What Does PEO Stand For?

Getting a Grasp of What a PEO Entails

Small businesses up to 100 employees (5-50 employees tends to be the sweet spot) can benefit from working with a Professional Employer Organization (PEO), which offers a range of HR services such as managing payroll and tax filings, along with ensuring compliance and providing group health insurance and benefits coverage for employees. By teaming up with a PEO as an employer partner, small businesses can access cost-effective health insurance options that are typically more difficult to secure without such collaboration.

Understanding PEO Health Plans for Employees

When your company partners with a Professional Employer Organization (PEO), your employees gain access to healthcare benefits that might typically be out of reach for smaller businesses. But how does this work? Let’s break it down.

Collaborative Advantage

A PEO extends the concept of co-employment, which means it merges your employees with those from other businesses into one large employee pool. This collective group allows the PEO to negotiate better rates and benefits with insurance providers.

Benefits to Employees

- Access to Premium Plans: With a large group acting as one entity, insurance providers can offer high-quality health plans at a rate smaller providers can’t typically secure.

- Economies of Scale: Because of the pooled risk among many employees, the cost of insurance is spread out, resulting in more affordable premiums for high-tier plans.

- Risk Mitigation: The large pool buffers any single employee’s claims, which can lead to more stable rates over time.

Financial Feasibility

These competitive rates and robust benefit options often directly translate to significant savings for both employers and employees. Smaller companies can offer attractive health benefits without the prohibitive costs usually associated with top-tier plans.

By joining forces with a PEO, your employees not only receive valuable health coverage but also enjoy the same advantages typically reserved for larger corporations.

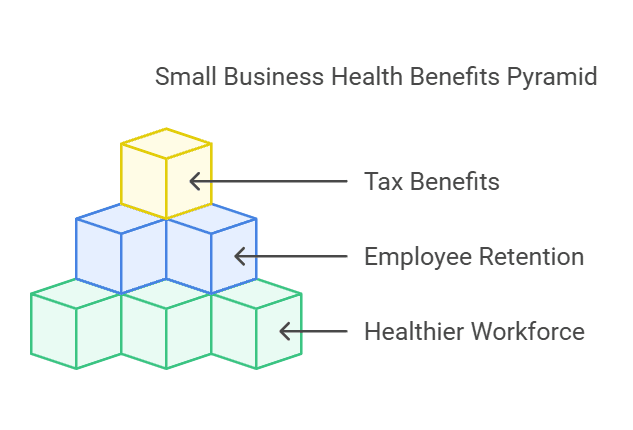

The Importance of PEO Health Insurance for Small Businesses

Health insurance offered by PEOs is incredibly beneficial for small businesses facing challenges in offering top-notch health coverage because of high premiums. PEOs negotiate with health insurers to secure better rates by combining employees from client companies under their umbrella. This approach leads to lower costs and improved coverage options for all involved. As a result of this arrangement, even small businesses with a small number of employees can provide their workforce with comprehensive health insurance packages. In a competitive job market, providing such perks can enhance your company’s appeal to highly skilled professionals.

Advantages of PEO Health Insurance

Efficiency in Cutting Costs: The Strength of Collective Purchasing

One major benefit of PEO health insurance is the savings on costs it offers by using the combined purchasing power of all its clients to negotiate rates for group health coverage and ancillary benefits, resulting in more budget-friendly rates for employees than what small businesses could secure independently. For instance, a study conducted by the National Association of Professional Employer Organizations (NAPEO) revealed that companies utilizing PEO services save an average of 35% on healthcare expenses.

Access to Comprehensive Health Insurance Plans

Professional Employer Organizations (PEOs) provide a range of health insurance options, such as coverage for vision care services that often come with broader networks and enhanced benefits than what small businesses can typically obtain on their own. Collaborating with a PEO enables businesses to offer comprehensive health insurance plans that encompass healthcare services, wellness initiatives, and the opportunity to connect with top-notch healthcare providers.

Efficient Administration and Assistance with Regulatory Compliance

Providing health insurance involves plenty of paperwork tasks like overseeing employee enrollments and ensuring adherence to healthcare regulations. PEO services cover all the duties related to providing health insurance. This helps small business owners save time and stay compliant with laws like the Affordable Care Act (ACA) and new state regulations such as required employees trainings, minimizing the chances of facing penalties and fines.

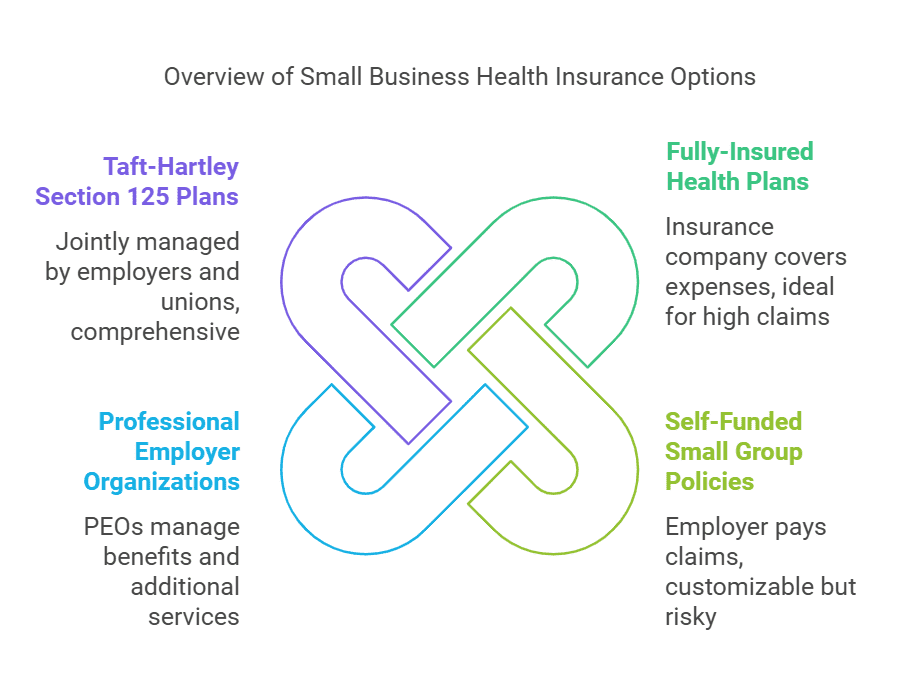

Essential Elements of a PEO Health Insurance Package

Different Options for Insurance Coverage

Health insurance packages for employees can differ, but they usually consist of:

- Health Insurance: Includes coverage for appointments with doctors/hospitals and emergency care, along with preventive services.

- Dental Insurance: Coverage for check-ups, cleanings, and treatments such as fillings or root canals.

- Vision Insurance: Coverage for eye examinations, prescription glasses, and contact lenses.

- Life and Disability Insurance: Provides financial security for employees in the event of disability or death.

Small businesses find PEO group health insurance appealing as it offers comprehensive coverage for their employees’ well-being and healthcare needs.

PEO Health Insurance Rates

PEO health insurance rates for employees are often lower because of the combined risk and purchasing leverage of the PEO entity involved in the process. The rates are influenced by factors like company size, coverage options selected, as well as employee health conditions. On average, PEO health insurance plans tend to be 10 to 20 percent cheaper than plans acquired directly by businesses.

What Is the Difference Between a PEO and a Staffing Company?

Understanding the distinction between a Professional Employer Organization (PEO) and a staffing company is crucial for businesses seeking the right type of employment support. Both entities can assist in managing a workforce but serve distinct roles and functions.

PEOs: Partners in Employment

A PEO functions as a co-employer, sharing responsibilities with your business. This means they handle various HR duties, including:

- Payroll processing: They manage payroll administration and ensure compliance with tax regulations.

- Benefits administration: PEOs often provide access to comprehensive employee benefits, such as health insurance and retirement plans, that might be otherwise costly for smaller businesses.

- Compliance support: They assist with navigating complex employment laws and regulations, minimizing compliance risks.

By partnering with a PEO, companies can leverage the expertise of seasoned HR professionals, allowing them to focus on core business activities while ensuring efficient HR management.

Staffing Companies: Providers of Talent

A staffing company, on the other hand, primarily focuses on recruiting and placing employees. They are ideal for businesses needing:

- Temporary staff: Quickly filling short-term needs for projects or seasonal work.

- Permanent placements: Finding suitable candidates for long-term positions, often involving extensive screening and interviewing processes.

- Specialized talent: Accessing niche skill sets or industry-specific experts that might not be easily found internally.

While staffing companies manage the recruitment process, the hiring business remains the sole employer of the recruited staff, taking on HR responsibilities once a candidate is placed.

Key Takeaways

- Employment Relationship: PEOs co-employ your staff, sharing HR tasks, while staffing companies simply supply candidates.

- Scope of Services: PEOs offer a wide range of HR services, whereas staffing firms focus predominantly on recruitment and placement.

- HR Administration: PEOs provide ongoing HR support, allowing businesses to concentrate on strategic initiatives, while staffing companies offer a quick solution to immediate employment needs.

Choosing between a PEO and a staffing company depends on your business needs. If you seek comprehensive HR solutions and risk management, a PEO might be the best fit. For rapid recruitment and flexible staffing, a staffing company could be the right choice.

How to Ensure Your PEO Partnership Adapts to Your Business Needs

To ensure that a Professional Employer Organization (PEO) partnership continues to meet your evolving business needs, regular communication is key. Here’s how to maintain a successful collaboration:

- Schedule Consistent Check-ins: Establish a routine for reviewing the partnership’s performance. This allows you to assess whether the PEO is aligning with your goals and can address potential issues early.

- Clearly Define Expectations: Begin with a detailed outline of your company’s short-term and long-term objectives. Sharing these with your PEO ensures they understand your strategic direction and can adjust their services accordingly.

- Solicit Employee Feedback: Gather insights from your team about the PEO’s performance. Employees can provide valuable perspectives on HR services, which can highlight areas that need improvement or confirm that the PEO is on track.

- Stay Informed About Industry Trends: Be aware of both industry advancements and changes in employment law that could impact your HR needs. This knowledge enables you to have informed discussions about service updates or modifications.

- Leverage Analytics and Reports: Use the data and performance reports provided by the PEO to make evidence-based decisions. Analyzing these metrics helps in gauging the partnership’s effectiveness and pinpointing areas that need attention.

- Flexibility to Change: If your current PEO isn’t meeting expectations, be prepared to explore other options. There are numerous PEOs with varied specializations, ensuring a match for your specific needs.

Utilizing these strategies not only aligns your PEO partnership with your business’s current needs but also supports its growth and adaptation over time.

How Can a Business Obtain Workers’ Compensation Through a PEO?

Navigating workers’ compensation insurance can be a daunting task for many businesses. However, partnering with a Professional Employer Organization (PEO) offers a seamless approach to managing this obligation. Here’s how you can secure workers’ compensation through a PEO:

- Research and Select a Suitable PEO:

- Begin by identifying PEOs that offer workers’ compensation solutions tailored to your industry.

- Evaluate their reputation, client reviews, and the range of services they provide.

- Understand the Co-Employment Relationship:

- When you enter into an agreement with a PEO, you share certain employment responsibilities. This is known as co-employment.

- The PEO assumes responsibility for managing payroll, benefits, and workers’ compensation, while you maintain control over day-to-day business operations.

- Review and Negotiate the Agreement:

- Go over the service agreement carefully before signing.

- It should outline the specifics of the workers’ compensation coverage, including claims management and premium rates.

- Leverage the PEO’s Buying Power:

- Since PEOs manage multiple clients, they have greater negotiating power with insurance carriers. This can lead to more competitive rates for workers’ compensation insurance.

- Streamlined Claims Management:

- A PEO typically handles claims processing and risk management, ensuring that workers’ compensation claims are managed efficiently.

- This can help reduce downtime and administrative burdens on your team.

- Benefit from Regulatory Expertise:

- PEOs stay updated with changing regulations and compliance requirements, ensuring your business meets all legal obligations related to workers’ compensation.

Why Choose a PEO for Workers Compensation?

- Cost Efficiency: Potential for reduced insurance premiums due to PEO’s pooling of multiple businesses.

- Expert Administration: Professional handling of claims and risk management.

- Compliance Assurance: Regular updates and adherence to regulations without you needing to track changes constantly.

By collaborating with a PEO, your business can streamline the workers’ compensation process, allowing you to focus on core operations while ensuring your employees are covered effectively.

Understanding a Co-Employment Agreement with a PEO

A co-employment agreement with a Professional Employer Organization (PEO) is a collaborative arrangement designed to streamline management tasks and enhance your business operations.

When you enter into this agreement, the PEO becomes the employer of record for your workforce. This means they handle critical responsibilities like payroll processing, tax compliance, and benefits administration. Consequently, your employees receive paychecks and tax documents under the PEO’s name.

However, it’s important to note that you retain complete control over the core functions of your business. Decisions related to daily operations, employee tasks, and strategic direction remain solely in your hands. By sharing administrative duties, you can focus more on growth and less on paperwork.

In summary, a co-employment agreement allows you to benefit from the expertise and resources of a PEO, while maintaining full authority over how your company operates.

Understanding Co-Employment vs. Employee Leasing

In the realm of workforce management, co-employment and employee leasing often get confused, but they represent different forms of business relationships.

Co-Employment

Co-employment involves a partnership typically seen in Professional Employer Organizations (PEOs). Here’s how it works:

- Shared Responsibilities: Both the PEO and the client company share employer responsibilities. The PEO handles HR duties such as payroll, benefits administration, and regulatory compliance. Meanwhile, the client company retains day-to-day oversight and control of the employees’ tasks and roles.

- Employee Focus: Employees are effectively working for both the client company and the PEO, but remain under the client company’s direct supervision for their everyday activities.

- Benefits: The client company benefits from the PEO’s expertise in managing HR functions, allowing it to focus on its core business activities while potentially offering better benefits to employees.

Employee Leasing

Employee leasing is a different scenario, often associated with staffing agencies. Here’s the breakdown:

- Transfer of Employees: In this setup, employees are technically employed by the leasing agency, not the client company. The staffing agency leases these employees to the client for a specified period.

- Control and Supervision: While the employees work at the client company’s site, the leasing agency retains control over employment-related aspects, such as hiring, discipline, and termination. The client company directs the employees’ daily work.

- Temporary Nature: Employee leasing is usually short-term and often caters to project-based work or temporary staffing needs.

Key Differences

- Employment Status:

- Co-Employment: Employees are co-employed by the client and the PEO.

- Employee Leasing: Employees are technically employed by the leasing agency.

- Responsibility Sharing:

- Co-Employment: Shared HR responsibilities between the client and PEO.

- Employee Leasing: Most employment responsibilities lie with the leasing agency.

- Duration:

- Co-Employment: Long-term partnership focused on ongoing business operations.

- Employee Leasing: Typically short-term, fulfilling immediate workforce needs.

Understanding these distinctions helps businesses choose the right strategy for their staffing and HR needs. Co-employment suits organizations seeking continuous support and shared HR functions, while employee leasing caters to temporary or project-based staffing requirements.

Challenges Small Businesses Often Face with Health Insurance Options

High Costs and Limited Variety

Small businesses face a major hurdle in securing health insurance due to the high costs involved and their lack of negotiating leverage compared to larger companies. PEO health insurance offers a solution by providing cost-effective coverage that small businesses may not have access to otherwise.

Tasks That Involve Paperwork and Red Tape

Managing health insurance internally involves a lot of administrative work. Dealing with paperwork and ensuring compliance with healthcare regulations takes up significant time for business owners and distracts them from their primary business operations. Professional Employer Organizations (PEOs) help ease this workload by handling tasks such as employee enrollments and compliance issues, so that business owners can dedicate their attention to growing their business and improving productivity.

PEO4YOU – A Unique PEO

Flexible Payroll and Workers Compensation Requirements

PEO4YOU is unique among Professional Employer Organizations because it doesn’t mandate businesses to switch their payroll provider or workers’ compensation policy like most other PEOs do. This flexibility enables business owners to keep their existing payroll system and workers’ compensation policy without any interruptions while also enjoying the excellent health benefits, such as dental and vision plans, provided by PEO4YOU.

Stable Costs and Predictable Renewals

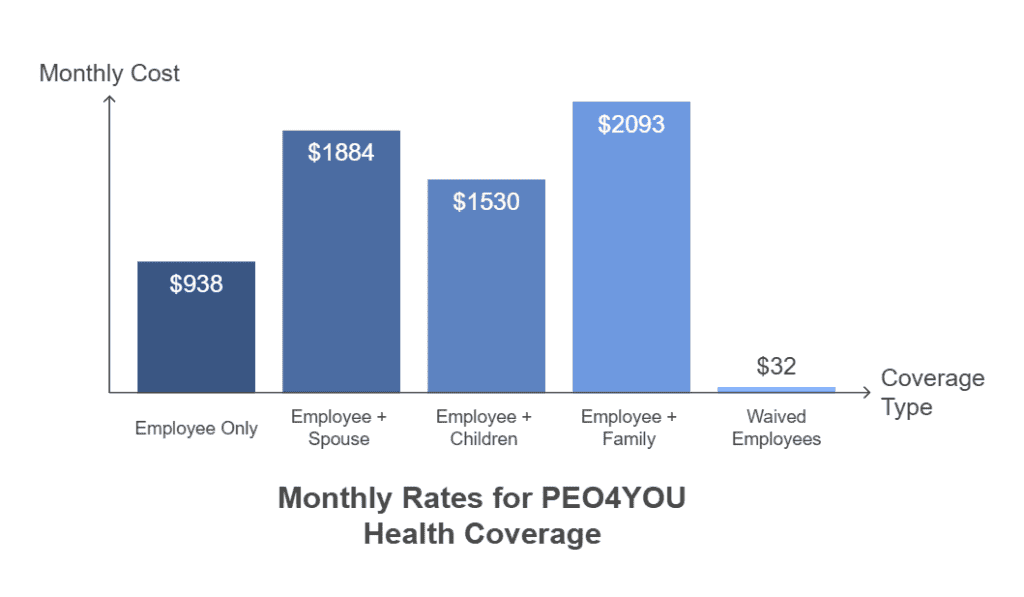

PEO4YOU stands out by providing stable premiums that do not depend on the age and health of employees. This sets it apart from regular PEO services where renewal costs often rise based on claims usage data. The typical renewal rate increase for PEO4YOU over five years is below 16%, contrasting with the national average of 40%. PEO4YOU also manages COBRA coverage to ensure former employees can still access healthcare—a valuable service for numerous small businesses.

Here are the rates for PEO4YOU:

- Employee Only: $938 per month

- Employee + Spouse: $1,884 per month

- Employee + Children: $1,530 per month

- Employee + Family: $2,093 per month

- Waived Employees: $32 per month

These rates provide comprehensive coverage, including medical, dental, vision, and life insuranceReal-World Examples Showcasing the Benefits of PEO Health Insurance

Case Study: How a Small Business Owner Benefits from PEO Health Insurance

Sarah, a small business owner with 15 employees, faced challenges in providing affordable health insurance for her team members. Collaborating with a PEO enabled her to secure a PEO health insurance plan that offered improved coverage at a budget rate compared to what she could source independently. By joining forces with the PEO scheme, she ensured that her employees had access to the healthcare options offered by the Blue Cross Blue Shield PPO network. This stability in premiums and cost-effectiveness freed up resources for Sarah to reinvest in other aspects of her business operations.

Case Study: Small Company Opts for PEO4YOU to Reduce Expenses

David manages a company that employs 25 individuals, with many of them supporting families. The average age of his team is on the higher side when compared to other businesses in the same industry category. Upon exploring Professional Employer Organization (PEO) alternatives, he found that the options quoted had higher rates due to the team members’ average age being higher. Fortunately, David discovered a cost-effective solution through PEO4YOU, which didn’t necessitate altering their current payroll or workers’ compensation arrangements. PEO4YOU was the perfect fit for David’s business due to its fixed rates and access to the Blue Cross Blue Shield PPO network, enabling him to offer top-tier healthcare benefits within his budget constraints.

Insights from Professionals on Health Insurance Provided by a PEO

Insights from Industry Experts

Sam Newland shared that health insurance offered by a PEO (Professional Employer Organization) can make a significant difference for small businesses and independent contractors by leveraging risk pooling among various companies to provide competitive rates and coverage choices that may not be accessible otherwise to many small businesses.

According to a study by NAPEO, companies utilizing PEO services experience a decrease in employee turnover rates by up to 40%. This improvement can be attributed to the health benefits provided by PEO partnerships and emphasizes the significance of PEO health insurance in retaining employees and driving business prosperity.

How to Choose the Best PEO for Health Insurance

Assessing the Requirements of Your Business

When selecting a PEO for health insurance, coverage for your business needs must be evaluated first and foremost. Think about the size, health, demographics of your workforce, the types of benefits you aim to provide, and your financial constraints. Bear in mind that not all PEO service providers are the same, hence it is vital to discover one that aligns with your needs.

Exploring the Cost of Health Insurance Plans Offered by PEOs

When you’re reviewing health insurance rates from Professional Employer Organizations (PEOs), it’s important to consider not only the premiums but also the range of coverage they offer. Some of these organizations might advertise lower premiums; however, they could have restricted networks or higher employee out-of-pocket expenses. It’s crucial to select a reliable provider that offers comprehensive coverage that benefits both your company and its employees effectively.

Verifying the List of Service Providers

One important consideration when choosing the PEO for health insurance is the network of providers they offer. For comprehensive coverage, it’s preferable to opt for a PEO that provides a PPO network, like Blue Cross Blue Shield. This enables your employees to have a broad choice of healthcare providers nationwide, giving them the freedom to select their preferred healthcare professionals.

Conclusion

PEO health insurance provides an option for enterprises, independent contractors, and sole proprietors who aim to offer thorough health coverage without straining their budgets. By utilizing the group buying influence of a PEO service provider, small businesses can secure pricing options, broader coverage, and efficient administrative assistance. This not only aids in expense management but also enhances the appeal of your business to potential employees.

If you’re a business owner seeking budget-efficient health insurance solutions for your employees, it is crucial to consider teaming up with a Professional Employer Organization (PEO). By opting for a PEO partnership, you can access advantages such as reduced expenses, improved insurance coverage, and streamlined administrative tasks, which can play a key role in providing top-tier health insurance benefits to your workforce.