You signed with a PEO to make HR easier. Instead, you’ve become the unofficial HR department — fielding benefits questions your PEO rep won’t answer, manually enrolling employees because the portal doesn’t work, and spending hours each week on tasks the PEO was supposed to handle.

If this sounds familiar, you’re not alone. When to switch PEO providers is one of the most common questions we hear from employers who chose their PEO based on price alone and are now paying for it in operational headaches. The good news: switching is more straightforward than most PEOs want you to believe.

- A PEO that won’t speak directly with your employees is shifting its workload to you

- Manual benefit enrollment in 2026 is a platform failure, not a “process difference”

- Cancellation fees ($5,000-$10,000) typically pay for themselves within 4-6 months of switching

- Month-to-month contracts with 30-day notice exist — long-term lock-ins aren’t necessary

- The real cost of a bad PEO is measured in management hours, not just fees

Warning Sign #1: Your PEO Won’t Talk to Your Employees

This is the most telling red flag. A PEO’s core value proposition is that it handles HR, benefits, and payroll so your team doesn’t have to. When your PEO reps refuse to speak directly with employees — forcing managers to relay questions about claims, coverage, or enrollment — the entire model breaks.

In our experience working with a financial services firm that was evaluating a switch, the operations manager had become a full-time benefits intermediary. Every employee question about insurance claims, prescription coverage, or enrollment changes went through him because the PEO’s reps wouldn’t take employee calls directly.

The operational cost was staggering: an estimated 10+ hours per week of management time spent on tasks the PEO was being paid to handle. At a loaded management rate, that’s $30,000-$50,000 annually in hidden costs that never appear on the PEO invoice.

A properly structured PEO provides a dedicated benefits coordinator who handles employee inquiries directly — freeing management to focus on revenue-generating activities. If your PEO can’t offer this, it’s time to explore PEO health insurance options for small businesses that include direct employee support.

Warning Sign #2: Benefits Enrollment Is Still Manual

In 2026, paper-based benefits enrollment is inexcusable. Yet we regularly encounter PEOs where employees must complete enrollment forms by hand, HR must manually enter I-9 documents, and benefits changes require phone calls and faxes.

When to switch PEO providers often comes down to this: if the platform your employees interact with daily doesn’t work, nothing else matters. The financial services firm we worked with had a benefits portal that was technically “available” but functionally broken — employees couldn’t complete enrollment online, and the system didn’t mandate required document uploads during onboarding.

A modern PEO platform should provide online self-service enrollment with mandatory document upload flows, automated onboarding workflows that track completion in real-time, a QuickBooks or accounting system integration that eliminates manual payroll data entry, and commission or variable pay import capabilities for complex compensation structures.

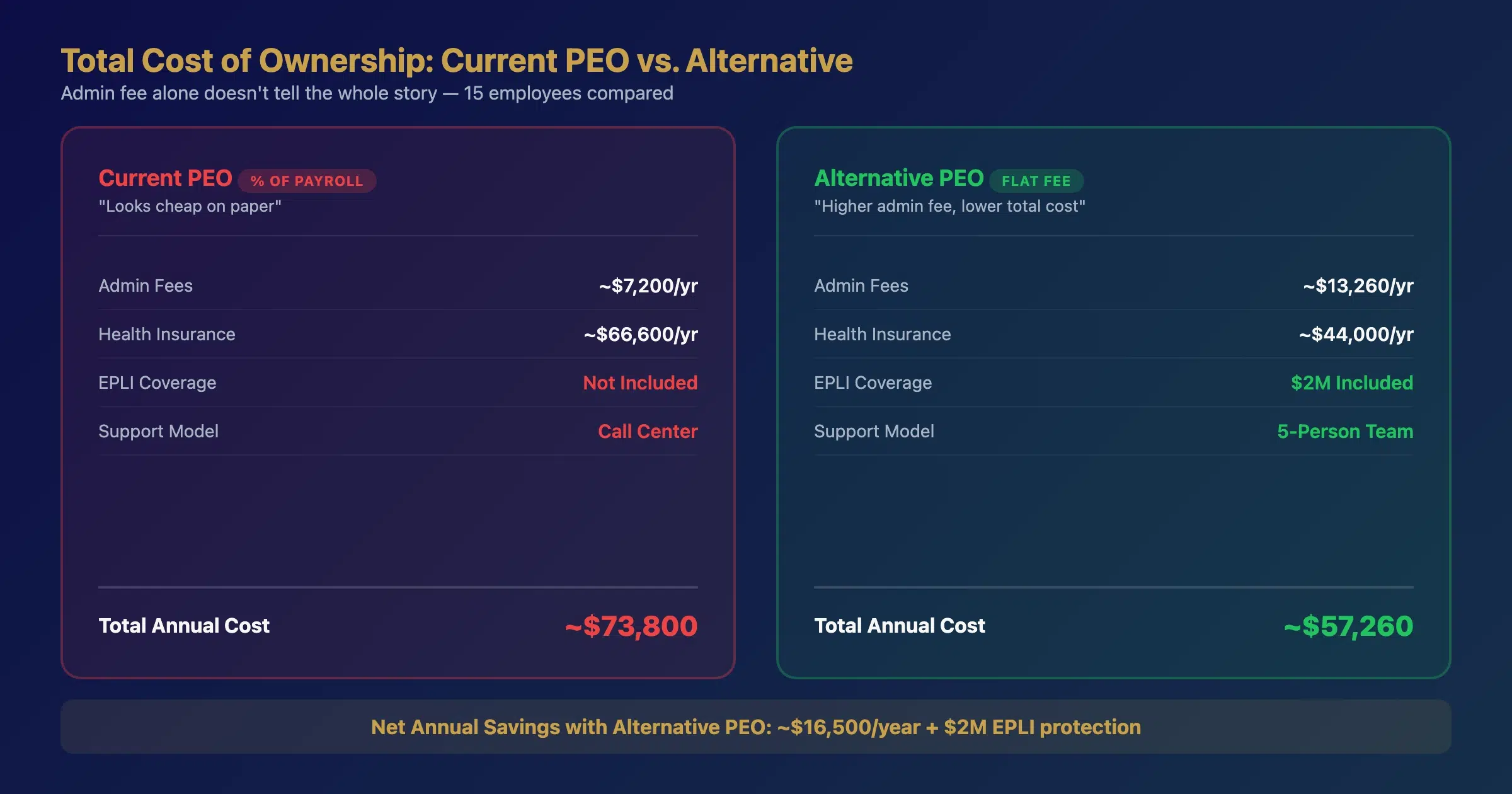

Warning Sign #3: Your Admin Fees Keep Climbing Without Added Value

PEO admin fees should reflect the value of services delivered. If your per-employee costs have increased 10-15% over two years without corresponding improvements in service, technology, or benefits, you’re subsidizing the PEO’s overhead — not paying for better outcomes.

When we build benefits savings strategies for employers evaluating a switch, the admin fee comparison often reveals the largest opportunity. Here’s a real comparison we modeled:

| Cost Category | Current PEO (% of payroll) | Alternative PEO (flat fee) | Impact |

|---|---|---|---|

| Admin fees (15 employees) | ~$7,200/year ($40/mo/ee) | ~$13,260/year ($17/wk/ee) | +$6,060 more |

| Health insurance (15 employees) | ~$66,600/year | ~$44,000/year | -$22,600 savings |

| EPLI coverage | Not included | $2M included | Risk reduction |

| Dedicated support team | Call center | 5-person team | Quality upgrade |

| Net annual impact | ~$16,500 savings |

The higher admin fee purchased dramatically more value: lower insurance costs, EPLI protection (average defense costs run $75,000-$125,000 per claim according to industry data), and a dedicated five-person service team. What looked like a “cheap” PEO was actually the most expensive option when total cost of ownership was calculated.

Warning Sign #4: You’re Locked Into a Long-Term Contract

Multi-year PEO contracts with substantial cancellation fees are a business model choice — they exist to create switching friction, not to serve your interests. If your PEO requires a 12-24 month commitment with a $5,000-$10,000 early termination penalty, ask why.

The financial services firm we worked with faced a $7,500 cancellation fee from their current provider. The initial reaction was that the fee made switching unaffordable. But when we ran the full analysis, the projected savings from switching were approximately $48,000 annually — meaning the cancellation fee paid for itself in under 10 weeks.

The right question isn’t “can I afford to leave?” It’s “can I afford to stay?”

Month-to-month PEO contracts with 30-day notice periods exist. They signal that the PEO is confident enough in its service to earn your business every month, rather than trapping you contractually. If your PEO won’t offer this flexibility, consider how traditional group health insurance compares as an alternative structure.

Warning Sign #5: Your Payroll Takes Too Long and Errors Are Common

When running a payroll report takes 10 minutes of processing time, or when commission entries require manual data input that introduces errors every cycle, your PEO’s technology infrastructure isn’t meeting basic standards.

Payroll should be fast, accurate, and integrated. Modern PEO platforms offer spreadsheet-based commission imports (eliminating manual entry errors), real-time payroll processing, and bi-directional accounting system sync. If your current PEO can’t deliver these fundamentals, it’s not a technology limitation — it’s a platform investment choice that tells you where you fall on their priority list.

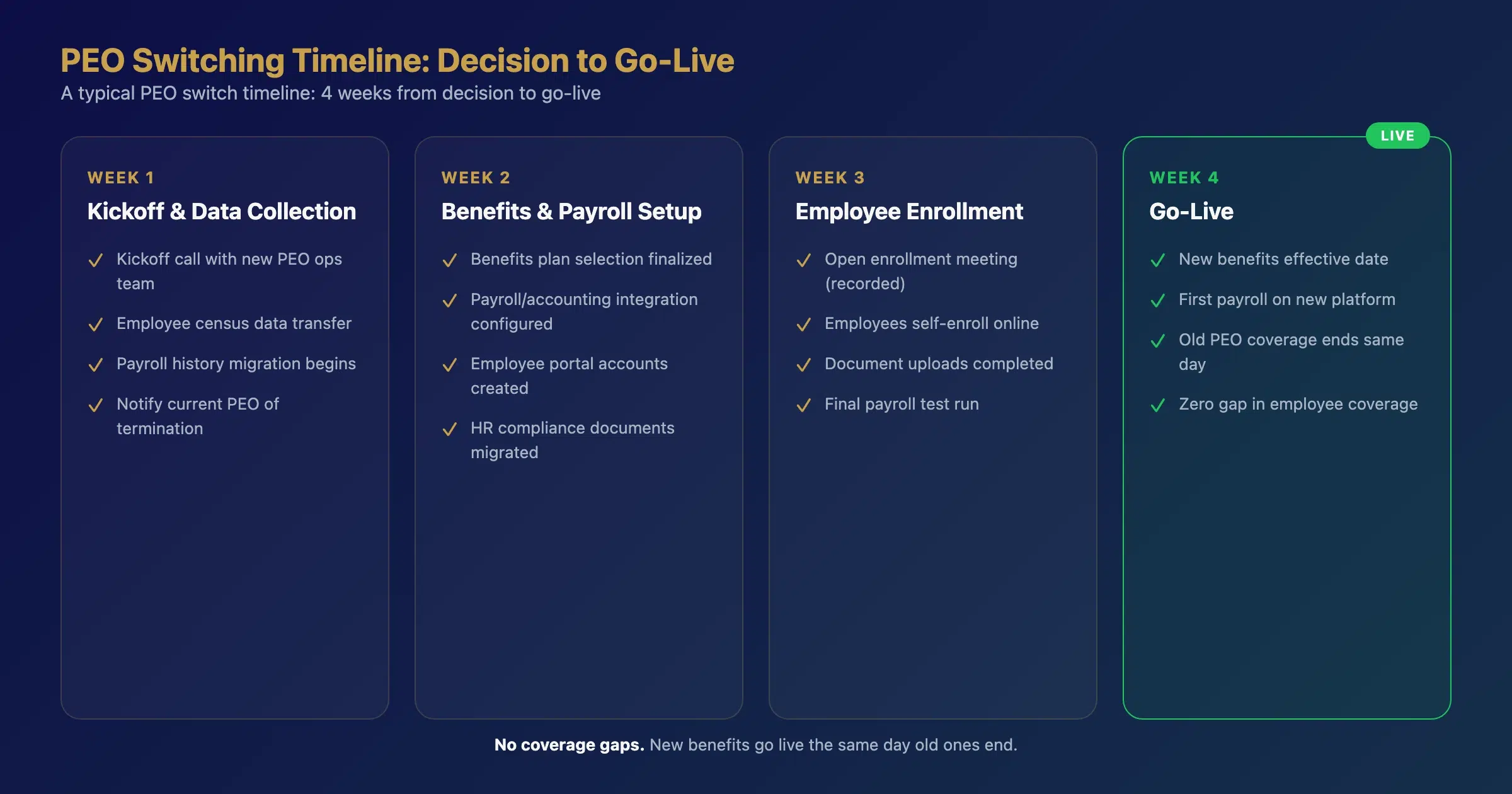

What Switching Actually Costs (and Saves)

The fear of switching PEOs is almost always worse than the reality. Here’s what a typical transition timeline looks like:

- Weeks 1-2: Kickoff calls for payroll/operations and benefits

- Weeks 2-3: Open enrollment meeting for employees (recorded for those unavailable)

- Week 4: Benefits effective date on the new platform

The most common concern — “my employees will lose coverage during the transition” — is addressed through coordinated effective dates. Your new PEO’s benefits go live on the same day the old ones end.

Use the Benefits ROI Calculator to model your total cost comparison before initiating conversations. Having clear numbers transforms the discussion from emotional to analytical.

If you’re spotting multiple warning signs in your current PEO relationship, the next step is understanding whether PEO honeymoon rates influenced your original decision — and how to avoid the same pattern in your next choice.

Frequently Asked Questions

How long does it take to switch PEO providers?

A typical PEO transition takes 3-4 weeks from decision to go-live. This includes kickoff calls, data migration, employee enrollment, and benefits activation. Larger groups (50+ employees) may need 4-6 weeks. The key is coordinating effective dates so there’s no gap in coverage.

Will my employees lose benefits during a PEO switch?

No, when managed properly. The new PEO coordinates a benefits effective date that aligns with your current plan’s termination date. Employees experience a seamless transition — often with improved benefits and the same or better provider networks.

What does a PEO cancellation fee typically cost?

PEO cancellation fees range from $2,000 to $15,000 depending on company size and contract terms. However, most employers who switch to a better-fit PEO recover the cancellation fee in savings within 2-6 months. The fee should be evaluated against projected annual savings, not in isolation.

Can I keep my current 401(k) provider when switching PEOs?

In most cases, yes. Modern PEOs support integrations with major 401(k) providers through 180-degree or 360-degree APIs. During the evaluation process, confirm that the new PEO can integrate with your specific plan administrator to automate contribution tracking and reporting.

What should I look for in a construction company benefits package when evaluating PEOs?

For construction and trade businesses, prioritize workers’ comp integration (pay-as-you-go billing), E-Verify compliance support, multi-class benefits eligibility (different tiers for field vs. office staff), and a PEO with experience in your industry’s specific OSHA and DOL requirements.

If you want to calculate whether switching makes financial sense for your business, the Benefits Savings Strategy Builder walks you through a comprehensive comparison — including cancellation fees, implementation costs, and projected savings.

About the Author: Sam Newland, CFP®, has spent 13+ years in the employee benefits industry and founded Business Insurance Health and PEO4YOU to bring transparency to an industry that profits from complexity. His approach is simple: show employers the real numbers and let them decide.