Your renewal letter just arrived. It says 18%. Maybe 22%. You're running a 25-50 employee company, your claims were clean last year, and the carrier is still raising your rates by double digits. Sound familiar?

You're not alone. The median small group health insurance renewal increase for 2026 is projected at 8-12%, with many employers in the 15-25% range depending on geography and claims history. Fully insured premiums have increased by an average of 6-7% annually over the past five years, compounding into a cost trajectory that quietly crushes small business margins.

But here's what most brokers won't tell you: level-funded health insurance gives small businesses access to the same cost-containment mechanics that large employers have used for decades — claims transparency, surplus refunds, and experience-based pricing — without the downside risk of full self-funding.

In our experience analyzing hundreds of renewals at Business Insurance Health and PEO4YOU, we've found that employers with 25-75 employees and relatively healthy workforces can save 10-30% in the first year by making this switch. Here's exactly how the math works.

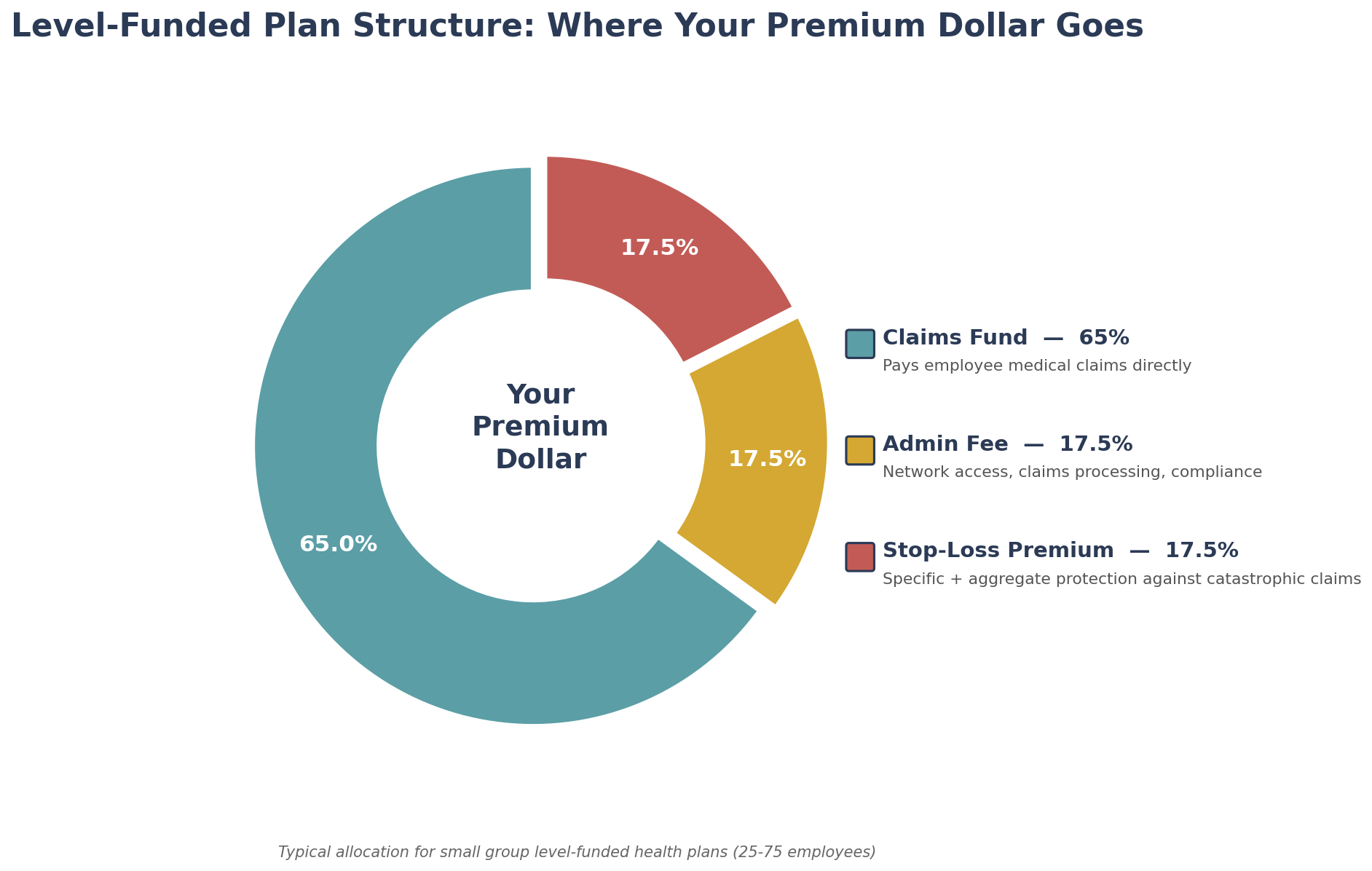

Level-funded health insurance is a funding arrangement where the employer pays a fixed monthly amount — similar to a fully insured premium — but the dollars flow into three distinct buckets: a claims fund, an administrative fee, and stop-loss insurance.

Here's how the three components break down:

| Component | What It Covers | Typical % of Total |

|---|---|---|

| Claims Fund | Pays employee medical claims directly | 60-70% |

| Admin Fee | Network access, claims processing, compliance | 15-20% |

| Stop-Loss Premium | Specific (per-person) + aggregate (total) protection | 15-25% |

The critical difference from fully insured: if your employees' claims come in under the funded amount, you get the surplus back. In a fully insured plan, the carrier keeps 100% of the difference between what you paid and what they spent on your claims.

This is why level-funded adoption has surged. According to industry data, the share of small and mid-size employers using level-funded arrangements grew from approximately 13% in 2020 to over 40% by 2023, and the trend has continued through 2025-2026. Employers are tired of subsidizing other companies' claims in fully insured risk pools.

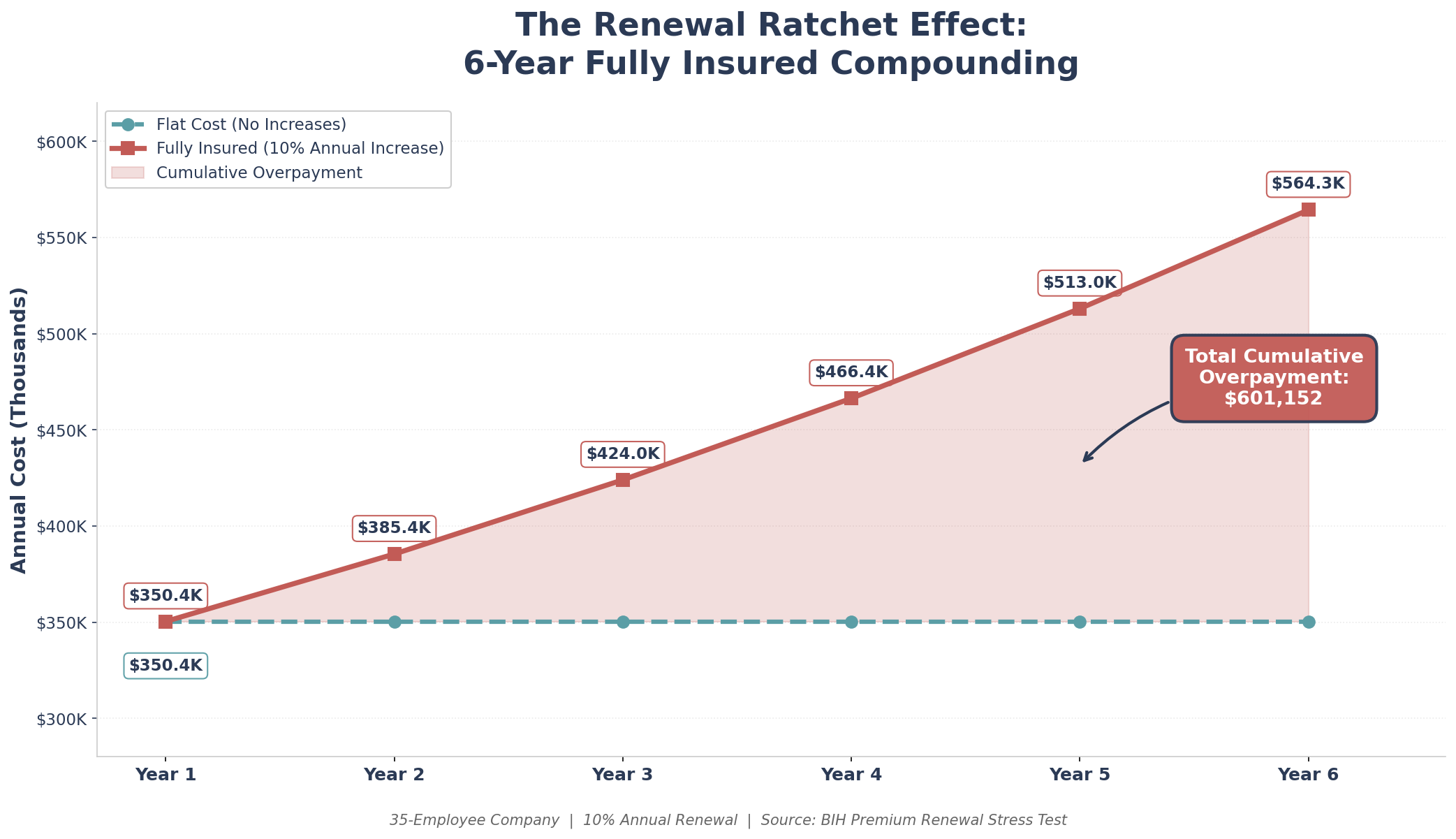

Here's a pattern we see constantly at BIH and PEO4YOU: an employer with clean claims gets hit with a renewal increase. They shop carriers. The new carrier offers a marginally better rate. Two years later, the same cycle repeats. Over six years, the compounding effect is devastating.

We call this The Renewal Ratchet Effect — and it's the hidden tax on every fully insured small employer in America.

| Parameter | Value & Source |

|---|---|

| Industry | Professional services (generalized) |

| Headcount | 25-50 employees |

| Avg. annual health cost/employee | $7,400-$8,400 (single); $22,000-$27,000 (family) — KFF 2024 |

| Funding strategy (current) | Fully insured |

| Annual renewal trend | 8-12% median (Segal/PwC 2026 projections) |

| Claims experience | Below average (clean year) |

When we modeled this scenario using the BIH Premium Renewal Stress Test, the 6-year cost trajectory was stark:

| Year | Monthly Premium (35 EE) | Annual Cost | Cumulative Overpayment vs. Flat |

|---|---|---|---|

| 1 | $29,200 | $350,400 | — |

| 2 | $32,120 | $385,440 | $35,040 |

| 3 | $35,332 | $423,984 | $108,624 |

| 4 | $38,865 | $466,380 | $224,604 |

| 5 | $42,752 | $513,024 | $387,228 |

| 6 | $47,027 | $564,324 | $601,152 |

That's over $600,000 in cumulative excess cost over six years for a 35-person company — money that went to the carrier, not to the business. BIH model estimate based on 10% compound renewal, consistent with 2024-2026 small group median trends.

A level-funded employer with the same clean claims history would have seen 3-5 of those 6 years end with a surplus refund, effectively resetting the ratchet. That's the fundamental asymmetry: fully insured plans only ratchet up, while level-funded plans can ratchet back.

Level-funded isn't a fit for every employer. In our analysis across hundreds of transitions at BIH, the strongest candidates share these characteristics:

Sweet spot: 25-75 employees with a workforce that skews younger or has below-average claims utilization. Employers above 75 often have enough scale to explore full self-funding or captive arrangements. Employers below 20 may not have enough lives to generate meaningful claims data for experience rating.

Industry fit: Professional services, technology, financial services, and any industry with a predominantly desk-based workforce tend to see the strongest level-funded results. But we've also seen construction and manufacturing employers succeed by combining level-funded plans with wellness programs and reference-based pricing networks.

Claims history: Employers with one or more years of clean claims data — no high-cost claimants above the specific stop-loss threshold — are positioned for immediate savings. If you're coming off a bad claims year, a level-funded plan may still work, but the stop-loss premium will be higher, reducing the savings margin.

When we compared funding strategies using the BIH Health Funding Cost Projector, level-funded consistently outperformed fully insured by 10-20% for employers in this sweet spot, with upside potential of 25-30% in surplus-refund years.

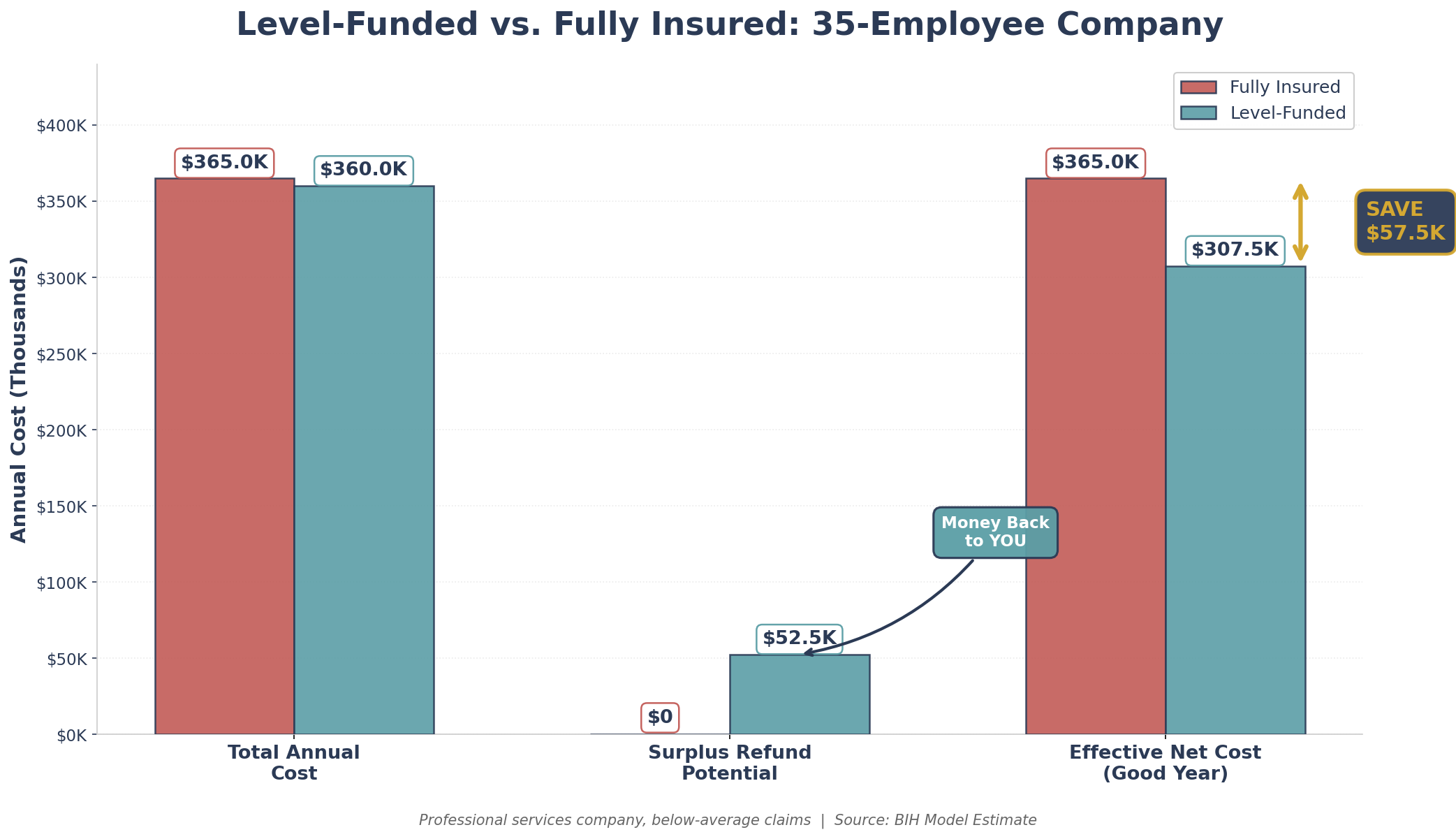

Let's break down the actual cost components side by side. This is the transparency that most brokers skip — they quote you a fully insured rate and a level-funded rate without showing where the dollars go.

| Cost Component | Fully Insured | Level-Funded |

|---|---|---|

| Claims cost (estimated) | Hidden in premium | $245,000-$265,000 |

| Admin/network fee | Hidden in premium | $52,500-$70,000 |

| Stop-loss premium | N/A (carrier retains risk) | $52,500-$87,500 |

| Carrier profit/risk margin | 12-18% of premium | Included in admin fee |

| Total annual cost | $350,000-$380,000 | $350,000-$370,000 (max) |

| Surplus refund potential | $0 (carrier keeps surplus) | $35,000-$70,000 (if claims low) |

| Effective net cost (good year) | $350,000-$380,000 | $280,000-$335,000 |

BIH model estimate based on anonymized client scenario: 35-employee professional services company, below-average claims, transitioning from fully insured to level-funded with Aetna PPO network access. Actual results vary by demographics, claims history, and stop-loss terms.

The key insight: even in the worst-case scenario, the level-funded cost is comparable to fully insured. But in a good claims year, the employer recaptures $35,000-$70,000 that would have been carrier profit under the old plan. Over three years, that's $100,000-$210,000 in potential savings for a mid-size employer.

Level-funded isn't risk-free. Here's what we advise every employer to evaluate before making the switch:

Stop-loss thresholds matter enormously. The specific stop-loss deductible — the per-person claims threshold before the reinsurer steps in — typically ranges from $25,000 to $75,000 for small groups. A lower deductible means more protection but a higher stop-loss premium. Get this wrong and your "savings" disappear into stop-loss costs.

Disclosure requirements vary by state. Some states regulate level-funded plans as insurance products (subject to state mandates and community rating), while others classify them as self-funded ERISA plans with federal-only regulation. This affects everything from benefit mandates to rate-setting flexibility. The DOL's ERISA framework governs fiduciary responsibility for self-funded arrangements.

Renewal isn't guaranteed. Unlike fully insured plans where carriers must renew (with a rate increase), level-funded carriers can decline to renew groups with adverse claims experience. If you have a catastrophic claims year, your renewal options may narrow.

For employers weighing level-funded against other alternatives, we also recommend exploring Taft-Hartley multiemployer plans — a strategy that 95% of brokers never mention — and PEO-based health coverage for groups that want bundled administration.

Based on our experience managing these transitions at BIH, here's the process that produces the best outcomes:

1. Pull your claims data. Request a detailed claims report from your current carrier (you're entitled to this under most contracts). You need 12-24 months of claims data broken out by category: inpatient, outpatient, pharmacy, and high-cost claimants above $25,000.

2. Model the scenarios. Run your data through a funding comparison tool that shows fully insured vs. level-funded vs. other strategies side by side with confidence intervals — not just best-case projections.

3. Evaluate carrier options. Carriers like UnitedHealthcare, Aetna, Cigna, and Anthem offer competitive level-funded products for small groups. Compare network breadth, stop-loss terms, and admin fees — not just the headline rate.

4. Integrate with an HRA if applicable. Many employers pair level-funded plans with an Integrated HRA to give employees cost-sharing flexibility while maintaining the employer's cost control. The BIH Plan Quality & HRA Analyzer can model whether this combination works for your demographics.

5. Set realistic expectations. Year one savings are typically 10-15%. Surplus refunds (if earned) add another 5-15% in effective savings. The compounding benefit kicks in over years 2-4 as you build claims history and avoid the Renewal Ratchet.

Most small businesses with 25-75 employees and below-average claims save 10-30% compared to fully insured plans, inclusive of potential surplus refunds. The savings come from three sources: elimination of carrier profit margin, claims transparency, and experience-based pricing. Use the BIH Premium Renewal Stress Test to model your specific scenario.

Your maximum cost is capped by the stop-loss insurance built into the plan. You won't receive a surplus refund that year, but you also won't pay more than the maximum funded amount. The specific stop-loss covers any individual claim above the deductible threshold, and the aggregate stop-loss caps your total claims exposure for the year.

No. Level-funded is a hybrid. Like self-funded plans, you're funding claims directly and get surplus refunds. But unlike full self-funding, level-funded plans include stop-loss coverage that caps your downside risk at a predetermined maximum. This makes level-funded accessible for smaller employers who can't absorb the volatility of pure self-funding.

PEOs offer a different path to savings: they pool your employees with thousands of others to negotiate volume discounts with carriers. Level-funded plans save money through claims transparency and surplus refunds rather than pooling. For a detailed cost comparison, see our PEO cost analysis guide. Some employers use PEO administration alongside level-funded funding — the two aren't mutually exclusive.

Yes. Taft-Hartley multiemployer health plans offer another path to below-market rates by aggregating risk across multiple employers in a union trust structure. For some industries, particularly construction and manufacturing, Taft-Hartley plans can deliver even deeper savings than level-funded. BIH and PEO4YOU can model both options simultaneously using the Health Funding Cost Projector.

This analysis is provided for educational purposes and does not constitute financial or legal advice. Consult your compliance counsel and benefits advisor for guidance specific to your situation.

About the Author: Sam Newland, CFP®, has spent 13+ years in the employee benefits industry and founded Business Insurance Health and PEO4YOU to bring transparency to an industry that profits from complexity. His approach is simple: show employers the real numbers and let them decide.

Recent Posts

March 13, 2026

March 13, 2026

March 10, 2026

March 5, 2026

March 4, 2026

March 3, 2026

Get In Touch— We’re available 24/7

"*" indicates required fields

“We respect your privacy. Your contact information will be used solely for the purpose of responding to your inquiry and will not be shared with third parties.”

Click To Open Modal

Get In Touch— We’re available 24/7

"*" indicates required fields

“We respect your privacy. Your contact information will be used solely for the purpose of responding to your inquiry and will not be shared with third parties.”

Thanks!

We will be in touch soon.

If you're looking to book a consultation now

Affordable health and benefits plans for small businesses, freelancers, and independent contractors.

Copyright © 2026. Peo4you. All rights reserved.