Health insurance can be overwhelming, especially for small businesses, independent contractors, and sole proprietors. Better health insurance solutions exist through Multiemployer Plans and Professional Employer Organizations (PEOs), offering innovative ways to access quality coverage. This article explores the structure and benefits of multiemployer plans, how they simplify healthcare, and how PEO4YOU bridges the gap as an intermediary to provide better health insurance options for businesses and individuals.

What Are Multiemployer Plans?

Multiemployer plans are health and retirement benefit programs established through collective bargaining agreements between employers and labor unions. These plans pool resources from multiple employers, offering comprehensive benefits to employees while ensuring financial sustainability.

Structure of Multiemployer Plans

Jointly Managed Multiemployer plans are administered by a board of trustees, which includes equal representation from both labor unions and employers. This collaborative approach ensures decisions benefit both parties fairly.

Pooling Resources Contributions from multiple employers go into a common fund, allowing for greater purchasing power and risk-sharing. This structure reduces costs and enables the plan to offer robust benefits compared to single-employer plans.

Flexibility for Workers Employees covered under a multiemployer plan can retain their benefits even if they switch jobs between participating employers, ensuring continuity of coverage.

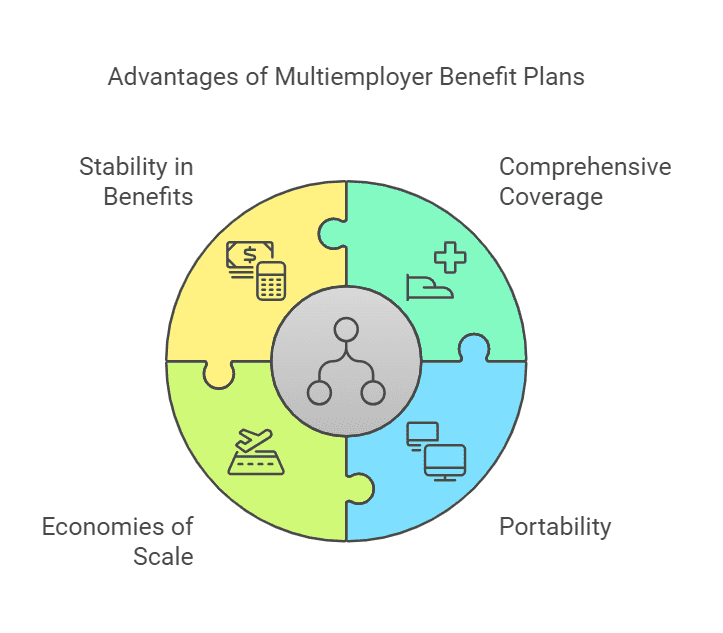

Benefits of Multiemployer Plans

Comprehensive Coverage These plans typically include a wide range of benefits:

Medical Insurance: Covering hospital stays, doctor visits, and prescriptions.

Dental and Vision: Often included to ensure holistic health coverage.

Retirement Benefits: In addition to medical plans, many multiemployer plans offer pension benefits.

Portability Workers can move between employers without losing coverage, making it particularly beneficial in industries with transient or project-based work.

Economies of Scale By pooling resources, these plans can negotiate better rates with healthcare providers and insurers, leading to lower premiums and more comprehensive benefits.

Stability in Benefits Multiemployer plans are designed to withstand economic fluctuations. The pooled funds and fiduciary oversight ensure that benefits remain stable even during downturns.

While multiemployer plans provide numerous benefits, they face several challenges that require careful management and adaptation. Below is a breakdown of the key challenges, with detailed explanations for each:

1. Funding Shortfalls

Explanation: Funding shortfalls occur when the contributions made by employers are insufficient to cover the promised benefits. This imbalance can arise from various factors, including rising healthcare costs, increasing life expectancy (leading to longer payout periods for pensions), and a decline in active participants.

Example: In industries like manufacturing, where automation has reduced the number of workers, fewer employers are contributing to the plan, while retired workers still depend on it for their pensions and healthcare benefits.

Impact: Plans with funding shortfalls may need to reduce benefits or increase employer contributions, both of which can strain relationships between employers, unions, and employees.

2. Complex Administration

Explanation: Managing contributions from multiple employers requires sophisticated systems to track payments, allocate funds, and ensure compliance with regulations such as the Employee Retirement Income Security Act (ERISA).

Challenge Areas:

Recordkeeping: Tracking contributions from numerous employers across various industries.

Compliance: Adhering to state and federal regulations to avoid penalties.

Impact: Errors in administration can result in delays in benefits, legal disputes, and loss of participant trust.

3. Regulatory Pressures

Explanation: Multiemployer plans must comply with a host of legal and regulatory requirements, including ERISA, Affordable Care Act (ACA) standards, and IRS rules. These regulations are complex and subject to change, making compliance an ongoing challenge.

Specific Challenges:

ERISA Fiduciary Standards: Mandate that plan assets be used solely for the benefit of participants, requiring meticulous financial management.

ACA Compliance: Ensures that plans meet minimum essential coverage standards and do not exceed permissible limits on cost-sharing.

Impact: Failure to comply with regulations can result in hefty fines and loss of tax-advantaged status, jeopardizing the plan’s sustainability.

4. Economic Downturns

Explanation: During recessions or industry-specific downturns, fewer employers may participate in the plan, and some may even default on their contributions. This creates a strain on the pooled resources needed to pay benefits.

Example: The COVID-19 pandemic saw a temporary halt in many industries like entertainment and construction, significantly reducing contributions to multiemployer plans while healthcare costs for participants increased.

Impact:

Reduced financial reserves to cover unexpected spikes in claims.

Increased financial risk to the plan as fewer active workers support a growing number of retirees.

5. Demographic Shifts

Explanation: As the workforce ages, the number of retirees drawing benefits increases while the number of active contributors declines. This demographic imbalance places a strain on the plan’s financial resources.

Example: In the construction industry, many older workers are retiring, and younger workers are entering the field at a slower rate, reducing contributions to the fund.

Impact: A growing retiree-to-worker ratio can lead to financial instability, requiring plans to increase employer contributions or reduce benefits.

6. Healthcare Cost Inflation

Explanation: Rising healthcare costs have a direct impact on multiemployer plans, which must cover these expenses for participants. This challenge is amplified for plans that include comprehensive coverage, such as hospitalization, mental health, and prescription drugs.

Example: The annual increase in drug prices can significantly strain the plan’s budget, especially for chronic condition management or high-cost specialty medications.

Impact: Rising costs may necessitate higher premiums for participants or reductions in covered services, potentially leading to dissatisfaction among plan members.

How PEO4YOU Complements Multiemployer Plans

To tackle these challenges, multiemployer plans are adopting various measures, including:

Modernizing Administration Systems: Using advanced technology to streamline recordkeeping and compliance tracking.

Strengthening Financial Reserves: Building robust reserves to buffer against economic downturns and unexpected costs.

Enhanced Participant Education: Informing participants about plan benefits and changes to ensure informed decision-making.

Advocating for Policy Support: Engaging with policymakers to address funding issues and ensure equitable regulations.

By addressing these challenges proactively, multiemployer plans can continue to provide stability and better health insurance coverage for participants in industries with fluctuating workforces. For businesses and individuals seeking to navigate these complex systems, PEO4YOU offers expert guidance and support to ensure optimal benefit management and compliance.

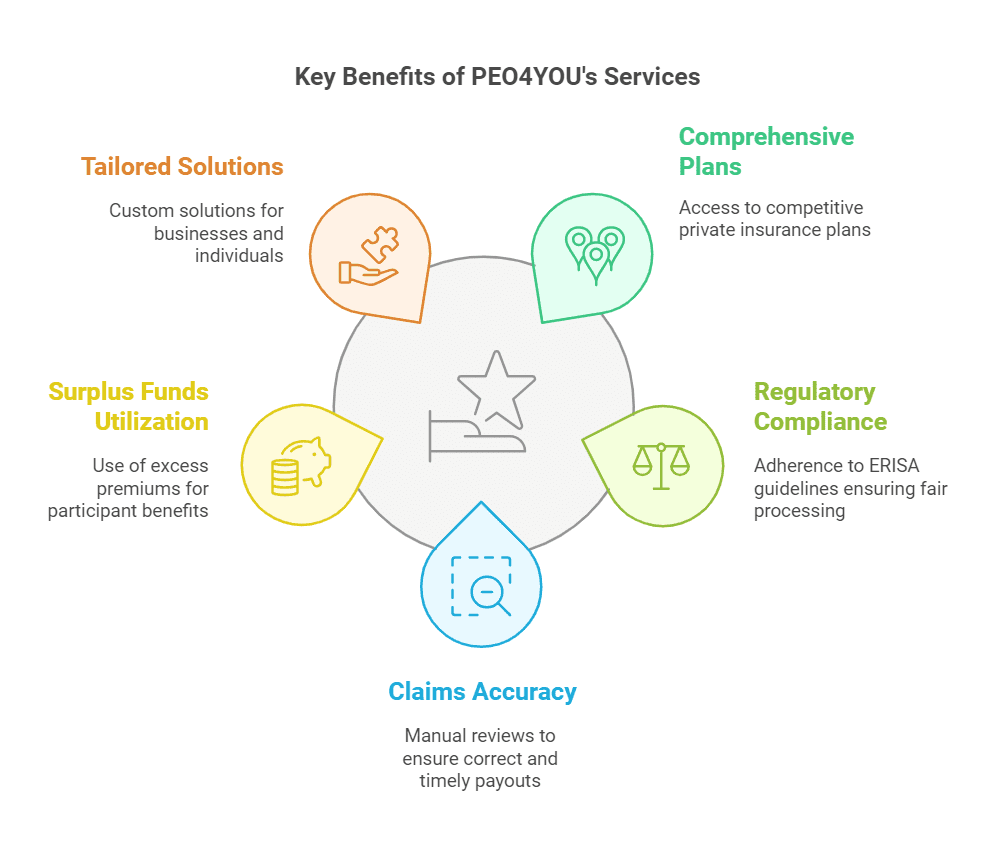

Key Benefits of PEO4YOU’s Services

Access to Comprehensive Plans PEO4YOU pools multiple small businesses, allowing them to access competitive private insurance plans that offer robust coverage at affordable rates.

Regulatory Compliance

Unlike traditional carriers, PEO4YOU is regulated by ERISA guidelines, ensuring claims are processed without profit-driven motives.

No minimum loss ratio (MLR) requirements mean premiums go directly to covering medical costs, enhancing plan value.

No Claims Game Practices: Traditional insurers often use algorithms to reduce payout amounts, leading to delayed or denied claims. PEO4YOU manually reviews medical bills to ensure accuracy, catching errors such as duplicate charges or incorrect coding, which are present in up to 80% of claims.

Excess Premiums for Participant Benefit Any surplus funds remain within the system, used for:

Enhancing benefits.

Building reserves for future uncertainties.

Participant education and communication.

Tailored Solutions Whether you’re a small business seeking group coverage or an individual navigating options, PEO4YOU customizes solutions to meet your needs.

Conclusion: Simplify Your Path to Better Health Insurance

Whether through multiemployer or PEO-facilitated plans, individuals and businesses have more options than ever to get health coverage that works. Multiemployer plans offer stability, affordability, and broad access, while PEOs provide tailored solutions for those outside the traditional scope of collective bargaining.

PEO4YOU stands as a trusted intermediary, ensuring clients find the best possible coverage for their needs. From regulatory compliance to personalized support, PEO4YOU bridges the gap, helping you navigate the complexities of the healthcare system with confidence.

Take the next step—partner with PEO4YOU to explore your options and secure comprehensive, affordable healthcare today.

March 1, 2026

PEO Honeymoon Rates: Spot Bait-and-Switch Pricing

Sam Newland

February 25, 2026

Medical Insurance Startup Strategies to Save Money and Keep Talent

Sam Newland

February 21, 2026

Best Dental Plans for Small Businesses That Keep Teams Smiling

Sam Newland

February 15, 2026

Blue Cross Blue Shield Employee Benefits for Small Businesses

Sam Newland

February 8, 2026

How Business Health Plus Helps You Offer Better Benefits

“We respect your privacy. Your contact information will be used solely for the purpose of responding to your inquiry and will not be shared with third parties.”

Click To Open Modal

Questions ?

Get In Touch We’re available 24/7

Floating Contact Form

Get In Touch—

We’re available 24/7

"*" indicates required fields

“We respect your privacy. Your contact information will be used solely for the purpose of responding to your inquiry and will not be shared with third parties.”

Question ?

Get In Touch We’re available 24/7

Floating Contact Form

Get In Touch—

We’re available 24/7

"*" indicates required fields

“We respect your privacy. Your contact information will be used solely for the purpose of responding to your inquiry and will not be shared with third parties.”

Thanks! We will be in touch soon. If you're looking to book a consultation now