Critical Need for Reliable Health Coverage

The absence of insurance in healthcare poses significant risks, including financial hardship, limited access to care, and adverse health outcomes. Without coverage, individuals may face crippling medical debt, struggle to access necessary healthcare services, and suffer from poorer long-term health.

Securing adequate insurance in healthcare is essential for protecting both health and financial well-being. Organizations like PEO4YOU assist individuals and small businesses in finding suitable health coverage options, acting as intermediaries between clients and health insurance companies. Their services help mitigate the risks associated with being uninsured, ensuring access to necessary healthcare services.If you or your employees need help navigating the complexities of insurance in healthcare, consider reaching out to PEO4YOU to explore your coverage options and safeguard your future.

In recent years, Americans have faced escalating costs for health plans, a trend that shows no signs of abating. A significant factor contributing to this surge is the increasing concentration within the health insurance market. Understanding the dynamics of this concentration, its underlying causes, and its impact on consumers is crucial for navigating the complexities of today’s healthcare landscape.

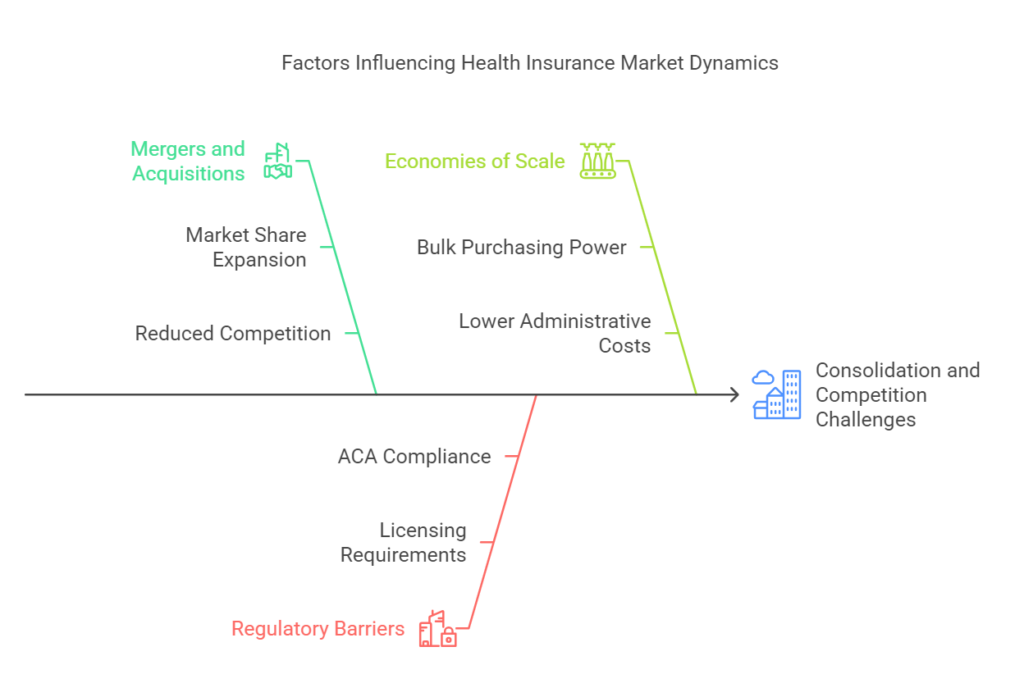

Understanding Market Concentration in Health Insurance

Market concentration occurs when a small number of insurers dominate the market share within a specific region or nationally. This dominance can lead to reduced competition, often resulting in higher premiums and fewer choices for consumers seeking health plans.

Key Factors Driving Market Concentration

Several factors have contributed to the increasing concentration in the health insurance market.

Mergers and Acquisitions

Large insurance companies have merged with or acquired competitors, consolidating market share and reducing the number of independent players.

In 2024, the health insurance industry witnessed significant consolidation through mergers and acquisitions, impacting market dynamics and consumer choices. Notable examples include:

UnitedHealth Group’s Acquisition Attempt of Amedisys: UnitedHealth Group pursued a $3.3 billion acquisition of Amedisys, aiming to expand its home health and hospice services. However, the U.S. Department of Justice filed a lawsuit to block the deal, citing concerns over reduced competition in the sector (The Wall Street Journal)

Sanford Health and Marshfield Clinic Health System Merger: Sanford Health announced plans to merge with Marshfield Clinic Health System, aiming to create an integrated health system with extensive reach. The merger would encompass numerous hospitals, providers, and health plans, further consolidating the market.

Regulatory Barriers

Stringent regulations can deter new entrants from joining the market, limiting competition and innovation in health plan offerings.

Some of the biggest regulatory barriers include:

State and Federal Licensing Requirements – Any new insurance provider must meet extensive licensing and solvency requirements in every state they operate in, making expansion costly.

Capital Reserve Requirements – Insurers must maintain significant cash reserves to pay claims, making it expensive for new players to enter the market.

ACA Compliance Costs – The Affordable Care Act (ACA) imposes strict rules on pricing, coverage, and essential benefits, making it hard for smaller insurers to compete with industry giants.

Rate Approval Processes – Insurers must submit rate increases to state regulators for approval, limiting their flexibility compared to larger firms that can absorb financial losses more easily.

Economies of Scale

Larger insurers benefit from economies of scale, allowing them to operate more efficiently and negotiate better rates with healthcare providers, further entrenching their market position.

These advantages include:

Bulk Purchasing Power – Large insurers negotiate lower rates with hospitals and drug companies because they serve millions of members.

Lower Administrative Costs Per Person – Larger firms can spread their fixed costs (like technology, compliance, and claims processing) over more policyholders, making it cheaper to operate.

Better Risk Pooling – With a larger customer base, major insurers can balance out high-risk patients with lower-risk ones, keeping premiums more stable.

Impact on Health Plan Costs

The concentration of the health insurance market has several implications for the cost of health plans:

Higher Premiums: With reduced competition, dominant insurers have greater pricing power, often leading to increased premiums for consumers.

Limited Plan Options: A concentrated market can result in fewer health plan choices, restricting consumers’ ability to find coverage that best suits their needs.

Decreased Innovation: Less competition may lead to stagnation in the development of new and improved health plan offerings, affecting the quality of coverage available.

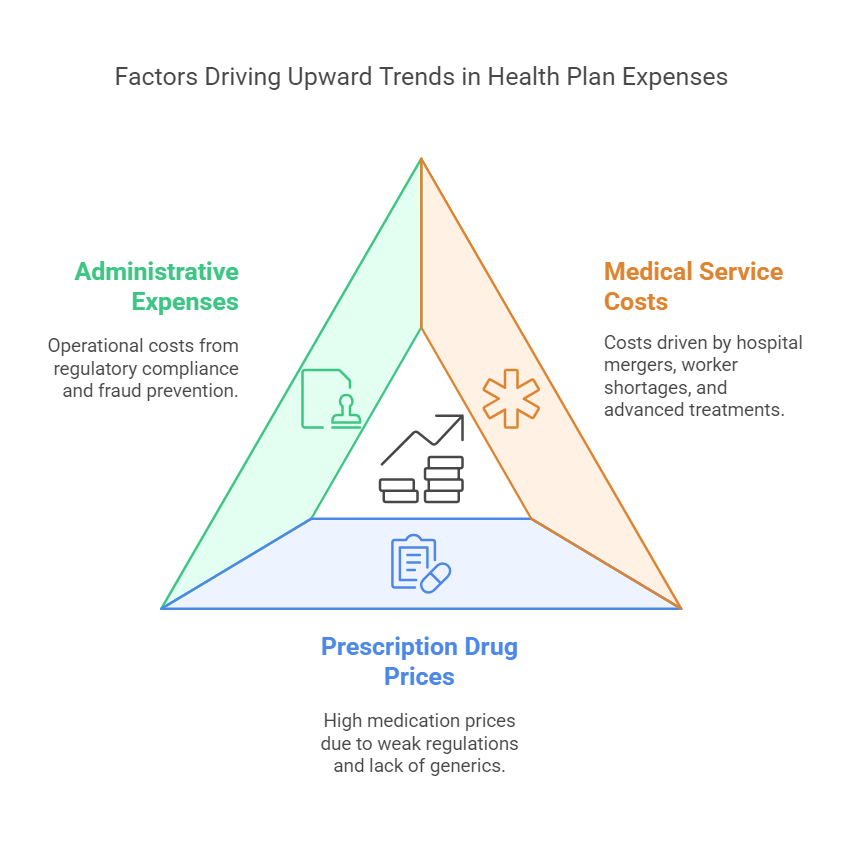

Inflation and Health Plan Costs

Inflation in the healthcare sector further exacerbates the rising costs of health plans. Key contributors include:

Medical Service Costs: Increases in the prices of medical services directly impact the cost of health plans.

Here’s why:

Hospital Mergers – Many hospitals are merging into large networks, reducing competition and allowing them to charge higher prices for services.

Shortages of Healthcare Workers – A growing shortage of doctors, nurses, and specialists means hospitals must pay more for staff, driving up overall costs.

Higher Costs for Advanced Treatments – New medical technologies and specialized treatments are expensive, and hospitals pass these costs onto insurers.

Increased Demand for Services – An aging population and rising chronic disease rates are leading to higher healthcare utilization, putting upward pressure on costs.

Prescription Drug Prices: Rising costs of medications contribute significantly to overall health plan expenses.

Several forces contribute to this trend:

Pharmaceutical Price Control Laws Are Weak – Unlike other countries, the U.S. does not regulate drug prices, allowing manufacturers to set high prices.

Lack of Generic Alternatives – Drug companies extend patents and delay generics from entering the market, keeping costs high.

Middlemen (Pharmacy Benefit Managers) – These third-party companies negotiate drug prices, but they often prioritize higher-cost drugs to secure bigger rebates.

Research and Development Costs – Drug companies justify high prices by pointing to expensive R&D, though many experts argue that profit margins are excessive.

Administrative Expenses: Operational costs, including compliance with regulatory requirements, add to the financial burden on insurers, which is often passed on to consumers.

These regulatory requirements include:

HIPAA Compliance – Protecting patient data requires heavy investment in cybersecurity and compliance measures.

Medical Loss Ratio (MLR) Rules – Insurers must spend a certain percentage of premiums on care, limiting flexibility in pricing and profitability.

Claims Processing & Fraud Prevention – Extensive oversight and fraud detection systems increase administrative expenses.

State-Specific Rules – Insurers must comply with different laws in each state they operate in, requiring additional legal and compliance teams.

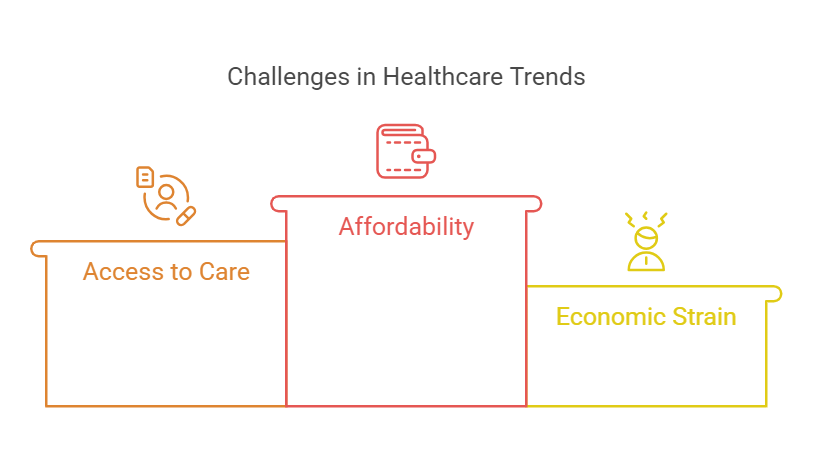

Challenges Posed by Current Trends

The current trajectory presents several challenges:

Affordability: As health plan costs rise, affordability becomes a pressing concern, particularly for low- and middle-income individuals and families.

Access to Care: Higher costs can lead to individuals forgoing necessary medical care, resulting in poorer health outcomes.

Economic Strain: Employers, especially small businesses, may struggle to provide health plans to employees, affecting workforce stability and satisfaction.

Conclusion

The increasing concentration in the health insurance market, coupled with inflationary pressures, poses significant challenges to the affordability and accessibility of health plans. Consumers are left with fewer choices and higher costs, underscoring the need for innovative solutions.

Organizations like PEO4YOU play a pivotal role in this industry. By offering tailored healthcare plans and comprehensive health coverage, PEO4YOU provides valuable alternatives for individuals and businesses seeking quality care without the burden of escalating costs. Their services include:

Customized Healthcare Plans: Designed to meet the unique needs of clients, ensuring optimal coverage.

Comprehensive Health Coverage: Including medical, dental, and vision options to promote overall well-being.

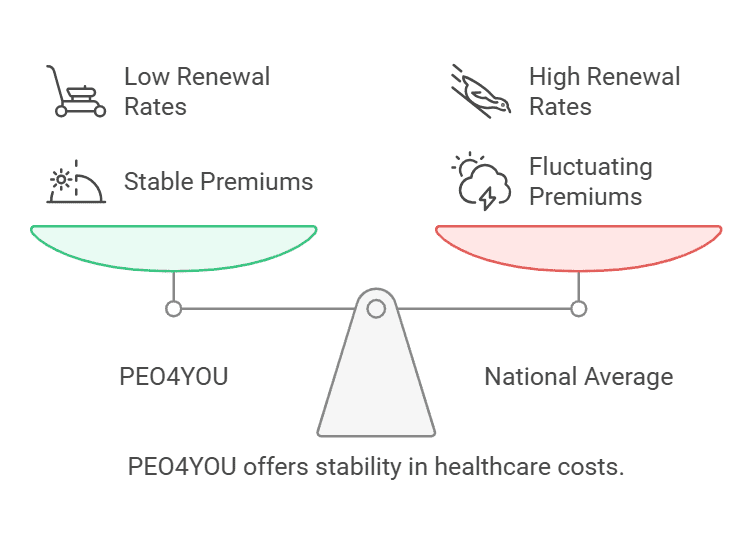

Competitive Pricing and Renewals: Leveraging partnerships to offer cost-effective solutions in a challenging market while providing solutions with a history of low, stable renewal increases.

By exploring options with PEO4YOU, consumers can go through the complexities of the current health insurance market and secure the health coverage plan they need

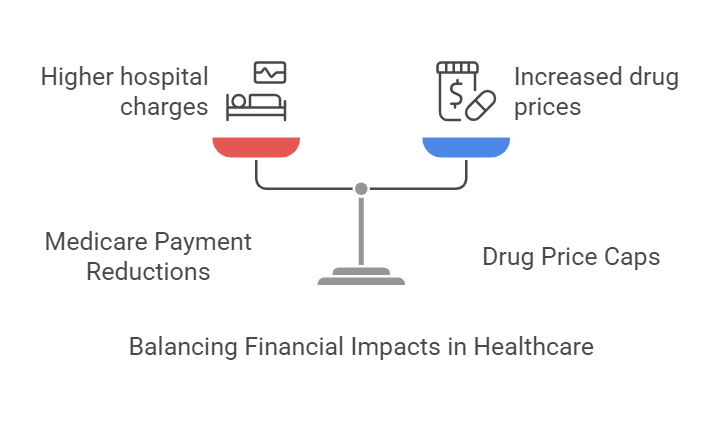

Efforts to lower healthcare costs, such as reducing Medicare-associated expenses or capping drug prices, are often met with praise. However, these actions can sometimes create unintended ripple effects, such as increased costs for the under-65 market or other medications. This article explores the evidence supporting and contradicting this cost-shifting phenomenon, evaluates its implications, and offers alternative solutions to reduce healthcare expenses without causing unintended economic consequences.

Understanding Cost-Shifting in Healthcare

Cost-shifting occurs when healthcare providers or drug manufacturers compensate for lost revenue in one area by increasing prices in another. For example:

Medicare Payment Reductions

When Medicare reduces reimbursement rates, hospitals may charge higher prices to private insurers to offset losses. This practice helps hospitals maintain financial stability, as the average profit margin for hospitals in the U.S. hovers around 8% according to the American Hospital Association (AHA, 2021). Without such adjustments, hospitals risk operating at a loss, potentially leading to closures or reduced services.

Drug Price Caps

Caps on the cost of certain medications may lead manufacturers to increase prices for other drugs or in other markets. Pharmaceutical companies often cite the need to recover significant research and development costs, which can exceed $2.6 billion per drug on average (Tufts Center for the Study of Drug Development, 2020). Without these price adjustments, companies may struggle to fund new innovations or face financial instability.

Evidence Supporting Cost-Shifting

Hospital Pricing Shifts

A study published in Health Affairs found that when Medicare reduced payments by 10%, hospitals increased prices for private insurers by 1.6% (Health Affairs, 2019). This 1.6% increase likely did not fully offset the 10% revenue loss from Medicare.

This practice disproportionately affects individuals with private insurance, as they indirectly subsidize Medicare payment shortfalls.

Drug Pricing Adjustments

A 2020 study by the National Bureau of Economic Research (NBER) revealed that drug manufacturers often respond to price controls in one market by raising prices in markets with fewer restrictions (NBER, 2020).

Example: The introduction of price caps in European markets led to a 25% increase in drug prices in unregulated markets like the United States.

Contradicting Evidence

Limited Ability to Shift Costs

Some experts argue that cost-shifting is overstated. A report from the Medicare Payment Advisory Commission (MedPAC) suggests that competitive market dynamics and insurer negotiations can limit providers’ ability to raise prices for private payers (MedPAC, 2021).

Example: Insurers in highly competitive regions may resist price increases, forcing providers to find operational efficiencies instead.

Market-Specific Dynamics

Cost-shifting is less prevalent in markets where alternative funding mechanisms, such as government subsidies or value-based care models, exist to offset revenue losses.

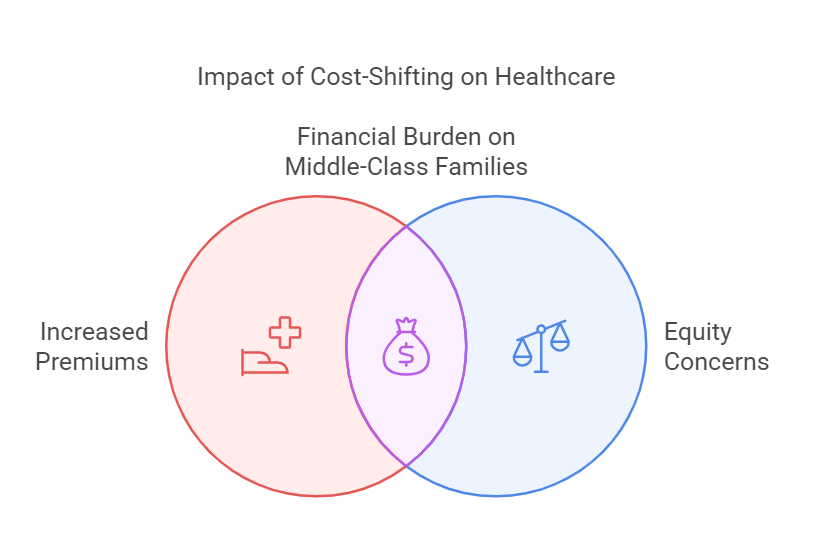

Potential Consequences of Cost-Shifting

Increased Premiums

Cost-shifting leads to higher premiums for the under-65 population, eroding affordability for middle-class families.

Innovation Stifling

Higher prices in non-regulated markets may discourage investment in innovative drug development due to reduced affordability and market access.

Equity Concerns

Cost-shifting exacerbates disparities, as those with private insurance bear a disproportionate financial burden compared to beneficiaries of public programs.

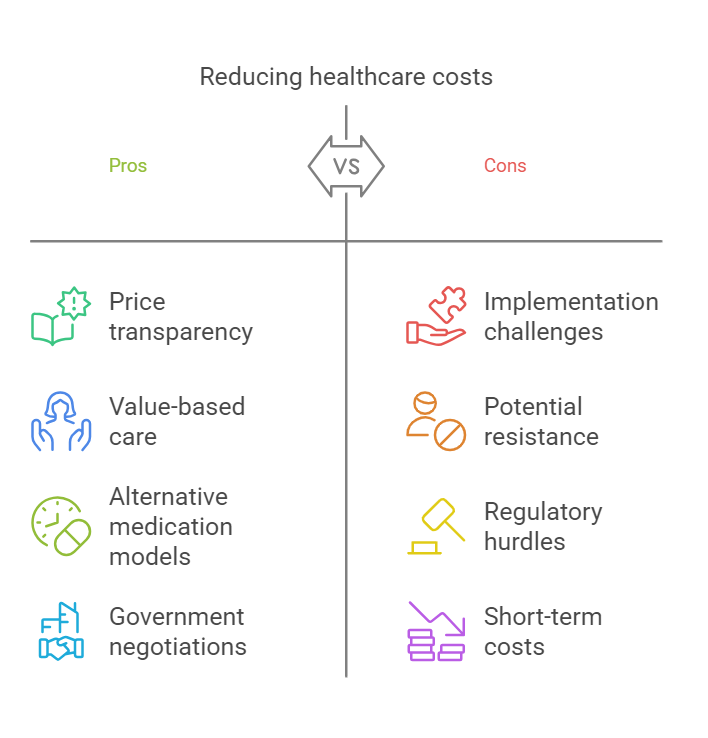

Alternative Solutions to Reduce Healthcare Costs Without Shifting Costs

To avoid the pitfalls of cost-shifting, policymakers and stakeholders can consider the following strategies:

1. Promoting Price Transparency

Transparency initiatives, such as requiring hospitals and drug manufacturers to disclose pricing, empower consumers and insurers to make informed decisions.

Impact: A RAND Corporation study found that transparent pricing could reduce healthcare spending by up to $25 billion annually (RAND, 2021).

2. Expanding Value-Based Care

Shifting from fee-for-service models to value-based care aligns provider incentives with patient outcomes, reducing overall costs.

Example: The Centers for Medicare & Medicaid Services (CMS) reported a 5% reduction in costs and improved outcomes in its value-based purchasing programs (CMS, 2022).

3. Leveraging Alternative Medication Models

CostPlusDrugs.com: This platform offers medications at wholesale prices with a small markup, bypassing traditional price-setting mechanisms.

Employer Programs: Companies like PEO4YOUprovide free or heavily discounted generic medications, reducing reliance on costly insurance plans.

These alternatives can oftentimes reduce medication costs by as much as 80% or more.

4. Government Negotiations and Bulk Purchasing

Allowing Medicare to negotiate drug prices directly with manufacturers can reduce costs without shifting the burden to private payers.

Example: Countries like Canada and the UK successfully control drug prices through government-negotiated bulk purchasing agreements, achieving lower overall costs.

Challenges to Implementing Alternative Solutions

Resistance from Stakeholders

Insurers, hospitals, and pharmaceutical companies may resist transparency or value-based models due to potential revenue losses.

Regulatory Barriers

Complex state and federal regulations often hinder the adoption of innovative pricing and care delivery models.

Operational Complexity

Transitioning to value-based care or transparent pricing requires significant investment in infrastructure and technology.

Conclusion

Reducing Medicare-associated costs or capping drug prices can inadvertently lead to cost-shifting, increasing financial burdens on other markets or populations. While evidence suggests this phenomenon is real, it is not inevitable. By adopting alternative strategies like price transparency, value-based care, and innovative drug pricing models, the healthcare system can reduce costs sustainably without creating new inequities.

The path forward requires collaboration among policymakers, healthcare providers, and private stakeholders. With the right mix of solutions, the U.S. can achieve a healthcare system that prioritizes affordability, equity, and innovation.

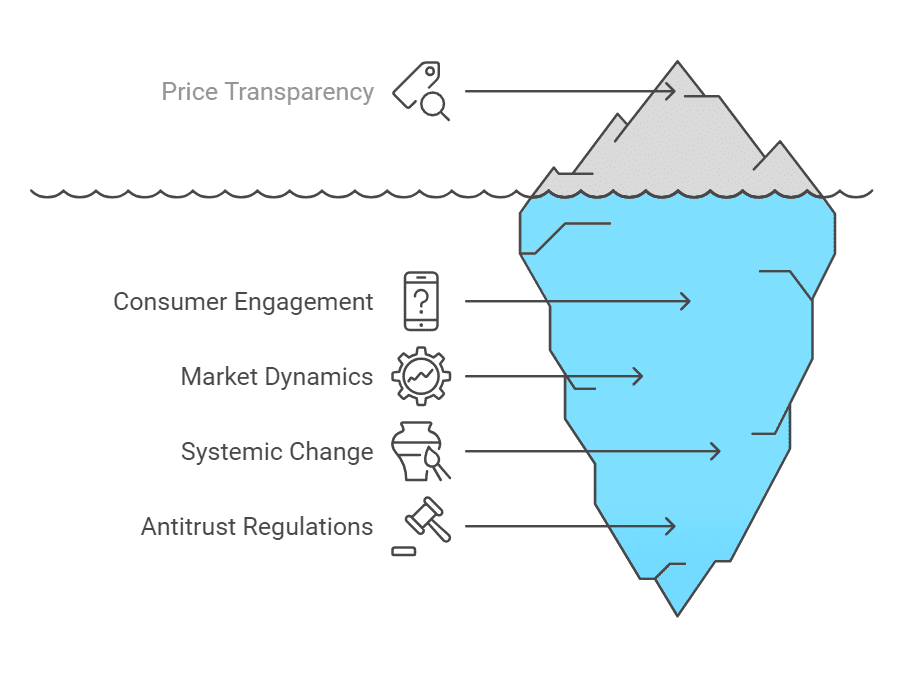

The Problem: Opaque Pricing and Limited Competition

Healthcare in the United States continues to grapple with rising costs and varying quality of care. Unlike other industries that leverage competition and price transparency to boost efficiency, healthcare has struggled to adopt these principles. Integrating competition and transparent pricing could enhance care quality, reduce expenses, and empower patients with better choices. Examples from the U.S. and global healthcare systems underscore the profound impact of these strategies.

The Impact of Opaque Pricing

U.S. healthcare costs is famously unclear and complex. Patients frequently face hidden costs, only learning their expenses post-treatment, which often leads to unexpected financial burdens. Opaque pricing prevents consumers from seeking value and removes pressure on providers to enhance efficiency or quality.

A 2021 study by the RAND Corporation revealed that hospital prices in the U.S. are, on average, 247% higher than Medicare rates (RAND Corporation, 2021, source). A 2024 survey by PwC revealed that 28% of consumers delayed or skipped medical care due to financial constraints, with younger generations, such as Gen Z and millennials, experiencing even greater difficulty.HealthManagement. Without clear pricing, consumers cannot shop for better value, and providers face little pressure to improve efficiency or quality.

The complexity of pricing affects all aspects of the system. For instance, bundled services—such as a hospital stay that includes medications, surgery, and post-operative care—make it difficult for patients to discern how costs are distributed. This opacity further hinders competition because patients cannot easily compare services across providers.

The Role of Competition in Enhancing Quality and Reducing Costs

Competition encourages providers to improve quality and lower prices to attract patients. The generic drug market exemplifies how competition drives down prices while maintaining quality. A 2019 report by the AAM noted that generic drugs saved the U.S. healthcare system $313 billion annually

Case Study: Reference Pricing in California

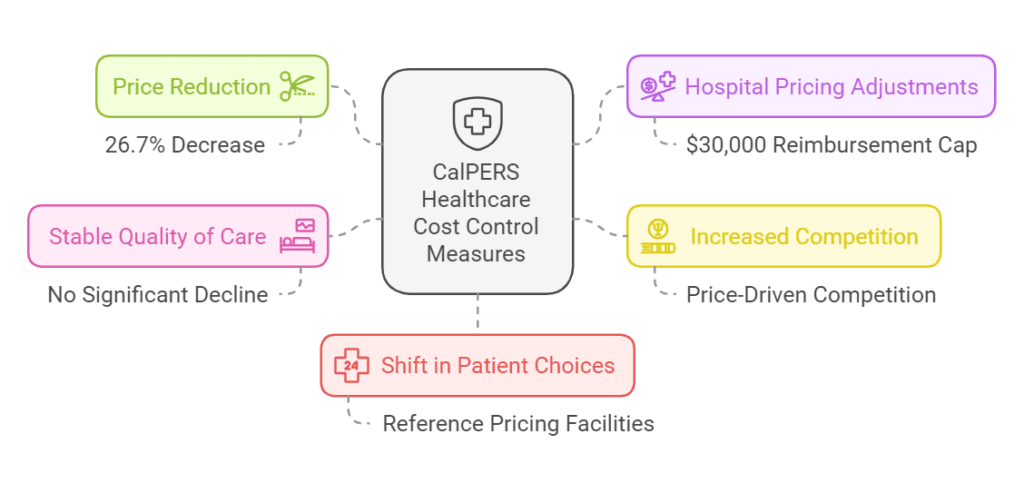

Reference Pricing: Reference pricing is a healthcare payment model where insurers or payers establish a maximum allowable reimbursement rate for specific medical procedures that is generally tied to regional and national averages or a percentage of Medicare rates. In California, the CalPERS initiative implemented this model for hip and knee replacements, compelling hospitals to compete by offering services at or below the set rate. What were the results?

Price Reduction: Average payments for procedures decreased by 26.7% within CalPERS preferred provider organizations (PPOs).

Hospital Pricing Adjustments: Higher-priced hospitals lowered their fees to meet the $30,000 reimbursement cap set by CalPERS.

Increased Competition: Hospitals began competing to offer services at or below the set price, driving overall cost reductions.

Stable Quality of Care: No significant decline in the quality of treatment despite lower costs.

Shift in Patient Choices: More patients opted for facilities adhering to reference pricing, reinforcing market-driven cost control.

This approach demonstrates that price caps can incentivize hospitals to operate more efficiently without compromising patient outcomes. Similar models could be expanded to other procedures and states to create broader cost reductions.

The Impact of Price Transparency on Cost and Quality

Transparent pricing allows patients to compare costs, motivating providers to offer competitive rates without compromising quality.

International Examples of Transparency

Singapore:

Mandated price disclosure for common procedures.

Impact: The introduction of the fee benchmarks has been effective in moderating the growth of private surgeon fees, fostering price transparency, instilling discipline in charging, and helping to moderate increases in fees(MOH).

Singapore’s system not only publishes procedure prices but also ranks providers based on quality metrics. This dual transparency empowers patients to make informed decisions while encouraging hospitals to improve their services to remain competitive.

Australia:

Zable Health created a digital referral system that shows specialist fees, out-of-pocket costs and waiting periods to meet demands for increased transparency.

Outcome: The platform revealed significant variations in specialist fees, with initial consultations ranging up to $950. By providing detailed cost information, the platform aims to empower patients and encourage specialists to offer more competitive pricing.

Employer Innovations: Walmart’s Centers of Excellence (COE) program stands out as an innovative example of employer-driven transparency and competition. By directly contracting with high-quality hospitals and healthcare providers, Walmart bypasses traditional insurance intermediaries to offer its employees specialized care. Through this program, employees receive certain procedures, such as back surgeries, at little to no out-of-pocket cost, with Walmart covering bundled payments directly negotiated with providers.