Your best employee — the one who's been with you since the beginning, who trains new hires and keeps operations running — just generated a claim that's about to make your health insurance unaffordable. One employee with a chronic condition or catastrophic event can produce claims exceeding $500,000 in a single year, and in the small group market, that translates directly to premium increases of 40% or more.

In 2026, this scenario is hitting harder than ever. With marketplace subsidies shrinking, employees who previously self-insured through the individual market are now seeking employer coverage — often bringing high-cost claim histories with them. For employers with 20-100 employees, the challenge is stark: you can't afford to not offer insurance (you'll lose talent), and you can't afford the quotes you're getting.

In a fully insured small group plan, your premium is your claims experience. Insurance carriers set rates based on the medical history of your specific employee population. One employee on a $20,000/month biologic for rheumatoid arthritis or one catastrophic surgery adds $240,000+ in annual claims to a pool that might only generate $300,000 in total premium.

The math is unforgiving. When we analyzed the situation for a growing healthcare practice with 35-60 employees, they'd received quotes ranging from $40,000 to $50,000 per month — for just 10 enrollees. That's roughly $590,000 annually. The cause: two high-cost claimants, including one with a claim history exceeding $2 million.

No amount of plan design changes fixes this. Raising deductibles, switching networks, or adding cost-sharing only shifts dollars between the employer and employees — it doesn't change the underlying risk that carriers are pricing.

This is where most brokers stop. They present the renewal, apologize for the increase, and suggest shopping the same plan design to three carriers. What they don't present are the structural alternatives that actually solve the problem.

A Professional Employer Organization operates a master health insurance policy that covers employees from hundreds of businesses. When your 35 employees join a PEO's plan that covers 20,000+ lives, your high-cost claimant becomes a fraction of a percentage of the total risk pool rather than 10% of it.

The practical impact is dramatic:

| Factor | Small Group Direct | PEO Master Policy |

|---|---|---|

| Risk pool size | 10-60 employees | 20,000+ lives |

| Impact of $2M claimant | 30-50% rate increase | <0.5% impact on pool |

| Underwriting approach | Full medical history | Simplified underwriting |

| Rate structure | Age-banded (older = more) | Community-rated (flat rate) |

| Premium stability | Subject to annual volatility | ≤3% annual increases |

For the healthcare practice we worked with, simplified underwriting through a PEO meant presenting the $2 million claim as context rather than a disqualifying event. The underwriter evaluates whether the claim pattern is ongoing or was a one-time catastrophic event — a fundamentally different question than "what did this person cost last year?"

The PEO model also replaces age-banded rates with flat, community-rated premiums. For a workforce with older employees, this alone can reduce individual premium costs by 30-50%. You can project how different funding structures affect your costs using the Health Funding Projector to compare PEO vs. direct insurance scenarios.

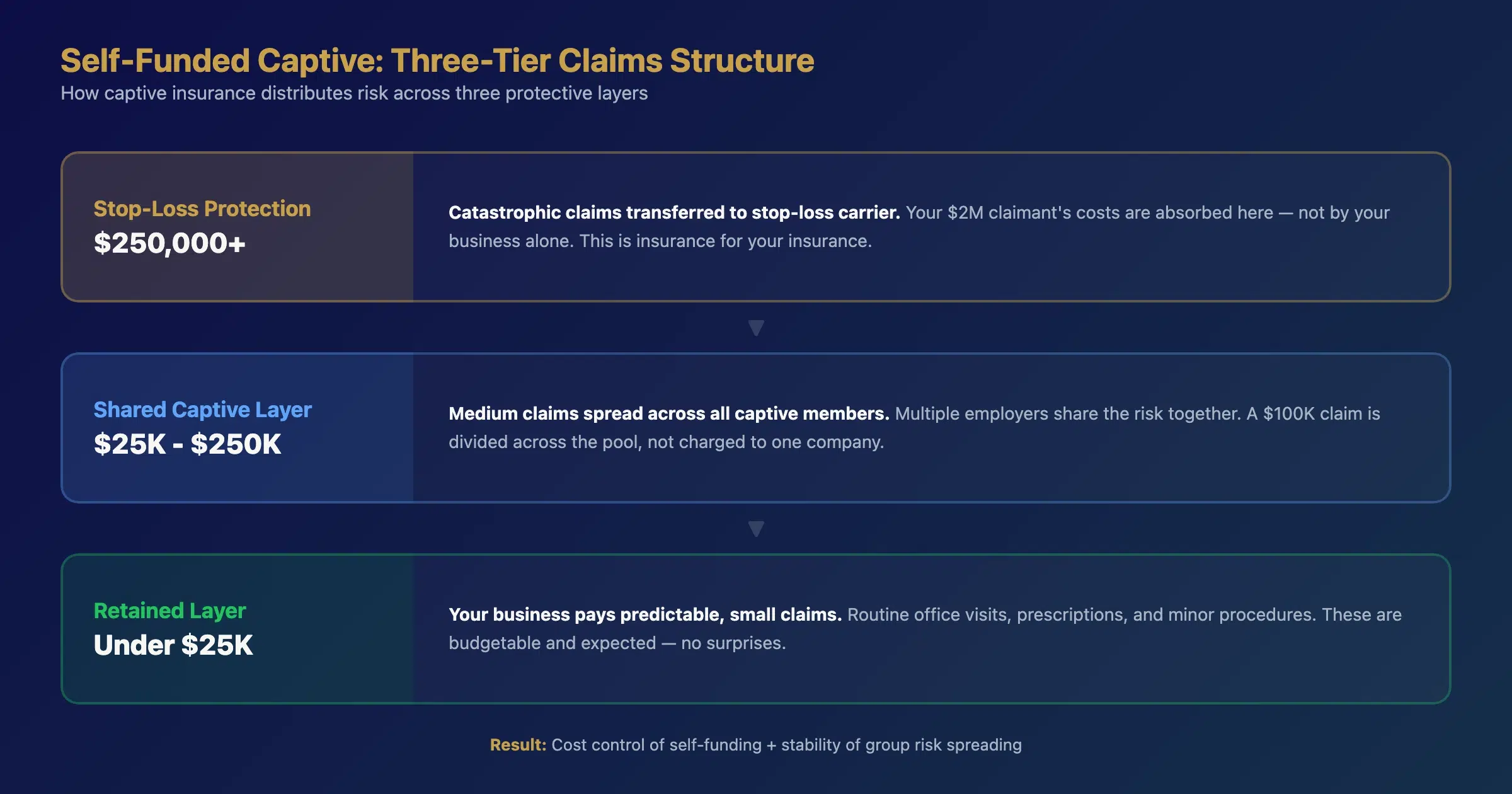

For employers with 20 or more employees enrolling in coverage, a self-funded captive offers an alternative that provides cost control, plan flexibility, and premium stability without the claim volatility that destroys small group rates.

Here's how it works: your business joins a captive — a community of employers who pool risk together. Claims are managed in three tiers:

This structure means your $2 million claimant's costs are absorbed primarily by the stop-loss layer — not by your business alone. The captive model provides direct access to major carrier networks (Blue Cross, UHC, Aetna) through a Third-Party Administrator (TPA), often with better service and more flexibility than going direct.

For employers who want plan design control — choosing deductibles, copays, and network — the captive model offers customization that PEO master policies typically don't. Learn more about how multiemployer plans offer better health insurance through similar risk-pooling structures.

In 2025-2026, the reduction of enhanced ACA marketplace subsidies created a cascade effect that directly impacts employer plans. Employees who previously self-insured through the marketplace at subsidized rates are now finding individual coverage unaffordable — and they're looking to their employer for coverage.

For the healthcare practice we analyzed, this shift was dramatic: employee interest in group coverage jumped from 10 employees to 30 when marketplace premiums became unsubsidized. That's good for participation rates — but it also means employers are absorbing employees who may have been managing expensive conditions through individual plans.

The timing creates a strategic window. Employers who can offer affordable group coverage now will retain employees who might otherwise leave for larger companies with established benefits. Understanding your integrated HRA options can help you structure coverage that's affordable for both the employer and employees with high healthcare needs.

Whether you're pursuing a PEO or captive, how you present high-cost claimant data matters. Underwriters evaluate risk, not just cost. A $2 million claim from a one-time surgical event signals different risk than $2 million in ongoing chronic condition management.

When we prepared the simplified underwriting form for the healthcare practice, we helped frame each high-cost claimant's situation with clinical context: whether the condition was resolved or ongoing, whether the treatment protocol was likely to continue at the same cost level, and what the employee's prognosis indicated about future claims.

This context transforms the underwriting conversation from "this group costs too much" to "here's why the historical claims don't predict the future."

Use the Premium Renewal Stress Test to model how your claims history affects pricing across different plan structures — it helps you walk into underwriting conversations with data rather than anxiety.

To understand how this same challenge plays out for trade businesses dealing with workers' comp and health insurance simultaneously, see our guide on PEO health insurance for construction businesses.

Yes. PEO master policies operate as large group plans, which means they cannot exclude employees based on pre-existing conditions. Simplified underwriting evaluates the overall group risk profile, not individual medical histories. This is one of the primary advantages for employers with high-cost claimants.

A self-funded captive pools multiple employers together to share risk, providing the cost control of self-funding with the stability of group risk spreading. Unlike traditional self-funding where one employer bears all claim risk, the captive structure distributes medium-sized claims across members and transfers catastrophic claims to stop-loss insurance.

Results vary based on group demographics and claim history, but we've seen small businesses reduce per-employee premium costs by 20-40% by moving from small group direct insurance to a PEO master policy. The savings come from risk pool dilution and community-rated (rather than age-banded) premium structures.

Indirectly, yes. As enhanced marketplace subsidies decrease, more employees will seek employer-sponsored coverage, increasing your enrollment. Higher enrollment can improve your negotiating position but may also bring in employees with higher healthcare utilization, which affects fully insured rates. PEO and captive models mitigate this risk through pool size.

Most captive programs require a minimum of 20 enrolled employees. Below that threshold, the risk pool is too small for effective claims spreading. For businesses with fewer than 20 enrollees, a PEO master policy typically provides better risk dilution. Read about how PEO honeymoon rates can complicate pricing decisions for smaller groups.

If you want to compare how PEO, captive, and fully insured models perform with your specific claims profile, the Health Funding Projector lets you model all three scenarios side by side.

About the Author: Sam Newland, CFP®, has spent 13+ years in the employee benefits industry and founded Business Insurance Health and PEO4YOU to bring transparency to an industry that profits from complexity. His approach is simple: show employers the real numbers and let them decide.

Recent Posts

March 4, 2026

March 3, 2026

March 2, 2026

March 1, 2026

February 25, 2026

February 21, 2026

Get In Touch— We’re available 24/7

"*" indicates required fields

“We respect your privacy. Your contact information will be used solely for the purpose of responding to your inquiry and will not be shared with third parties.”

Click To Open Modal

Get In Touch— We’re available 24/7

"*" indicates required fields

“We respect your privacy. Your contact information will be used solely for the purpose of responding to your inquiry and will not be shared with third parties.”

Thanks!

We will be in touch soon.

If you're looking to book a consultation now

Affordable health and benefits plans for small businesses, freelancers, and independent contractors.

Copyright © 2026. Peo4you. All rights reserved.