Your broker just presented three options for next year's health insurance: the same carrier at a higher rate, a different carrier at a slightly lower rate, or a higher-deductible plan to offset the increase. Sound about right?

There's a fourth option that 95% of brokers never present: a Taft-Hartley multiemployer health plan. It's not new — these plans have existed since the Taft-Hartley Act of 1947 — but most brokers either don't understand them or don't have access to them. We call this The Broker Blind Spot, and it costs small employers hundreds of thousands of dollars over time.

At Business Insurance Health and PEO4YOU, we've helped employers with 30-200+ employees access Taft-Hartley trusts that delivered 15-40% savings compared to their fully insured plans — with BCBS PPO networks, no reduction in plan quality, and multi-year rate stability that fully insured carriers simply cannot match.

A Taft-Hartley health plan — also called a multiemployer health and welfare fund — is a trust-based health benefits arrangement where multiple employers contribute to a shared fund administered by a joint board of trustees. The trust negotiates directly with carriers and providers, pooling the purchasing power of all participating employers.

Unlike fully insured plans where each employer is rated independently, Taft-Hartley trusts aggregate risk across dozens or hundreds of employers. This pooling effect smooths out the impact of individual high-cost claims and gives the trust leverage that no single small employer could achieve alone.

The key structural components:

| Component | How It Works | Employer Impact |

|---|---|---|

| Trust Fund | Pooled contributions from all employers | Shared risk = rate stability |

| Board of Trustees | Joint labor-management oversight (ERISA fiduciary) | Operates for members, not carrier profit |

| Carrier Access | Trust negotiates directly with major carriers | BCBS, UHC, Aetna PPO networks available |

| Contribution Rate | Fixed per-employee-per-month contribution | Predictable budgeting, multi-year stability |

| MSO Structure | Management-side organization facilitates non-union access | No union required for participation |

The critical misconception: you don't need to be a union shop. Through a management-side organization (MSO) structure, non-union employers can participate in Taft-Hartley trusts while maintaining their existing employment relationships.

In 13+ years in the employee benefits industry, I've watched the same pattern repeat: a broker presents fully insured options, maybe adds a level-funded alternative, and calls it a day. Taft-Hartley never enters the conversation.

This isn't malice — it's structural. Most brokers don't present Taft-Hartley for three reasons:

1. Access barriers. Taft-Hartley trusts don't work through standard broker distribution channels. They require specialized relationships with trust administrators and MSO partners. If your broker doesn't already have these relationships, the option simply doesn't exist in their toolkit.

2. Commission structure. Many Taft-Hartley trusts use flat administrative fees rather than percentage-based broker commissions. This changes the economics for the advisor — not necessarily for the better. A broker earning 4-5% on a fully insured plan has limited financial incentive to move you to a flat-fee trust arrangement.

3. Complexity perception. The words "Taft-Hartley" and "multiemployer" trigger associations with large union plans, pension obligations, and regulatory complexity. The reality is simpler: for a participating employer, the experience is comparable to a fully insured plan — you pay a fixed monthly contribution and your employees access a carrier network.

This blind spot means thousands of eligible small businesses are overpaying for health coverage by 15-40% annually. When we run the numbers using the BIH Health Funding Cost Projector, the gap is often the largest single savings opportunity available.

Let's model this with a real (anonymized) scenario from our client work.

| Parameter | Value & Source |

|---|---|

| Industry | Healthcare services (generalized) |

| Headcount | 30-40 employees |

| Structure | MSO with multiple related entities |

| Current funding | Fully insured BCBS PPO |

| Current annual cost | $380,000-$420,000 (BIH client analysis) |

| Annual renewal trend | 8-12% (Segal/PwC 2026 projections) |

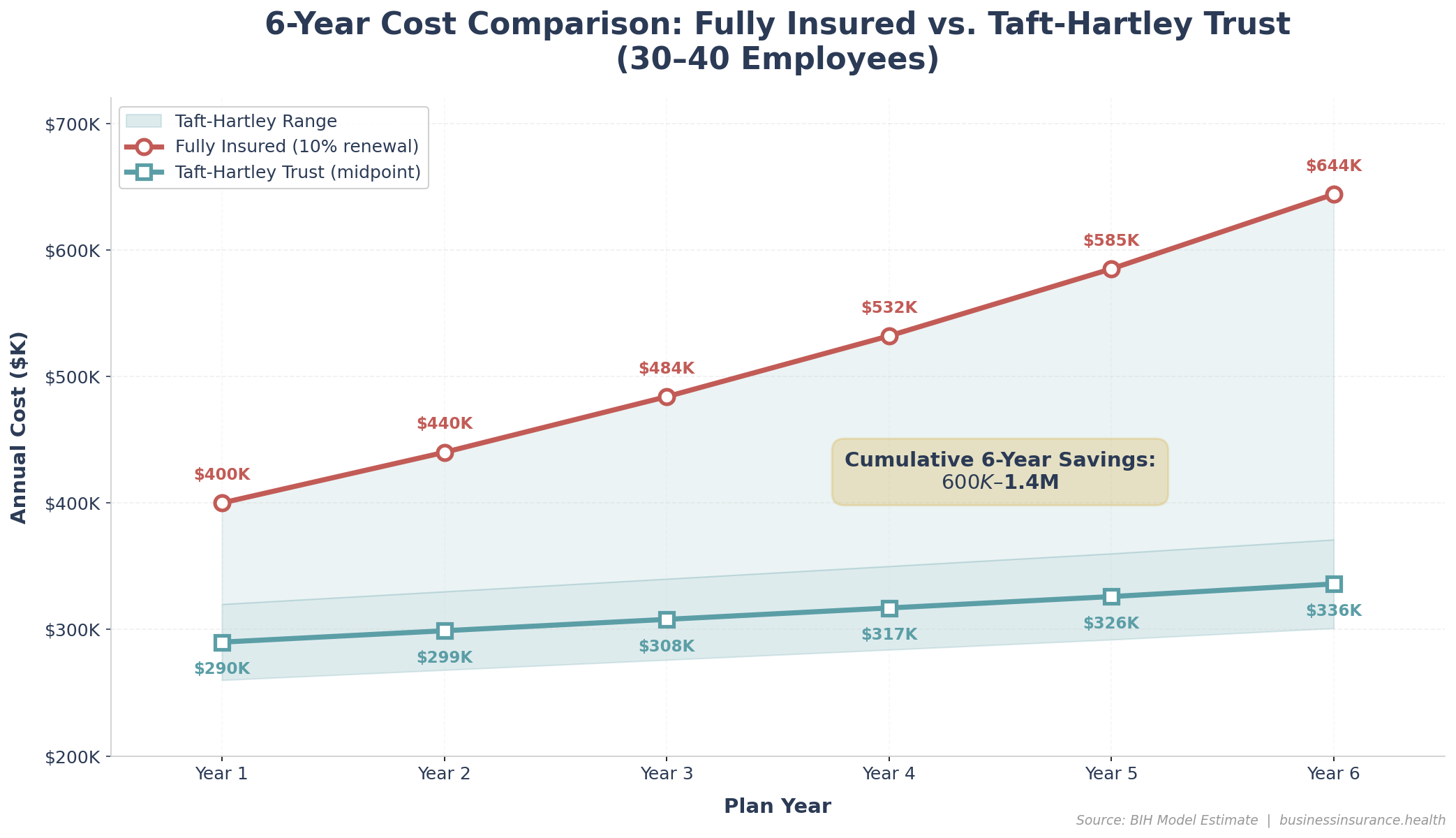

| Year | Fully Insured (10% renewal) | Taft-Hartley Trust | Annual Savings |

|---|---|---|---|

| 1 | $400,000 | $260,000-$320,000 | $80,000-$140,000 |

| 2 | $440,000 | $268,000-$330,000 | $110,000-$172,000 |

| 3 | $484,000 | $276,000-$340,000 | $144,000-$208,000 |

| 4 | $532,000 | $284,000-$350,000 | $182,000-$248,000 |

| 5 | $585,000 | $292,000-$360,000 | $225,000-$293,000 |

| 6 | $644,000 | $301,000-$371,000 | $273,000-$343,000 |

Projected 6-year cumulative savings: $600,000-$1,400,000 (BIH model estimate). The range depends on trust contribution rates, fully insured renewal trajectory, and claims experience. Conservative estimate assumes 3% annual trust contribution increases; aggressive assumes flat trust rates for years 1-3.

BIH model estimate based on anonymized client scenario. Trust contribution rates derived from actual MSO participation data. Fully insured projections based on 10% compound annual renewal, consistent with 2024-2026 small group median trends.

Eligibility varies by trust, but the general parameters at BIH and PEO4YOU include:

Minimum group size: Most trusts require 25-30+ eligible employees, though some MSO structures allow smaller groups by combining related entities (e.g., a management company with 15 employees and a services company with 20).

Industry alignment: Some trusts are industry-specific (construction, healthcare, hospitality), while others are open to multiple industries. The trust's risk profile works best when participating employers share similar workforce demographics.

Geographic availability: Taft-Hartley trusts operate regionally. Coverage depends on the carrier networks the trust has negotiated. In the Northeast (NY, MA, CT), several trusts offer BCBS and UHC PPO access.

Commitment period: Most trusts require a 12-month minimum participation, with some offering multi-year rate locks that further enhance cost predictability.

For employers comparing Taft-Hartley to other alternatives, the BIH Benefits Savings Strategy Builder models 32+ strategies including level-funded, PEO, and captive arrangements to identify the optimal fit.

ERISA fiduciary requirements. As a multiemployer plan, Taft-Hartley trusts are subject to ERISA fiduciary standards. Trustees must act in the best interests of plan participants. This is actually a benefit for participating employers — it means the plan can't make decisions that favor the carrier over members — but it adds regulatory complexity.

Limited portability. If you leave the trust, your employees transition to whatever coverage you arrange next. There's no continuity guarantee. Plan the exit strategy before you enter.

Contribution rate increases. Trust contribution rates can increase, though typically at 2-5% annually — significantly below the 8-12% fully insured median. However, in years with adverse trust-wide claims experience, increases can be higher.

Withdrawal liability. Some trusts assess withdrawal liability if an employer exits before a specified period. Understand the terms before committing. This is where having an advisor experienced with multiemployer plan structures matters.

No. Through a management-side organization (MSO) structure, non-union employers can participate in Taft-Hartley trusts. The MSO acts as the collective bargaining agent, and your employment relationships remain unchanged. This is one of the most common misconceptions that keeps eligible employers from exploring this option.

Based on BIH client analysis, employers with 30-200+ employees typically see 15-40% savings compared to fully insured rates, depending on the trust's negotiated carrier rates and the employer's current cost baseline. Use the BIH Benefits ROI Calculator to model your specific scenario.

Major carrier networks including BCBS, UnitedHealthcare, Aetna, and Cigna are commonly available through established trusts. The specific network depends on the trust's geographic footprint and negotiated contracts. Plan quality — including PPO access, prescription coverage, and preventive care — is typically comparable to or better than small group fully insured products.

PEOs bundle health insurance with HR administration, payroll, and workers' comp into a single co-employment model. Taft-Hartley plans are health-benefits-only — you keep your existing payroll, HR, and comp arrangements. For employers who only need benefits savings (not full HR outsourcing), Taft-Hartley often delivers deeper savings. For those wanting bundled services, see our PEO cost analysis.

Exit terms vary by trust. Some allow departure at the end of any plan year with 60-90 days notice. Others may assess a withdrawal contribution for employers leaving within the first 2-3 years. Always negotiate exit terms upfront and document them in writing before joining.

This analysis is provided for educational purposes and does not constitute financial or legal advice. Consult your compliance counsel and benefits advisor for guidance specific to your situation.

About the Author: Sam Newland, CFP®, has spent 13+ years in the employee benefits industry and founded Business Insurance Health and PEO4YOU to bring transparency to an industry that profits from complexity. His approach is simple: show employers the real numbers and let them decide.

Recent Posts

March 13, 2026

March 13, 2026

March 10, 2026

March 5, 2026

March 4, 2026

March 3, 2026

Get In Touch— We’re available 24/7

"*" indicates required fields

“We respect your privacy. Your contact information will be used solely for the purpose of responding to your inquiry and will not be shared with third parties.”

Click To Open Modal

Get In Touch— We’re available 24/7

"*" indicates required fields

“We respect your privacy. Your contact information will be used solely for the purpose of responding to your inquiry and will not be shared with third parties.”

Thanks!

We will be in touch soon.

If you're looking to book a consultation now

Affordable health and benefits plans for small businesses, freelancers, and independent contractors.

Copyright © 2026. Peo4you. All rights reserved.