Nonprofit organizations face a unique challenge: delivering maximum impact for their mission while operating under tight budget constraints. Yet many nonprofits unknowingly drain precious resources through inefficient benefits administration riddled with broker errors, manual processes, and hidden costs that compound over time.

A Massachusetts nonprofit administrator managing two organizations with approximately 80 employees recently shared her frustration with persistent enrollment errors from their current broker. Misspelled names, missed dependents, and former employees lingering on invoices month after month created an administrative nightmare that consumed hours of valuable time better spent on mission-critical work. The situation became so overwhelming that the organization had to hire an HR Generalist at $60,000 to $70,000 annually just to regain administrative capacity.

This scenario plays out across the nonprofit sector, where limited staff and resources make every hour and every dollar count. According to the Bureau of Labor Statistics, nonprofit organizations employ 12.8 million people, representing 9.9 percent of all private sector jobs.1 However, Independent Sector research shows that 22% of nonprofit employees earn below the ALICE threshold and struggle financially,2 making efficient benefits administration crucial for both employee wellbeing and organizational sustainability.

Key Takeaways

- Nonprofit HR teams can lose an estimated 200 to 400 hours annually to broker enrollment errors and manual corrections

- Benefits administration costs average $24 per employee per month with disconnected systems and high error rates

- The Administrative Burden Audit helps nonprofits quantify hidden costs and identify improvement opportunities

- Professional Employer Organizations can reduce administrative costs by $450 per employee annually

- 53% of nonprofits are expanding in 2025, making efficient benefits administration increasingly critical

The Hidden Cost of Benefits Administration Errors

Most nonprofit leaders focus on visible costs like premium increases or new benefit additions. However, the administrative burden of managing benefits errors often represents a larger drain on organizational resources than the benefits themselves. Industry research shows that benefits administration costs average $24 per employee per month when using disconnected systems, with error rates significantly higher during open enrollment periods.3

These errors manifest in multiple ways that compound over time. Enrollment mistakes require hours of detective work to identify and correct. Former employees remaining active on plans create ongoing premium charges that may go unnoticed for months. Dependent eligibility errors can trigger compliance issues or expensive retroactive corrections. Each error generates a cascade of administrative work that pulls staff away from mission-focused activities.

Common Broker Error Patterns

Through extensive work with nonprofit organizations, certain patterns emerge repeatedly:

- Data entry mistakes: Misspelled names, incorrect birthdates, and transposed Social Security numbers that delay coverage activation

- Dependent enrollment errors: Missing spouse or child additions, incorrect effective dates, and eligibility verification failures

- Termination processing delays: Former employees remaining active on plans for weeks or months after departure

- Plan selection mistakes: Employees enrolled in wrong coverage levels or benefit options despite clear election forms

- Billing discrepancies: Charges for terminated employees, incorrect premium calculations, and missing discounts or credits

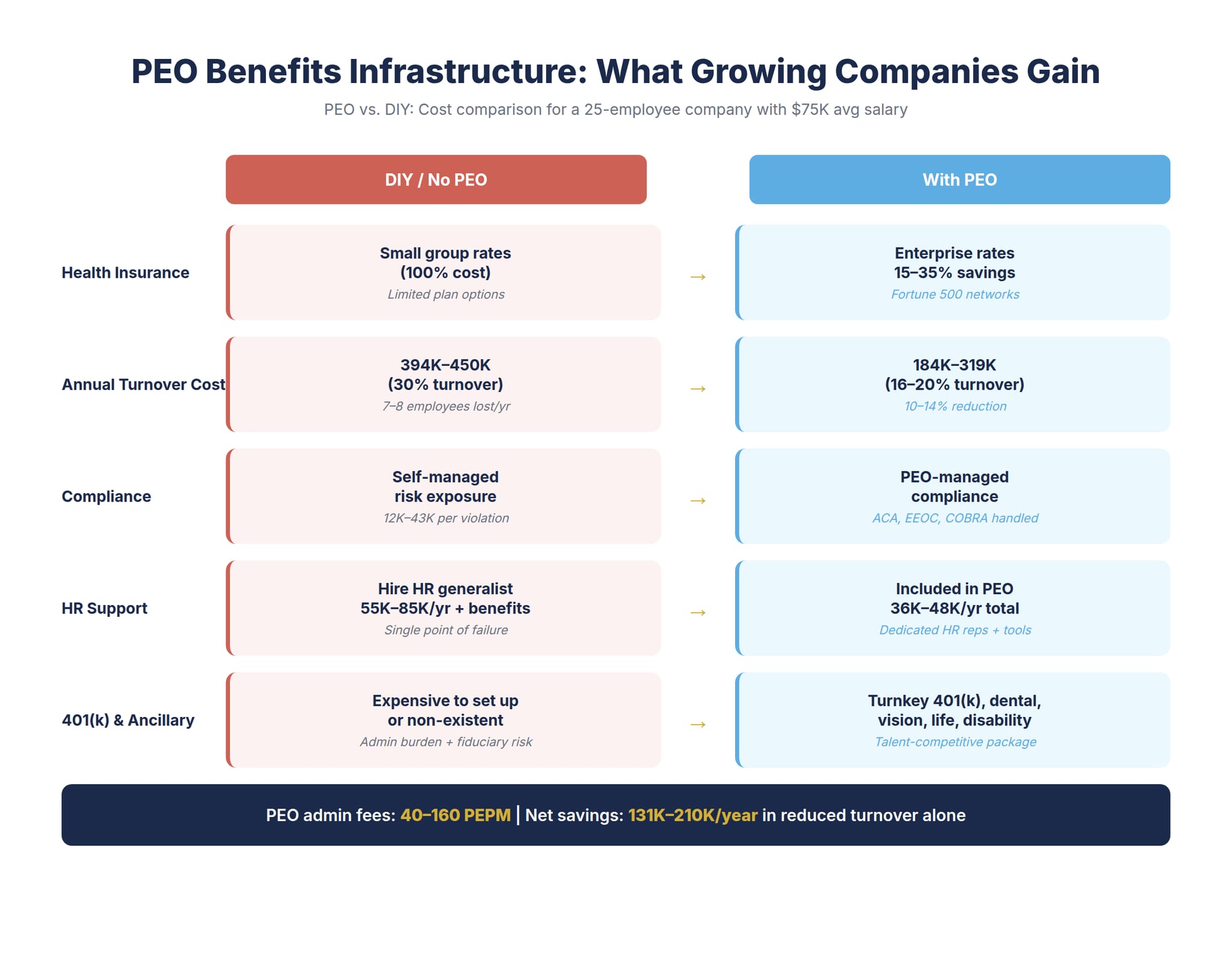

The National Association of Professional Employer Organizations research indicates that companies using professional services can reduce HR administrative costs by approximately $450 per employee annually,4 largely by eliminating these types of recurring errors and the administrative burden they create.

Introducing The Administrative Burden Audit

To help nonprofits quantify the true cost of benefits administration inefficiencies, we developed The Administrative Burden Audit, a systematic framework for measuring hidden costs and identifying improvement opportunities. This audit examines six key areas where broker errors typically drain nonprofit resources:

Time Tracking Assessment

The first component measures actual staff hours spent on benefits-related administrative tasks. Most nonprofits dramatically underestimate this burden because the work happens in small increments throughout the year rather than concentrated blocks.

Weekly Time Categories:

- Enrollment error corrections and follow-up communications

- Billing discrepancy investigations and resolution

- Employee questions about coverage or claim issues

- Vendor communication and status updates

- Manual data entry and verification processes

A dual-organization HR administrator typically spends 8 to 12 hours weekly on these activities during active periods and 4 to 6 hours during maintenance periods, totaling 300 to 450 hours annually. At a loaded cost of $35 to $50 per hour for HR staff time, this represents $10,500 to $22,500 in annual administrative costs before considering benefits.

Error Frequency Analysis

The second component tracks specific error types and their resolution time. Organizations with inefficient brokers typically experience an estimated 12 to 24 enrollment errors per year per 100 employees, with each error requiring 2 to 8 hours to resolve depending on complexity.

High-performing benefits administration systems, including those offered through PEO health coverage solutions, typically reduce error rates to 2 to 4 per year per 100 employees while providing dedicated support to resolve issues quickly.

The True Cost of Manual Processes

Beyond error correction, manual benefits administration creates ongoing inefficiencies that compound over time. Open enrollment becomes a months-long ordeal of paper forms, data entry, and verification rather than a streamlined digital process.

SHRM research shows that benefits offerings have increased 23% in recent years, from 175 available options to 216 different benefit types.5 This expansion creates additional complexity for nonprofits managing benefits manually, as each new option requires separate enrollment tracking, vendor coordination, and ongoing administration.

Scalability Challenges

Robert Half research indicates that 53% of nonprofit employers are expanding their teams in 2025.6 Growing organizations quickly discover that manual benefits processes do not scale efficiently. Adding new employees becomes increasingly complex as benefit options multiply and compliance requirements expand.

Organizations that rely on manual processes often reach a tipping point around 40 to 60 employees where the administrative burden becomes overwhelming. This is precisely when many nonprofits begin exploring comprehensive employee benefits solutions that provide both cost savings and administrative relief.

Financial Impact Beyond Administration

While administrative costs represent the most visible burden, broker errors create additional financial impacts that many nonprofits overlook:

Premium Leakage

Terminated employees remaining on active status create direct premium charges that can persist for months. A terminated employee with family coverage costing $1,500 monthly represents $18,000 in annual premium leakage if not caught quickly. Across an 80-employee organization, just 2-3 such errors annually can cost $5,000 to $10,000 in unnecessary premiums.

Compliance Risk

Benefits enrollment errors can trigger compliance violations that carry financial penalties. Incorrect dependent eligibility, missed COBRA notifications, or improper plan changes can result in Department of Labor fines ranging from $1,000 to $10,000 per violation. For cash-strapped nonprofits, these penalties represent a significant unbudgeted expense.

Employee Relations Impact

Independent Sector research shows that 40% of nonprofits say their employee benefits positively impact workforce recruiting and retention, while 25% report that insufficient benefits negatively affect their ability to attract and retain staff.7 Benefits administration errors undermine these positive impacts by creating employee frustration and distrust.

When employees experience coverage gaps, billing issues, or claim denials due to enrollment errors, they lose confidence in the organization’s ability to provide reliable benefits. This erosion of trust can contribute to turnover, which costs nonprofits an estimated 50% to 200% of an employee’s annual salary in replacement costs.

Technology Solutions and Automation

Modern benefits administration technology addresses many common error sources through automation and integrated data systems. However, not all technology solutions provide equal value for nonprofit organizations.

Automated systems can handle repetitive tasks with precision and efficiency, reducing the burden on HR staff and minimizing the risk of errors.8 Key features that provide the greatest impact for nonprofits include:

- Real-time enrollment validation that catches errors before submission

- Integrated payroll deduction calculations that eliminate manual data entry

- Automated termination processing that removes employees from all benefits simultaneously

- Electronic forms and signatures that reduce processing time and improve accuracy

- Centralized employee data that eliminates duplicate entry across multiple systems

Organizations considering technology upgrades should evaluate solutions based on total cost reduction rather than just software pricing. A system that costs $15 per employee monthly but eliminates 200 hours of administrative work provides significantly more value than a $5 per employee solution that only addresses basic enrollment.

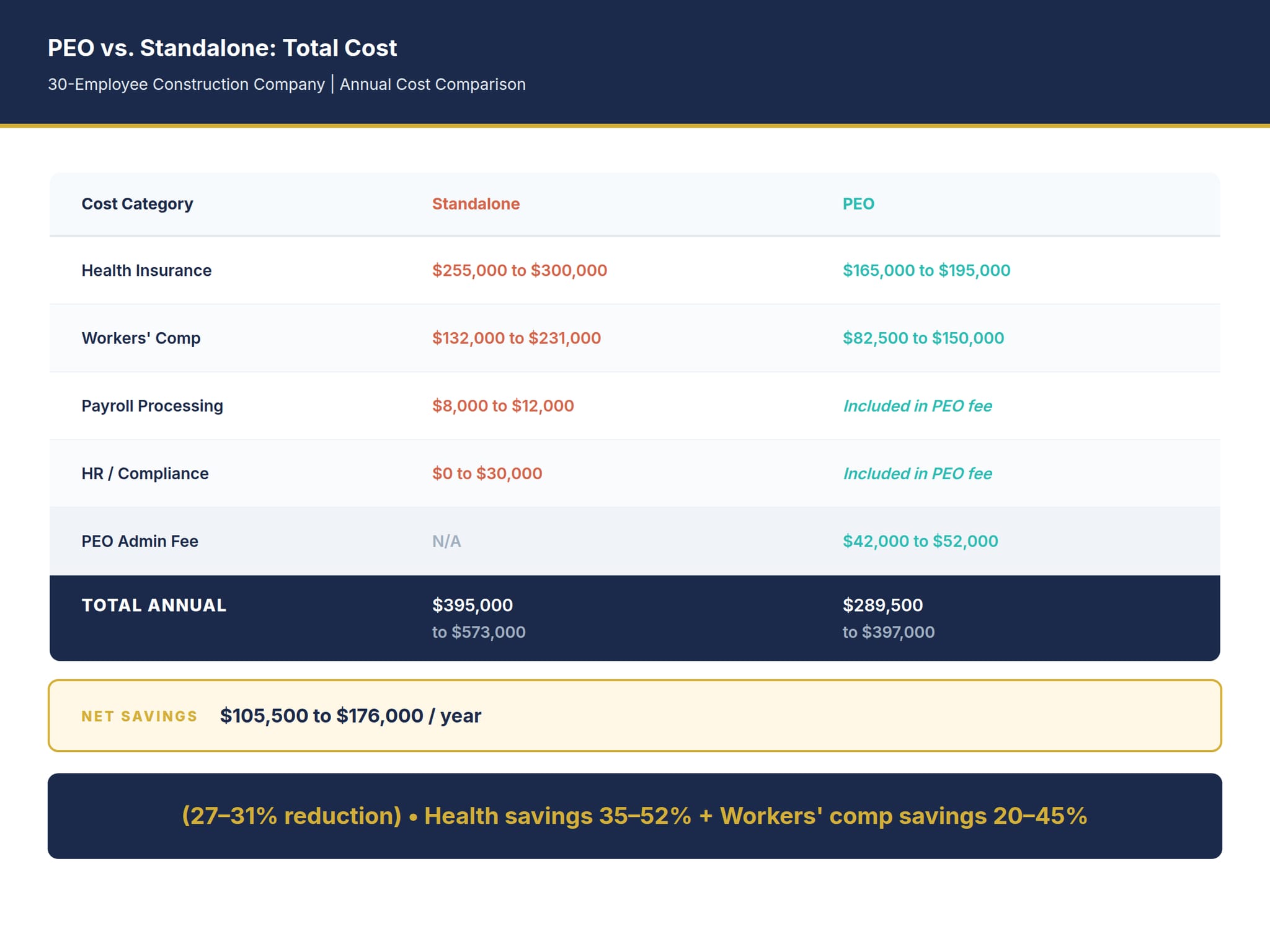

Professional Employer Organization Benefits

For many nonprofits, partnering with a Professional Employer Organization represents the most comprehensive solution to benefits administration challenges. PEOs provide access to Fortune 500-level benefits packages while handling all administrative functions through dedicated support teams.

NAPEO research demonstrates that companies using PEOs experience a 27.2% annual return on investment,9 largely driven by reduced administrative costs and improved operational efficiency. For nonprofits, this translates to more resources available for mission-critical activities.

Comprehensive Support Model

Unlike traditional brokers who primarily focus on plan selection and renewal, PEOs provide year-round administrative support including:

- Dedicated account management with nonprofit sector expertise

- Real-time enrollment processing and error prevention

- Integrated payroll and benefits administration

- Employee self-service portals that reduce HR inquiries

- Compliance monitoring and automatic updates for regulatory changes

For organizations concerned about nonprofit health coverage costs, PEOs often provide access to larger risk pools and better rates than organizations can obtain independently, particularly for smaller nonprofits with fewer than 100 employees.

Benefits ROI Calculator

See how your nonprofit’s benefits spending compares. Quantify the return on 42 different benefit types using 9 institutional data sources.

No login required. No email gate. Free.

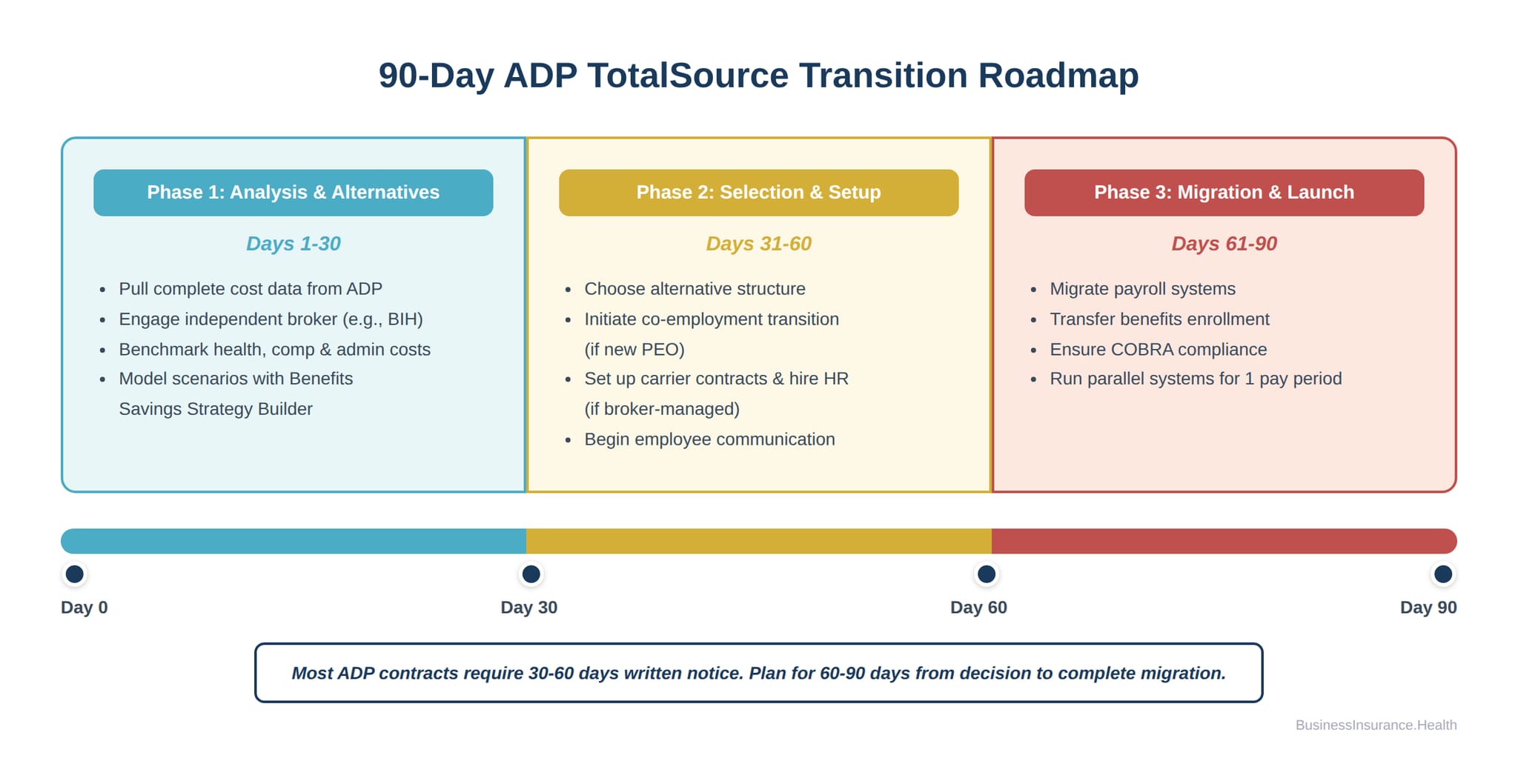

Implementation Strategy for Nonprofits

Transitioning from inefficient benefits administration to streamlined processes requires careful planning and realistic timeline expectations. Most nonprofits can complete this transition within 90 to 120 days with proper preparation.

Assessment Phase

Begin with a comprehensive Administrative Burden Audit to establish baseline metrics. Document current processes, error rates, and time investments to create a clear picture of improvement opportunities. This data becomes essential for evaluating potential solutions and measuring success post-implementation.

Key Assessment Questions:

- How many hours does your team spend weekly on benefits administration?

- What types of errors occur most frequently with your current broker?

- How long does it typically take to resolve enrollment or billing issues?

- Are there former employees still appearing on benefit invoices?

- How satisfied are employees with current benefits communication and support?

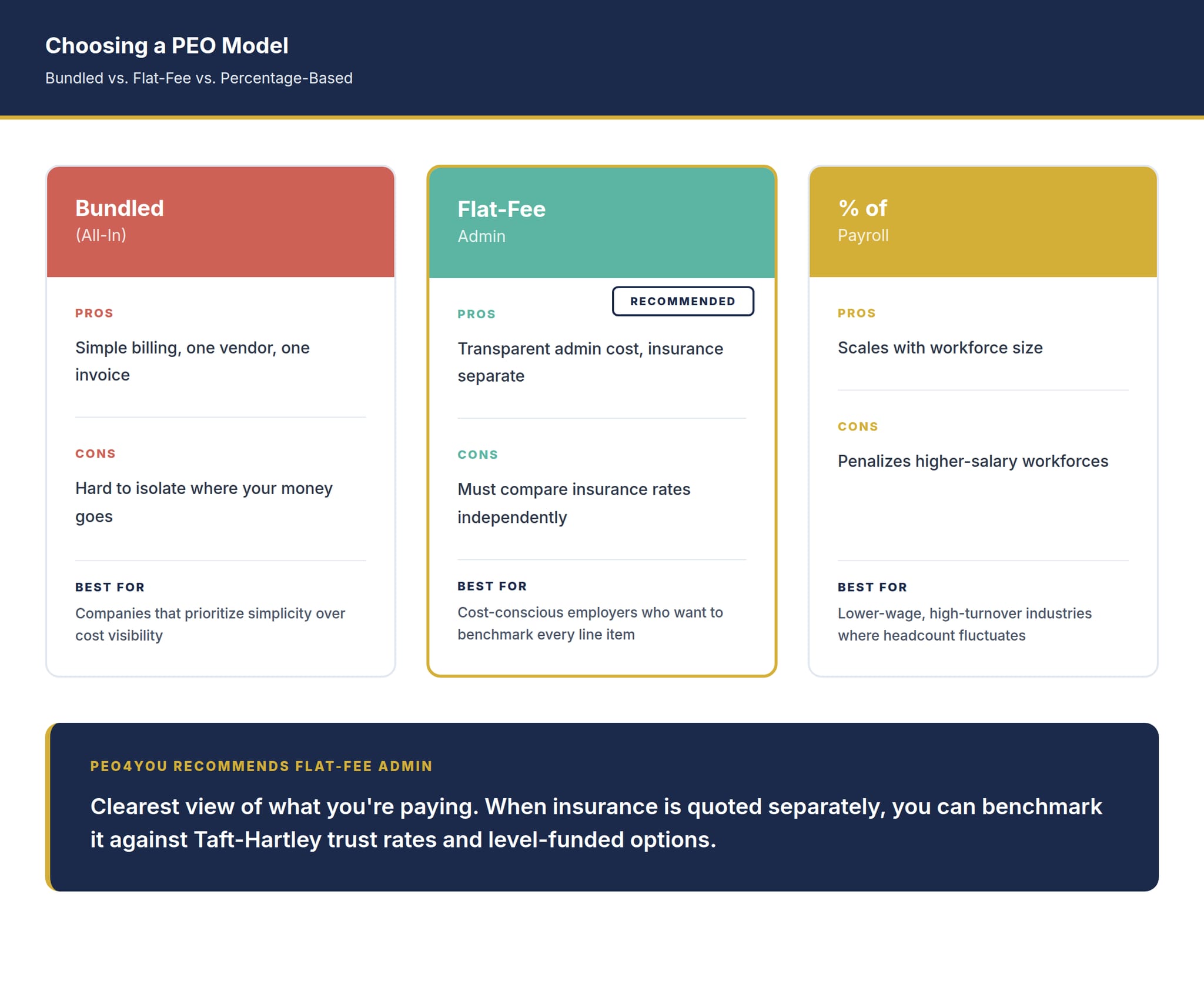

Vendor Evaluation Criteria

When evaluating potential benefits administration partners, nonprofits should prioritize service quality and error prevention over purely cost considerations. The cheapest option often creates the highest long-term costs through administrative burden and mistakes.

Look for providers that demonstrate:

- Specific experience serving nonprofit organizations

- Dedicated account management and customer service teams

- Technology platforms designed to prevent common enrollment errors

- Transparent reporting on error rates and resolution times

- Integration capabilities with existing payroll and HR systems

Measuring Success and ROI

Successful benefits administration improvements should deliver measurable results within the first enrollment period. Track key performance indicators to validate that changes are delivering expected value.

Primary Success Metrics

- Administrative time reduction: Target 50% to 70% reduction in HR hours spent on benefits tasks

- Error rate improvement: Aim for fewer than 5 enrollment errors annually per 100 employees

- Issue resolution speed: Most problems should resolve within 24 to 48 hours rather than weeks

- Employee satisfaction: Track improvements in benefits-related employee survey scores

- Cost per employee: Total benefits administration costs should decrease despite service improvements

Organizations that implement comprehensive solutions typically see administrative time reductions of 300 to 400 hours annually, equivalent to $10,500 to $20,000 in staff cost savings. Combined with reduced errors and improved employee satisfaction, these improvements often deliver 200% to 300% return on investment within the first year.

Future-Proofing Nonprofit Benefits

As the nonprofit sector continues evolving, benefits administration must adapt to changing workforce expectations and regulatory requirements. Organizations that invest in scalable solutions today position themselves for sustainable growth tomorrow.

Emerging trends affecting nonprofit benefits administration include:

- Increased demand for flexible and voluntary benefit options

- Growing emphasis on mental health and wellness programs

- Remote work considerations affecting coverage and administration

- Enhanced compliance requirements and reporting obligations

- Integration expectations with other HR technology platforms

By addressing current administrative inefficiencies while selecting solutions that accommodate future growth, nonprofits can ensure that benefits management supports rather than hinders their mission-focused work.

For organizations ready to explore comprehensive benefits solutions, resources are available to compare small business health coverage options and evaluate total cost of ownership rather than just premium expenses.

Frequently Asked Questions

Q: How long does it typically take to fix benefits enrollment errors?

A: Simple errors like name corrections may resolve in 24 to 48 hours, while complex issues involving dependent eligibility or plan changes can take 1 to 3 weeks. Organizations with professional administration support typically resolve most issues within 1 to 2 business days.

Q: What should nonprofits budget for benefits administration costs?

A: Industry benchmarks suggest $15 to $30 per employee per month for comprehensive benefits administration. However, total cost should include internal HR time, which often represents the largest expense component.

Q: Can small nonprofits with fewer than 50 employees benefit from professional administration?

A: Yes, smaller organizations often see the greatest proportional benefit since they typically lack dedicated HR staff to handle complex benefits administration. Professional services can provide expertise and efficiency that smaller organizations cannot develop internally.

Q: How do nonprofits measure the ROI of improved benefits administration?

A: Track time savings, error reduction, and employee satisfaction improvements. Most organizations see 200% to 300% ROI within 12 months through reduced administrative burden and fewer costly mistakes.

Q: What happens during the transition to a new benefits administration system?

A: Professional transitions typically take 60 to 90 days and include data migration, employee communication, training, and parallel processing to ensure no coverage gaps occur. Experienced providers handle most transition complexity.

References

- U.S. Bureau of Labor Statistics. “Nonprofit Sector Research Data.” BLS, 2025. bls.gov/bdm/nonprofits

- Social Current. “Navigating Workforce Challenges: 2025 Trends and Solutions for the Social Sector.” Social Current, February 2025. social-current.org

- Lift HCM. “The Hidden Costs of Using Multiple HR, Payroll, and Benefits Systems.” Lift HCM, August 2025. lifthcm.com

- Axcet HR Solutions. “PEO Cost Considerations: Is It Worth the Investment?” Axcet HR, October 2025. blog.axcethr.com

- SHRM. “Employee Benefit Trends for 2025.” SHRM, August 2025. shrm.org

- Robert Half. “Employment Trends Spotlight: Nonprofit Industry.” Robert Half, June 2025. roberthalf.com

- Independent Sector. “New Report Shows Nonprofits Are Being Squeezed by Growing Community Need and Fewer Resources.” Independent Sector, December 2025. independentsector.org

- Navia Benefit Solutions. “6 Common Challenges in Benefit Administration Services & How to Overcome Them.” Navia Benefits, December 2025. naviabenefits.com

- NAPEO. “The ROI of Using a PEO.” National Association of Professional Employer Organizations, March 2025. napeo.org

About the Author

Sam Newland, CFP®, is the founder of Business Insurance Health (BIH). With over 13 years of experience in employee benefits and a background as the former #1 face-to-face health coverage agent nationally, Sam helps employers with 30-200+ employees navigate complex funding strategies including PEO, self-funded, captive, level-funded, and Taft-Hartley arrangements. Contact: [email protected] | 857-255-9394

This article is educational and does not constitute professional financial, legal, or benefits advice. Nonprofit organizations should consult with qualified benefits consultants and legal counsel to evaluate strategies appropriate for their specific size, state, and workforce.