Key Takeaways

You run a manufacturing operation with 20 employees. Your health plan costs $130,000 a year. The plan has 50% coinsurance and a $10,000 out of pocket maximum. You're paying 80% of the premium, and your employees are still one hospital visit away from a $5,000 bill they can't afford.

Does that sound like a good deal to anyone?

It shouldn't. Because across the manufacturing sector, companies like yours are overpaying for health coverage that underdelivers. And the worst part: most brokers keep presenting the same three options every year. The same carrier at a higher rate. A different carrier at a slightly lower rate. Or a higher deductible plan to "offset" the increase.

There are better options. And they don't require you to cut benefits.

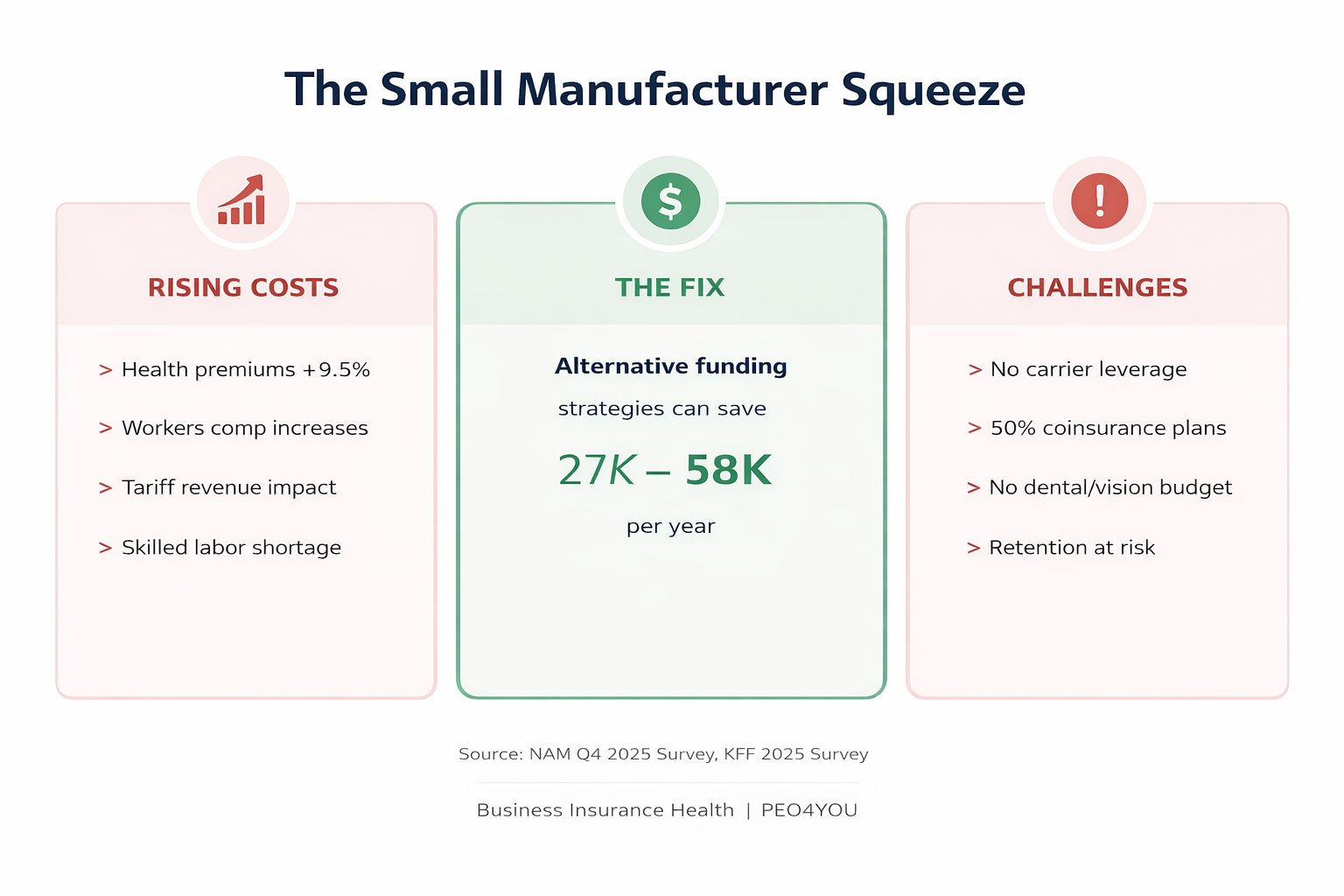

Manufacturing companies face a specific combination of factors that drive healthcare costs higher than many other industries:

Physical job demands create claims. Even in modern manufacturing facilities, workers face musculoskeletal injuries, repetitive motion issues, and occasional acute injuries. These claims show up in your experience rating and drive renewal increases.

Smaller groups get worse pricing. A manufacturer with 20 employees has virtually no negotiating leverage with carriers. According to the KFF 2025 survey, average annual premiums reached $9,325 for single coverage and $26,993 for family coverage.³ Small groups typically pay above these averages because carriers price in higher risk and lower administrative efficiency.

Workforce demographics skew older. Manufacturing workforces often include experienced tradespeople in their 40s, 50s, and 60s. In community-rated states, age doesn't directly affect premiums. But in states with age banding, older workforces pay significantly more.

Tariff uncertainty compounds the pressure. The NAM Q4 2025 survey found that rising healthcare costs have become the second-greatest business challenge for manufacturers, behind only an unfavorable business climate.¹ Companies that have already absorbed 20% to 25% revenue hits from tariff disruptions cannot absorb another 10%+ on healthcare costs.

Here's what separates good companies from great ones in manufacturing: the great ones don't treat health plan savings as profit. They reinvest it.

We call this The Benefits Reinvestment Strategy. When a company saves $25,000 to $40,000 on health coverage through smarter funding, the best use of that money is:

1. Reduce employee cost-sharing (lower deductibles, better coinsurance)

2. Add dental and vision (often requested, frequently skipped due to cost)

3. Fund wage increases that improve retention

4. Create an HRA that covers employee out of pocket costs

A manufacturer we worked with put it this way: the goal isn't to cut costs to increase company profit. It's to stop overpaying insurers so you can put that money back into the people who actually run your operation.

That philosophy is especially important in manufacturing, where skilled workers are increasingly difficult to find and expensive to replace. The cost of losing one experienced machinist, welder, or line supervisor far exceeds any annual savings on health premiums.

A PEO combines your employees with thousands of others into a single large group for benefits purchasing. This gives a 20 employee manufacturer access to the same health plans, rates, and voluntary benefits as a Fortune 500 company.

How it works for manufacturers:

Cost impact: PEO admin fees typically run $40 to $160 per employee per month, but the health plan savings, workers' comp reductions, and HR time savings often produce a net positive ROI. NAPEO research shows PEO clients grow twice as fast, have 12% lower employee turnover, and are 50% less likely to go out of business.⁴

Best for: Manufacturers with 10 to 40 employees who want comprehensive HR support alongside better benefits. Read more about PEO health coverage options.

This is the option most brokers never mention. A multiemployer trust pools thousands of employees across hundreds of small companies, creating the buying power of a large employer.

Key advantages for manufacturers:

Cost impact: For a manufacturer paying $130,000 per year for 20 employees on a 50% coinsurance plan, a multiemployer trust typically offers richer benefits (20% coinsurance, lower out of pocket maximum) at comparable or lower cost. The savings come from the trust's massive risk pool and non-profit structure.

Best for: Manufacturers with 5 to 50 employees seeking premium stability and richer benefits.

A level-funded plan gives you fixed monthly payments like fully insured, but with transparency and potential upside. If your group has a healthy year with low claims, you get money back.

Key advantages for manufacturers:

Cost impact: Level-funded plans typically save 5% to 15% compared to fully insured in the first year, with the potential for additional savings through refunds. More importantly, the claims data you receive enables smarter plan design decisions for future years.

Best for: Manufacturers with 25 to 75 employees and reasonably healthy workforces who want data visibility. Read our guide on when to transition from fully insured to self-funded.

This isn't a health plan. It's a tax savings strategy that layers on top of whatever health plan you already have. A Section 125 wellness plan reduces employer FICA taxes by $900 to $1,400 per employee per year while simultaneously increasing employee take-home pay by 2% to 5%.⁵

Key advantages for manufacturers:

Cost impact: For a 20 employee manufacturer, annual employer savings of $15,000 to $28,000 after program fees.

Best for: Any manufacturer with 20+ employees, regardless of current health plan. Stack this with any of the other three strategies.

📊 MODEL YOUR SAVINGS BY STRATEGY

Benefits Savings Strategy Builder at businessinsurance.health — explore 32+ cost reduction strategies for your specific headcount and industry.

No login required. No email gate. Free.

Like this tool? We built five more just like it — all free, all ungated. Explore all tools at Business Insurance Health.

| Parameter | Value | Source |

|---|---|---|

| Industry | Manufacturing (craft production) | Scenario |

| Employees | 20 | Scenario |

| Current plan | Fully insured, 50% coinsurance, $10K OOP max | Based on typical small group |

| Current annual cost (employer 80%) | $130,000 | Scenario |

| Average employee salary | $48,000 | BLS manufacturing median⁶ |

| Strategy | Est. Annual Cost | Savings vs. Current | Employee Benefit Improvement |

|---|---|---|---|

| Current (fully insured) | $130,000 | Baseline | 50% coinsurance, $10K OOP max |

| PEO arrangement | $100,000 to $115,000 | $15,000 to $30,000 | 20% coinsurance, lower OOP, dental/vision included |

| Multiemployer trust | $95,000 to $118,000 | $12,000 to $35,000 | First-dollar copays, 20% coinsurance, full Rx coverage |

| Level-funded | $110,000 to $125,000 | $5,000 to $20,000 | Similar benefits + claims data + potential refund |

| Section 125 overlay (add-on) | Saves $15,000 to $28,000 | Stacks with above | Telehealth, behavioral health, Rx, EAP |

BIH model estimate based on market rates for manufacturing groups of 15 to 30 employees. Actual costs depend on employee demographics, location, claims history, and plan design. All figures represent ranges.

| Metric | Conservative | Moderate |

|---|---|---|

| Health plan savings | $12,000 | $30,000 |

| Section 125 FICA savings | $15,000 | $28,000 |

| Total annual savings | $27,000 | $58,000 |

| Savings per employee | $1,350 | $2,900 |

| Employee take-home increase | $1,000/yr each | $2,400/yr each |

That $27,000 to $58,000 in annual savings? That's your reinvestment fund. Better dental coverage. A $500 HRA for each employee. A $1/hour wage increase across the board. Whatever makes the biggest difference for retention.

Pull your most recent renewal letter and benefits summary. You need: annual premium, employer contribution percentage, deductible, coinsurance, out of pocket maximum, and which carrier/plan you're on. If you don't have this, your broker should send it within 24 hours.

Use the Premium Renewal Stress Test to model your current plan against alternative funding strategies over six years. This shows you not just Year 1 savings but the cumulative impact of different rate increase trajectories.

If the numbers show opportunity, get a formal evaluation from a benefits consultant who works across all funding strategies (not just one carrier or one PEO). The evaluation should include PEO options, multiemployer trust eligibility, level-funded quotes, and Section 125 overlay analysis. At Business Insurance Health and PEO4YOU, we evaluate all six plan types for every client. There's no commitment and no cost for the initial analysis.

Yes. Most PEOs accept manufacturing companies with as few as 5 employees. Manufacturing is a strong fit for PEOs because of the bundled workers' compensation benefit, which is often 15% to 30% cheaper through a PEO's group rating than standalone policies. Some PEOs specialize in manufacturing and construction, offering features like certified payroll, prevailing wage support, and OSHA compliance assistance. Learn more about PEO health coverage.

According to the KFF 2025 survey, average annual premiums are $9,325 for single coverage and $26,993 for family coverage across all industries.³ Manufacturer-specific costs depend on workforce age, location, and plan design. For a 20 employee manufacturer with a blended single/family enrollment, annual employer costs typically range from $5,500 to $8,000 per employee (at 80% employer contribution). Projected 2026 averages may surpass $17,000 per employee including both employer and employee shares.²

Through a PEO, yes. PEOs combine payroll, health coverage, workers' compensation, and HR administration into a single platform. The workers' comp savings alone can be significant for manufacturers: PEO group rates are typically 15% to 30% lower than standalone policies because the PEO's larger pool diversifies risk across many industries and employers. This is covered in our guide to cutting costs while maintaining quality.

A multiemployer trust (often called a Taft-Hartley plan) pools employees from hundreds of small companies into a single large group. This creates the purchasing power and risk diversification of a large employer. For manufacturers, the key benefits are premium stability (increases averaging 3% or less annually), nationwide carrier networks, and richer plan designs than the small group market offers. Minimum enrollment is typically 5 employees. See our detailed guide on how multiemployer plans offer better health coverage.

The transition period does require communication and enrollment, typically 30 to 60 days. However, most alternative funding strategies (PEO, multiemployer trust, level-funded) offer the same major carrier networks (Blue Cross Blue Shield, UHC, Aetna, Cigna) that your employees may already be using. In many cases, employees keep the same doctors and hospitals with better coverage at lower personal cost. The disruption is administrative, not clinical.

📊 CALCULATE YOUR BENEFITS ROI

Benefits ROI Calculator at businessinsurance.health — see the full financial impact of benefits improvements for your manufacturing company.

No login required. No email gate. Free.

Like this tool? We built five more just like it — all free, all ungated. Explore all tools at Business Insurance Health.

1. National Association of Manufacturers. "NAM Manufacturers' Outlook Survey, Fourth Quarter 2025." December 2025. https://nam.org/wp-content/uploads/securepdfs/2025/12/NAM_Q4_2025_Outlook_Write_Up.pdf

2. Live Insurance News. "Small Business Health Insurance Hits Breaking Point as Costs Surge 11% in 2026." March 2026. https://www.liveinsurancenews.com/small-business-health-insurance/8570249/

3. Kaiser Family Foundation. "2025 Employer Health Benefits Survey." October 2025. https://www.kff.org/health-costs/2025-employer-health-benefits-survey/

4. National Association of Professional Employer Organizations. "Industry Research & Data." NAPEO.org. https://napeo.org/intro-to-peos/industry-research-data/

5. IRS. "Topic No. 751, Social Security and Medicare Withholding Rates." IRS.gov. https://www.irs.gov/taxtopics/tc751. Section 125 savings calculated at 7.65% employer FICA rate applied to DOI-approved benefit value. See our detailed analysis in the Section 125 wellness plan savings guide.

6. Bureau of Labor Statistics. "Occupational Employment and Wage Statistics: Production Occupations." May 2025. https://www.bls.gov/oes/

7. Peterson-KFF Health System Tracker. "How Much and Why Premiums Are Going Up for Small Businesses in 2026." September 2025. https://www.healthsystemtracker.org/brief/how-much-and-why-premiums-are-going-up-for-small-businesses-in-2026/

8. Business.com. "Average Employee Health Insurance Cost in 2026." January 2026. https://www.business.com/articles/health-insurance-costs-this-year/

Methodology Note: Cost comparisons in this article use a 20-employee manufacturer model with 80% employer contribution and blended enrollment (mix of single and family coverage). Current annual cost of $130,000 is based on client consultation data. Alternative strategy pricing reflects 2025-2026 market rates for manufacturing groups of 15 to 30 employees. Section 125 savings are calculated using the IRS FICA rate of 7.65% applied to a DOI-approved benefit value of $1,600 per month, with program fees of $35 to $45 per employee per month. All projections are presented as ranges.

This analysis is provided for educational purposes and does not constitute financial or legal advice. Consult your compliance counsel and benefits advisor for guidance specific to your situation.

About the Author

Sam Newland, CFP® is the Founder and President of Business Insurance Health and PEO4YOU. With over 13 years in the employee benefits industry and experience as the former #1 face-to-face health benefits advisor nationally, Sam helps businesses with 30 to 200+ employees navigate funding strategies that most brokers don't present. Contact: [email protected] | 857-255-9394 | businessinsurance.health | peo4you.com

Recent Posts

March 17, 2026

March 17, 2026

March 15, 2026

March 14, 2026

March 14, 2026

March 13, 2026

Get In Touch— We’re available 24/7

"*" indicates required fields

“We respect your privacy. Your contact information will be used solely for the purpose of responding to your inquiry and will not be shared with third parties.”

Click To Open Modal

Get In Touch— We’re available 24/7

"*" indicates required fields

“We respect your privacy. Your contact information will be used solely for the purpose of responding to your inquiry and will not be shared with third parties.”

Thanks!

We will be in touch soon.

If you're looking to book a consultation now

Affordable health and benefits plans for small businesses, freelancers, and independent contractors.

Copyright © 2026. Peo4you. All rights reserved.