Access to hospital services is one of the most critical aspects of health insurance coverage. A well-structured medical plan ensures that individuals and families can receive essential hospital care without facing crippling financial burdens. This article explores how health insurance covers hospital services, the types of plans offering the most comprehensive coverage, challenges faced by hospitals, and how health insurance plays a role in addressing those challenges.

Intermediaries like PEO4YOU simplify the process of finding the right medical plan by connecting individuals and businesses with the best health care options tailored to their needs.

Hospital services encompass a wide range of care, including emergency room visits, inpatient care, surgeries, maternity services, and specialized treatments. According to a 2024 report by the American Hospital Association (AHA), hospital care accounted for nearly 30% of all U.S. healthcare expenditures, highlighting its importance in health coverage.

A good medical plan ensures access to:

Inpatient care refers to medical treatments provided when a patient is admitted to a hospital for at least one night. This includes services like:

Why it Matters: Inpatient care often involves significant costs, making it essential for a medical plan to offer comprehensive coverage to reduce financial strain.

Outpatient care involves medical procedures or consultations that do not require an overnight stay in a hospital. These include:

Why it Matters: Outpatient care is often more cost-effective than inpatient services, and most modern medical plans offer extensive coverage for these services to promote preventive care and early treatment.

Emergency care addresses urgent medical conditions that require immediate attention to prevent severe health outcomes. Common scenarios include:

Why it Matters: Under the Affordable Care Act (ACA), medical plans are required to cover emergency services without preauthorization, even if the hospital is out-of-network.

Specialized care focuses on advanced or complex medical conditions requiring unique expertise or technology. Examples include:

Why it Matters: Specialized treatments often come with high costs, but they are crucial for patients managing life-threatening or long-term illnesses. Comprehensive medical plans ensure these services are accessible and affordable.

Example: A 2023 study by the Kaiser Family Foundation revealed that 80% of employer-sponsored health plans offer full inpatient coverage but vary in outpatient benefits, depending on the plan type.

Emergency care is a cornerstone of health insurance. By law, under the Affordable Care Act (ACA), all health plans must cover emergency services without requiring preauthorization, regardless of whether the hospital is in-network.

Many hospital stays require medications, which are typically covered under the prescription drug benefits of a medical plan. Comprehensive plans ensure that these costs are either partially or fully reimbursed.

Mental health services are increasingly recognized as essential. Modern medical plans include coverage for psychiatric hospitalizations and substance abuse treatments, aligning with the Mental Health Parity and Addiction Equity Act.

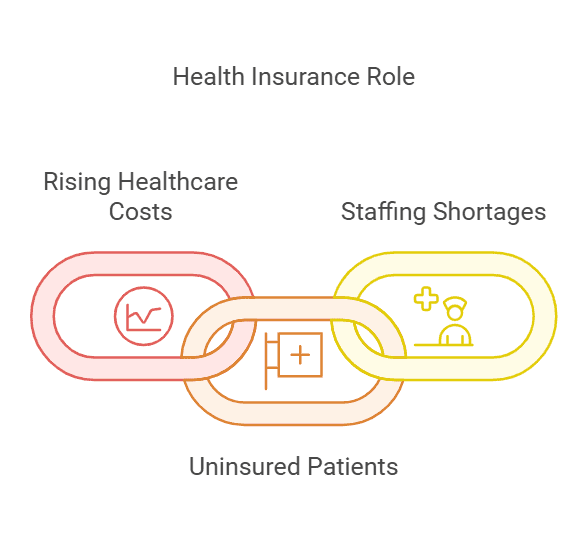

Hospitals face significant financial pressure due to increasing operational costs, including advanced medical technologies, specialized staff, and regulatory compliance. According to a 2024 Commonwealth Fund report, hospitals saw a 7% rise in operational costs in 2023 alone.

Health insurance helps mitigate this by ensuring patients can afford care. Plans with robust hospital coverage reduce instances of unpaid medical bills, a common issue for uninsured patients.

Hospitals often absorb the costs of treating uninsured individuals. In 2023, the American Hospital Association reported $42 billion in uncompensated care, underscoring the critical role of health insurance in alleviating financial strain on healthcare providers.

A shortage of healthcare professionals affects hospital efficiency and care quality. Comprehensive medical plans that include wellness programs can help address this issue by keeping patients healthier and reducing hospital admissions.

A well-designed medical plan is essential for accessing comprehensive hospital services, from emergency care to specialized treatments. As hospitals face challenges like rising costs and uninsured patients, health insurance plays a crucial role in bridging the gap between patient needs and healthcare providers' capabilities.

By partnering with experts like PEO4YOU, individuals and businesses can find the best health plan options, ensuring that hospital services are accessible, affordable, and tailored to their unique needs. Trust PEO4YOU to guide you in choosing the right plan, because medical plan coverage is not just about affordability—it’s about securing the care you deserve.

April 19, 2026

April 19, 2026

April 20, 2026

April 20, 2026

Recent Posts

April 20, 2026

April 20, 2026

April 19, 2026

April 19, 2026

April 18, 2026

April 18, 2026

Get In Touch— We’re available 24/7

"*" indicates required fields

“We respect your privacy. Your contact information will be used solely for the purpose of responding to your inquiry and will not be shared with third parties.”

Click To Open Modal

Get In Touch— We’re available 24/7

"*" indicates required fields

“We respect your privacy. Your contact information will be used solely for the purpose of responding to your inquiry and will not be shared with third parties.”

Thanks!

We will be in touch soon.

If you're looking to book a consultation now

Affordable health and benefits plans for small businesses, freelancers, and independent contractors.

Copyright © 2026. Peo4you. All rights reserved.