Every year, your insurance carrier collects premiums on your voluntary benefits -- dental, vision, life, disability, accident, critical illness. They pay out claims. And they keep the difference. For most voluntary benefit lines, carriers retain 40-55% of premiums as profit, overhead, and reserves.

What if you could keep that margin instead?

That's the premise behind captive insurance for employee benefits -- a structure where employers (individually or in a group) form their own insurance entity to underwrite voluntary benefit lines, retain the underwriting profit, and maintain the same employee-facing coverage. It's not new in property and casualty insurance, where over 40% of Fortune 500 companies use captives. But it's increasingly available to mid-size employers for employee benefits -- and most brokers have never heard of it.

At Business Insurance Health and PEO4YOU, we've evaluated captive structures for employers with 50-300+ employees. When the model fits, it transforms voluntary benefits from a cost center into a profit center -- literally returning underwriting margin to the employer's bottom line.

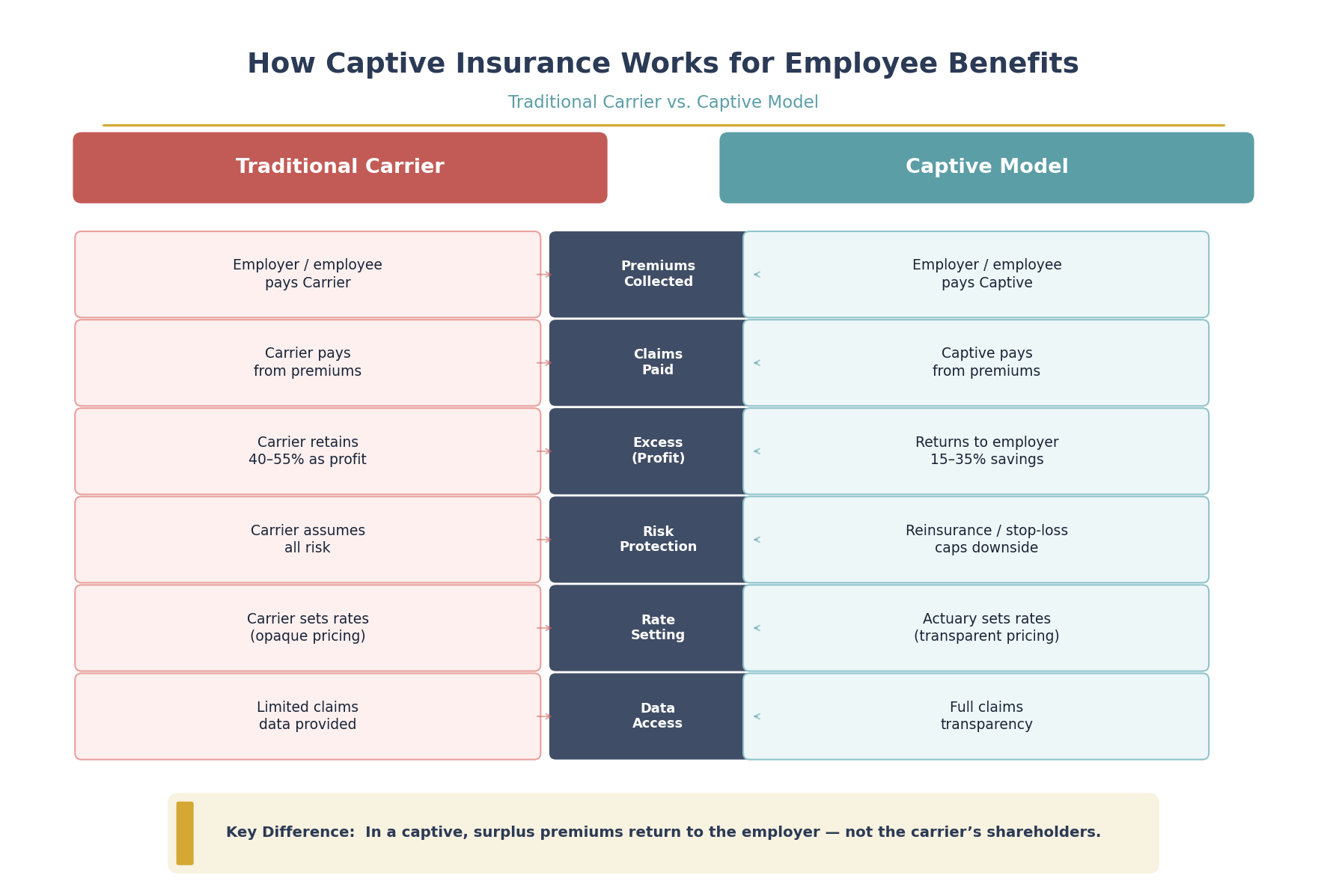

A captive insurance company is an insurance entity owned by the employer (or a group of employers) that underwrites risk the owner would otherwise transfer to a commercial carrier. In the employee benefits context, here's how the flow changes:

| Flow Step | Traditional Carrier | Captive Model |

|---|---|---|

| Premiums collected | Employer/employee to Carrier | Employer/employee to Captive |

| Claims paid | Carrier pays from premiums | Captive pays from premiums |

| Excess (profit) | Carrier retains 40-55% | Returns to employer (15-35%) |

| Risk protection | Carrier assumes all risk | Reinsurance/stop-loss caps downside |

| Rate setting | Carrier sets rates (opaque) | Actuary sets rates (transparent) |

| Data access | Limited claims data | Full claims transparency |

The mechanics are straightforward: instead of sending voluntary benefit premiums to MetLife, Guardian, or another carrier, the premiums flow into the captive entity. The captive pays claims, purchases reinsurance for catastrophic risk, and distributes the remaining surplus -- the underwriting profit -- back to the employer-owner.

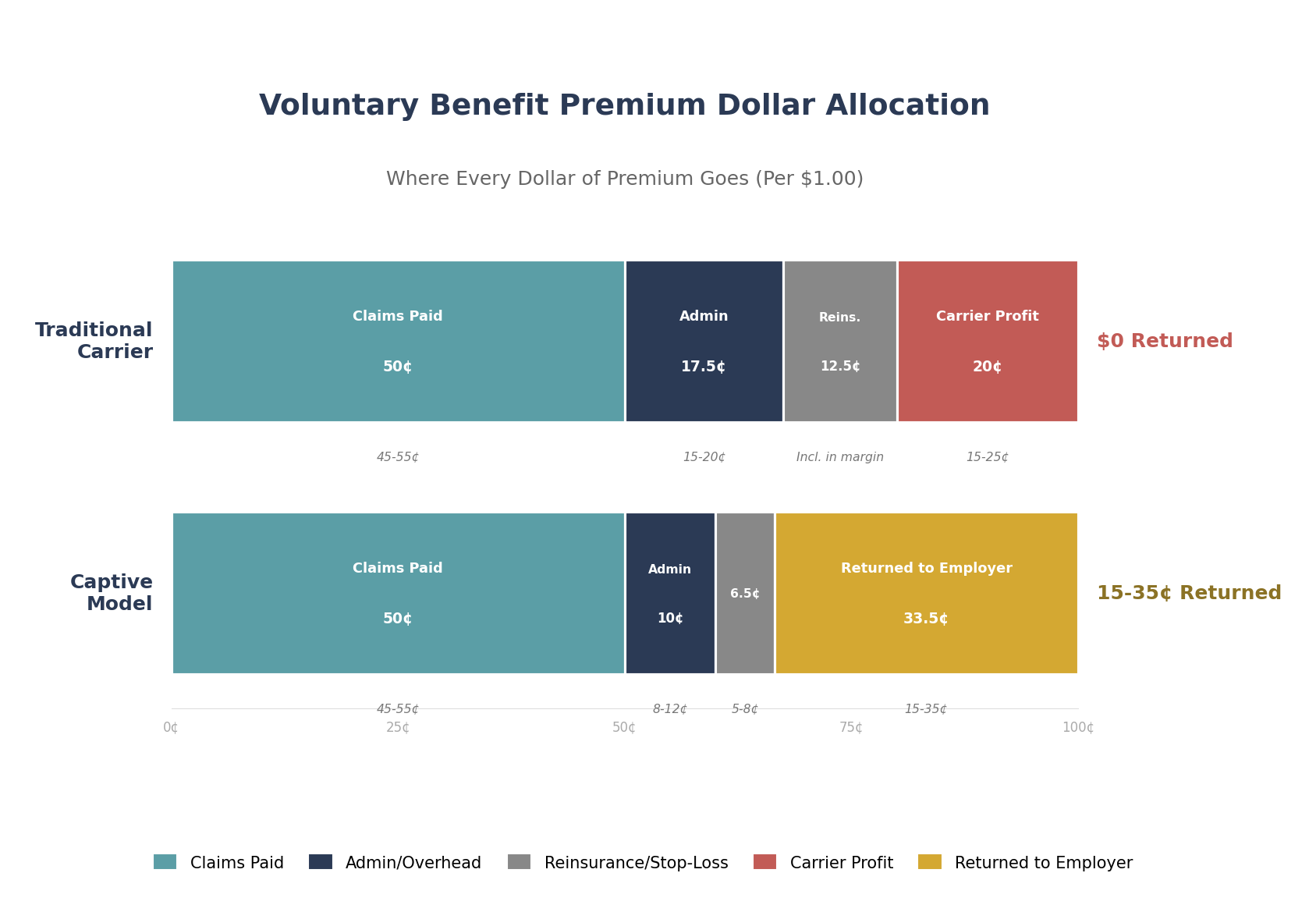

Let's trace a typical voluntary benefit dollar to show why captives create value:

| Component | Traditional Carrier | Captive Model |

|---|---|---|

| Claims paid | 45-55 cents | 45-55 cents |

| Admin/overhead | 15-20 cents | 8-12 cents |

| Reinsurance/stop-loss | Included in carrier margin | 5-8 cents |

| Carrier profit/surplus | 15-25 cents (retained by carrier) | 0 cents (no carrier profit layer) |

| Returned to employer | $0 | 15-35 cents |

The target loss ratio in a well-structured captive program is 45-55% -- meaning 45-55 cents of every premium dollar goes to claims, with the remainder covering administration, reinsurance, and employer surplus. Compare this to traditional carriers where the employer sees zero return regardless of claims experience.

BIH model based on anonymized captive program data. Target loss ratios vary by benefit line: dental typically runs 50-60%, vision 40-50%, life/disability 30-45%, accident/critical illness 25-40%.

| Parameter | Value |

|---|---|

| Employees enrolled in voluntary benefits | 80-100 (75-85% participation) |

| Annual voluntary benefit premiums | $180,000-$240,000 (dental + vision + life + disability + supplemental) |

| Traditional carrier retention | 40-55% = $72,000-$132,000 kept by carrier |

| Captive target loss ratio | 45-55% |

| Captive admin + reinsurance | 13-20% = $23,400-$48,000 |

| Estimated employer surplus (Year 1) | $27,000-$84,000 (15-35% of premiums) |

| 3-Year cumulative return (if stable claims) | $81,000-$252,000 |

The recapture: $27,000-$84,000 per year that was previously carrier profit, now returned to the employer. For a 200-employee company, double these figures. For a 50-employer group captive pooling 5,000+ lives, the aggregate economics are even more compelling.

Model your own scenario using the BIH Health Funding Cost Projector, which can compare captive structures against level-funded plans, Taft-Hartley trusts, and fully insured arrangements side by side.

Based on our evaluation work at BIH and PEO4YOU, the strongest captive candidates share these traits:

50-300+ employees with stable voluntary benefit enrollment. The captive needs sufficient premium volume to be actuarially credible. Smaller employers can access group captives where multiple companies pool premium.

High voluntary benefit participation rates (65%+ enrollment). The higher the participation, the larger the premium base, and the more predictable the claims experience. Employers with strong benefits cultures and generous employer contributions see the best results.

Willingness to accept fiduciary responsibility. As an ERISA-governed arrangement, captive programs require proper legal structure, actuarial support, and trustee oversight. This isn't a set-it-and-forget-it solution -- it's an active risk management strategy that rewards engaged employers.

Multi-year commitment. Captive programs deliver the best ROI over 3-5+ years as claims data builds and the program matures. Year-one returns may be modest; years 3-5 are where the compounding benefit of retained underwriting profit becomes significant.

For employers not ready for a full captive, level-funded health plans offer a simpler entry point to self-funded economics with surplus refund potential. Think of level-funded as the on-ramp and captive as the destination for employers seeking maximum cost control.

ERISA fiduciary obligations. The employer (or trust) that sponsors the captive has fiduciary duties to plan participants under ERISA. This means prudent management of plan assets, proper disclosure, and acting in participants' best interests. Violations can result in personal liability for fiduciaries. Work with ERISA counsel.

Claims volatility in early years. With less premium volume, small captives are more susceptible to adverse claims experience. Reinsurance mitigates catastrophic risk, but a bad claims year can eliminate the surplus. The BIH Benefits Savings Strategy Builder models both conservative and aggressive claims scenarios.

Regulatory complexity. Captive insurance companies are domiciled in specific jurisdictions (Vermont, Utah, and several offshore domiciles are popular for employee benefit captives). Each jurisdiction has its own capital requirements, reporting obligations, and regulatory framework.

Not a fit for major medical (usually). Most employer captives focus on voluntary/ancillary benefit lines where loss ratios are predictable and margins are wide. Major medical captives exist but require significantly more scale and risk tolerance. For major medical alternatives, see our guides on Taft-Hartley trusts and mid-size employer strategies.

Captive insurance is a structure where employers form their own insurance entity to underwrite voluntary benefit lines (dental, vision, life, disability, supplemental) instead of purchasing coverage from a commercial carrier. The employer retains the underwriting profit that a traditional carrier would keep -- typically 15-35% of premiums in a well-managed program.

Savings depend on company size, participation rates, and claims experience. A 100-employee company with $180,000-$240,000 in annual voluntary benefit premiums can expect employer surplus returns of $27,000-$84,000 per year once the program matures. Use the BIH Health Funding Cost Projector to model your scenario.

They share the concept of employer-retained risk, but differ in structure. Self-funded health plans (including level-funded) typically cover major medical. Captive insurance for employee benefits usually covers voluntary/ancillary lines (dental, vision, life, disability, supplemental) where loss ratios are more predictable and carrier margins are wider.

ERISA requires captive program sponsors to act as fiduciaries: managing plan assets prudently, disclosing plan information to participants, and acting solely in participants' best interests. This requires legal counsel experienced with ERISA welfare benefit plans and actuarial support for rate-setting and reserve calculations.

Yes. Group captives pool multiple employers into a single captive entity, spreading risk and achieving premium volume that individual small employers couldn't reach alone. Some programs accept employers with as few as 25-50 employees. At BIH and PEO4YOU, we can evaluate whether individual or group captive structures fit your company's profile.

This analysis is provided for educational purposes and does not constitute financial or legal advice. Consult your compliance counsel and benefits advisor for guidance specific to your situation.

About the Author: Sam Newland, CFP®, has spent 13+ years in the employee benefits industry and founded Business Insurance Health and PEO4YOU to bring transparency to an industry that profits from complexity. His approach is simple: show employers the real numbers and let them decide.

Recent Posts

March 10, 2026

March 10, 2026

March 9, 2026

March 9, 2026

March 5, 2026

March 4, 2026

Get In Touch— We’re available 24/7

"*" indicates required fields

“We respect your privacy. Your contact information will be used solely for the purpose of responding to your inquiry and will not be shared with third parties.”

Click To Open Modal

Get In Touch— We’re available 24/7

"*" indicates required fields

“We respect your privacy. Your contact information will be used solely for the purpose of responding to your inquiry and will not be shared with third parties.”

Thanks!

We will be in touch soon.

If you're looking to book a consultation now

Affordable health and benefits plans for small businesses, freelancers, and independent contractors.

Copyright © 2026. Peo4you. All rights reserved.