You've heard the pitch: bundle your HR, payroll, health insurance, and workers' comp with a PEO and save money. The question nobody answers clearly is how much does a PEO actually cost, and does the math work for your company?

PEO fees typically range from $40–$160 per employee per month (PEPM) or 2–6% of gross payroll, depending on the provider, services included, and your company's risk profile. But quoting the fee in isolation is like quoting a health insurance premium without mentioning the deductible — it's the total cost of ownership that matters.

At Business Insurance Health and PEO4YOU, we've analyzed PEO cost structures for hundreds of employers. The honest answer: PEOs save some companies 15–40% on total benefits-related costs, and cost other companies 10–20% more than they need to spend. The difference comes down to what we call The PEO Break-Even Equation.

PEO pricing falls into two models:

| Model | How It Works | Typical Range |

|---|---|---|

| Flat PEPM | Fixed dollar amount per employee per month | $40–$160/employee/month |

| % of Payroll | Percentage of total gross payroll | 2–6% of gross payroll |

But the fee label is misleading. What's included in the fee varies enormously across providers. Some PEOs bundle health insurance, workers' comp, payroll, HR support, and compliance into a single PEPM. Others quote a base admin fee and layer health insurance, workers' comp, and compliance as separate line items.

Let's model this with a real (anonymized) scenario from our PEO4YOU practice.

| Parameter | Value & Source |

|---|---|

| Industry | Construction (generalized) |

| Headcount | 25–35 employees |

| Avg. annual salary | $55,000–$65,000 (BLS ECEC construction avg) |

| Workers' comp rate (standalone) | $8–$14 per $100 payroll (construction avg) |

| Current health insurance | Fully insured, $8,500–$10,000/employee/year (KFF 2024) |

| Current payroll processing | $8,000–$12,000/year standalone |

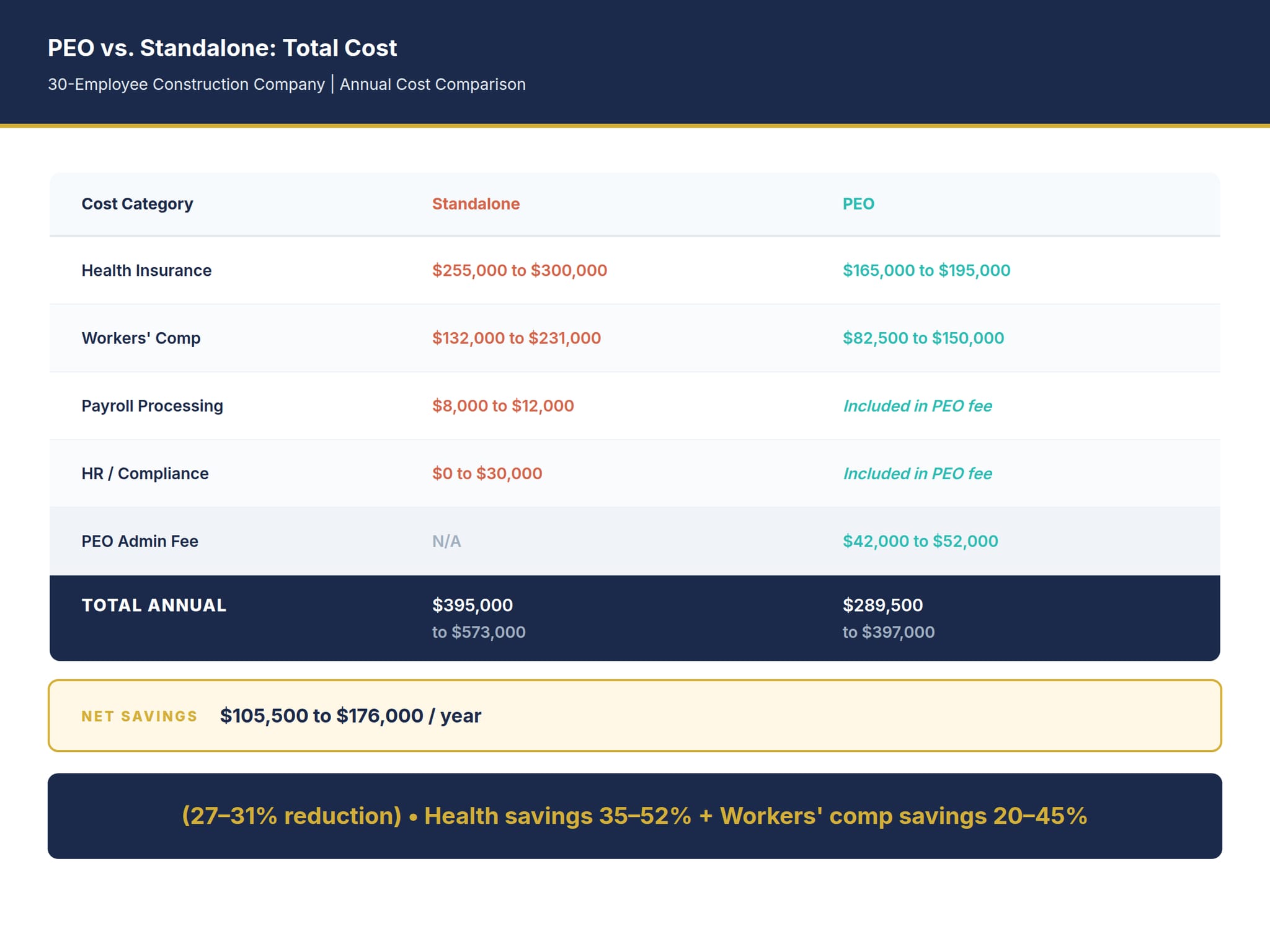

| Cost Category | Standalone | PEO |

|---|---|---|

| Health insurance | $255,000–$300,000 | $165,000–$195,000 |

| Workers' comp | $132,000–$231,000 | $82,500–$150,000 |

| Payroll processing | $8,000–$12,000 | Included in PEO fee |

| HR/compliance support | $0 (DIY) or $15,000–$30,000 (outsourced) | Included in PEO fee |

| PEO admin fee | N/A | $42,000–$52,000 ($120–$145 PEPM) |

| TOTAL ANNUAL COST | $395,000–$573,000 | $289,500–$397,000 |

Net savings range: $105,500–$176,000/year (27–31% reduction). BIH model estimate based on anonymized construction client scenario with PEO health insurance rates 35–52% below fully insured and workers' comp rates 20–45% below standalone.

BIH model estimate. Actual savings vary by PEO provider, claims history, workers' comp classification codes, and geographic location. Health savings reflect PEO master plan pooling advantage; workers' comp savings reflect PEO experience modification rate.

But notice the PEO admin fee of $42,000–$52,000. Compare that to standalone payroll at $8,000–$12,000. The PEO charges $30,000–$40,000 more in admin fees than basic payroll. The math only works because the health and workers' comp savings significantly exceed this premium.

Not every employer benefits from a PEO. Based on our analysis at BIH, the math typically breaks down when:

Your health claims are already low. If you're a healthy workforce on a level-funded plan earning surplus refunds, the PEO's pooled rate may actually cost more than your current arrangement.

Your workers' comp risk is low. Office-based employers with low workers' comp rates ($0.50–$2.00 per $100 payroll) don't get the dramatic comp savings that make PEOs compelling for construction and manufacturing.

You're above 150 employees. At this scale, you likely have enough leverage to negotiate carrier rates independently and justify dedicated HR staff. PEO admin fees become harder to justify when you can replicate the value in-house. Consider ADP TotalSource alternatives or standalone broker-managed programs.

You need maximum flexibility. PEO co-employment means shared employment records, standardized benefit plans, and carrier restrictions. If you need highly customized benefits or want to switch carriers mid-year, the PEO model creates friction.

NAPEO reports that PEO clients grow 7–9% faster and are 50% less likely to go out of business than comparable non-PEO companies, but these aggregate statistics include selection bias — companies that proactively manage their benefits tend to be better-run businesses overall.

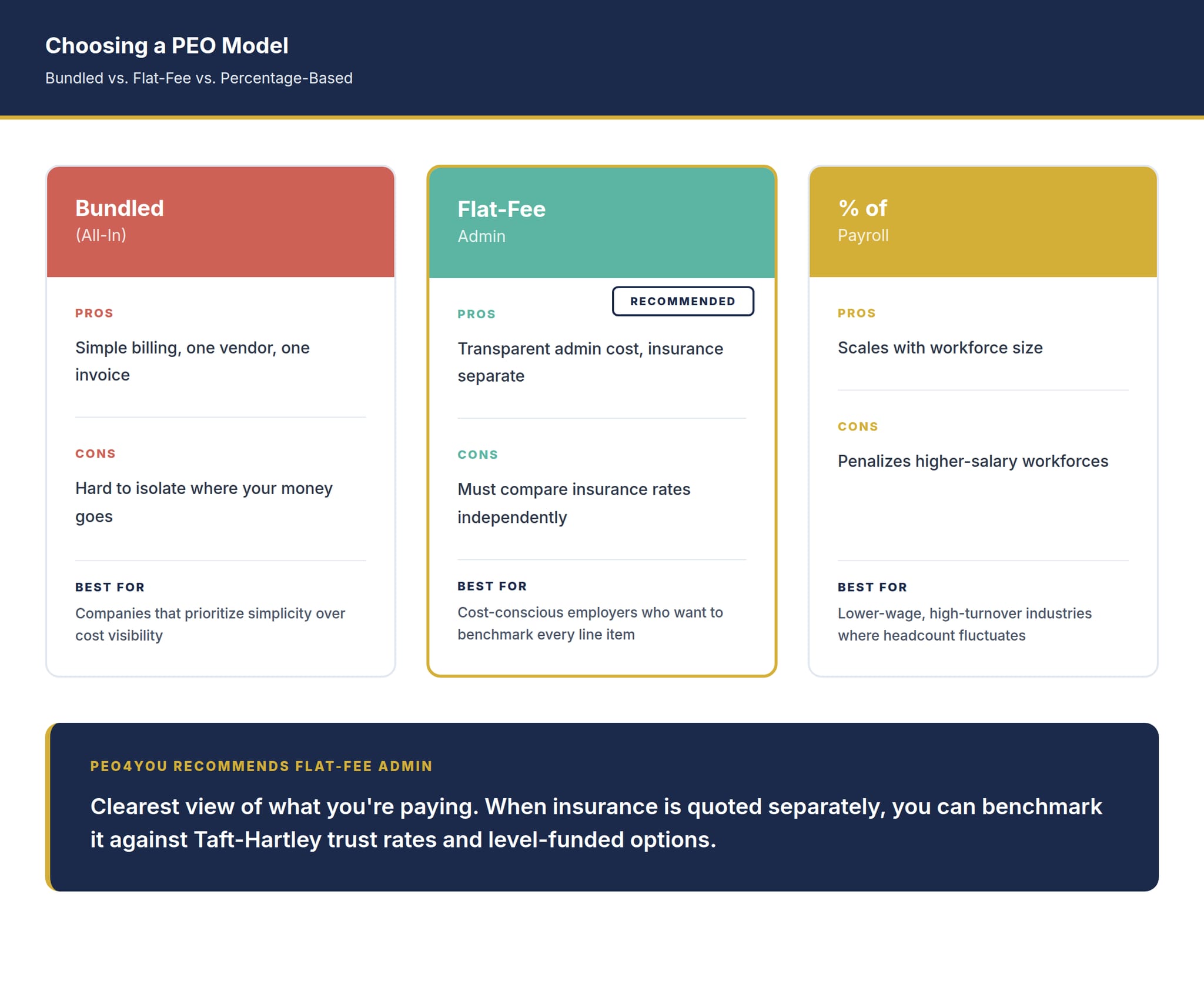

Not all PEOs are structured the same. The three primary models affect cost transparency:

| PEO Type | Pros | Cons |

|---|---|---|

| Bundled (all-in) | Simple billing, one vendor | Hard to isolate where money goes |

| Flat-fee admin | Transparent admin cost, insurance separate | Must compare insurance rates independently |

| % of payroll | Scales with workforce size | Penalizes higher-salary workforces |

At PEO4YOU, we generally recommend flat-fee admin PEOs for cost-conscious employers because they provide the clearest view of what you're paying for. When health insurance is quoted separately, you can benchmark it against Taft-Hartley trust rates and level-funded options.

PEO fees typically range from $40–$160 per employee per month for admin services, or 2–6% of gross payroll. Health insurance and workers' comp are usually additional. Total cost depends on services included, industry risk classification, and company size. Use the BIH Benefits ROI Calculator to model your total cost of ownership.

For many small businesses with 15–100 employees, PEO health insurance rates are 15–40% below small group fully insured rates because PEOs pool thousands of employees into a master plan. However, if your company has below-average claims and qualifies for level-funded or Taft-Hartley plans, those strategies may deliver comparable or greater savings without the PEO admin fee.

A standalone payroll company (ADP Run, Gusto, Paychex Flex) costs $8,000–$15,000/year for a 30-employee company. A PEO admin fee for the same company runs $42,000–$52,000/year. The $30,000–$40,000 difference pays for HR compliance support, benefits administration, risk management, and co-employment protections. Whether that's worth it depends on your internal HR capacity.

Construction, manufacturing, staffing, and other high-risk industries see the strongest PEO ROI because workers' comp rate reductions of 20–50% often represent the largest single line-item savings. Low-risk office environments benefit less on the comp side but may still gain from PEO health insurance pooling.

Consider transitioning off a PEO when your company exceeds 100–150 employees and can negotiate carrier rates independently, when your claims experience qualifies for level-funded or self-funded plans, or when the PEO's benefit plan options no longer match your workforce needs. For a detailed framework, see our PEO4YOU guide on evaluating your PEO.

This analysis is provided for educational purposes and does not constitute financial or legal advice. Consult your compliance counsel and benefits advisor for guidance specific to your situation.

About the Author: Sam Newland, CFP®, has spent 13+ years in the employee benefits industry and founded Business Insurance Health and PEO4YOU to bring transparency to an industry that profits from complexity. His approach is simple: show employers the real numbers and let them decide.

Recent Posts

March 14, 2026

March 14, 2026

March 13, 2026

March 13, 2026

March 10, 2026

March 5, 2026

Get In Touch— We’re available 24/7

"*" indicates required fields

“We respect your privacy. Your contact information will be used solely for the purpose of responding to your inquiry and will not be shared with third parties.”

Click To Open Modal

Get In Touch— We’re available 24/7

"*" indicates required fields

“We respect your privacy. Your contact information will be used solely for the purpose of responding to your inquiry and will not be shared with third parties.”

Thanks!

We will be in touch soon.

If you're looking to book a consultation now

Affordable health and benefits plans for small businesses, freelancers, and independent contractors.

Copyright © 2026. Peo4you. All rights reserved.