The Employee Retirement Income Security Act (ERISA) requires certain employee benefit plans to submit Form 5500 as a mandatory compliance document. The document serves as a key tool for the federal government to monitor a plan’s financial status and management of investments and operations.. Understanding who must file Form 5500 for health insurance is essential for employers to remain compliant and avoid potential penalties.

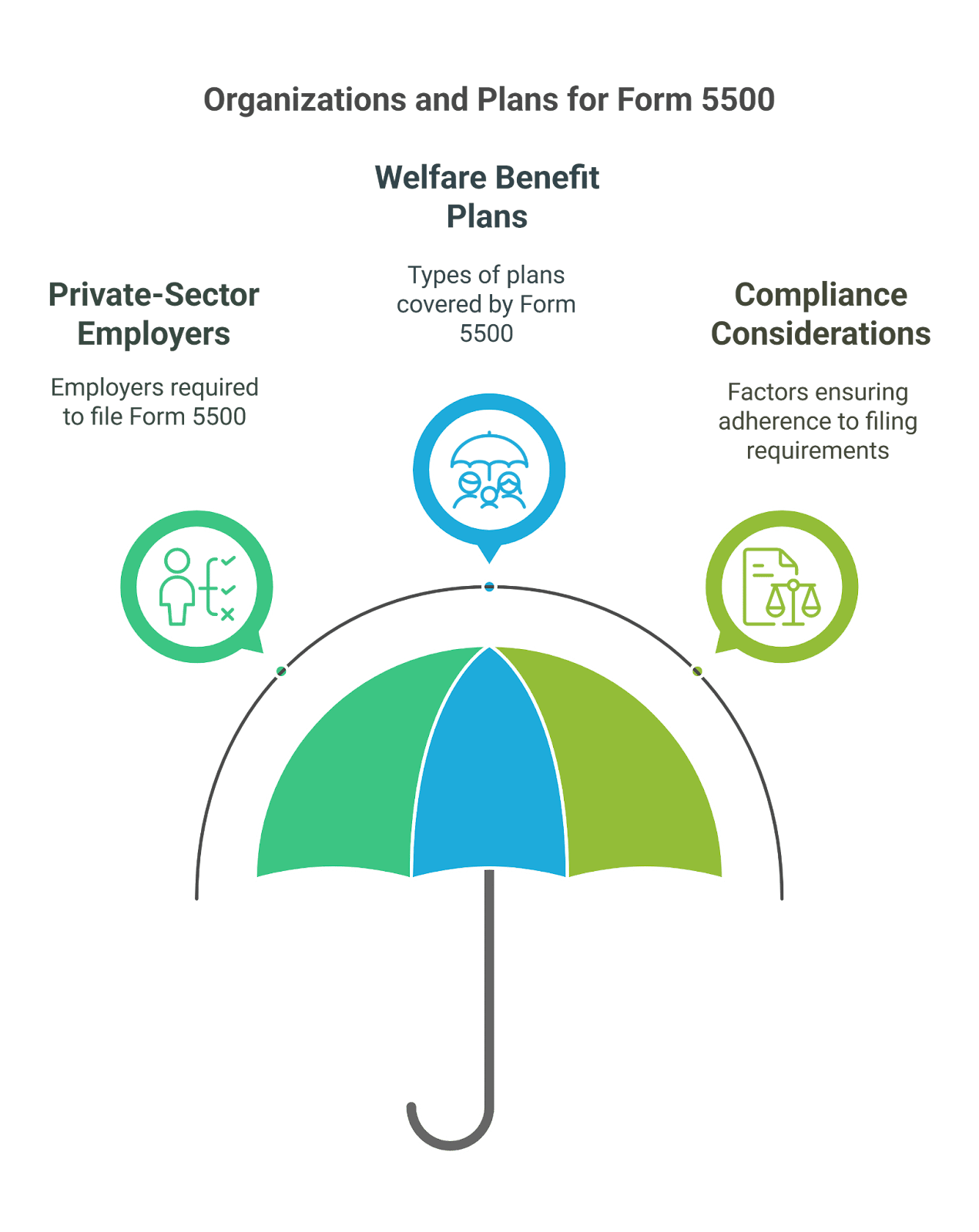

Types of Organizations Required to File Form 5500 for Health Insurance Plans

ERISA requires that private-sector employers who sponsor employee welfare benefit plans file Form 5500 annually. These welfare benefit plans encompass a range of health and welfare benefits, including:

- Medical insurance: Coverage for hospitalization, doctor visits, prescription drugs, and other medical services.

- Dental and vision insurance: Plans covering dental cleanings, orthodontics, eye exams, and prescription glasses or contact lenses.

- Life insurance: Provides financial protection to an employee’s beneficiaries in the event of their death.

- Disability plans: Short-term and long-term disability coverage for employees unable to work due to illness or injury.

The filing requirement applies to:

- Fully insured, self-funded, and mixed-funding plans.

- Private-sector employers offering employee benefits.

- Plans covering 100 or more participants.

- Multiple Employer Welfare Arrangements (MEWAs), which cover employees from multiple employers under a single plan.

To fully understand who must file Form 5500 for health insurance, employers need to determine whether their plans fall under ERISA’s reporting guidelines.

Organizations Exempt from Filing:

- Governmental plans (federal, state, or local government agencies).

- Church plans (as defined by ERISA) that provide benefits to employees of religious organizations.

- Top-hat plans (plans that exclusively cover a select group of management or highly compensated employees).

- Plans with fewer than 100 participants that are unfunded or fully insured (subject to specific conditions).

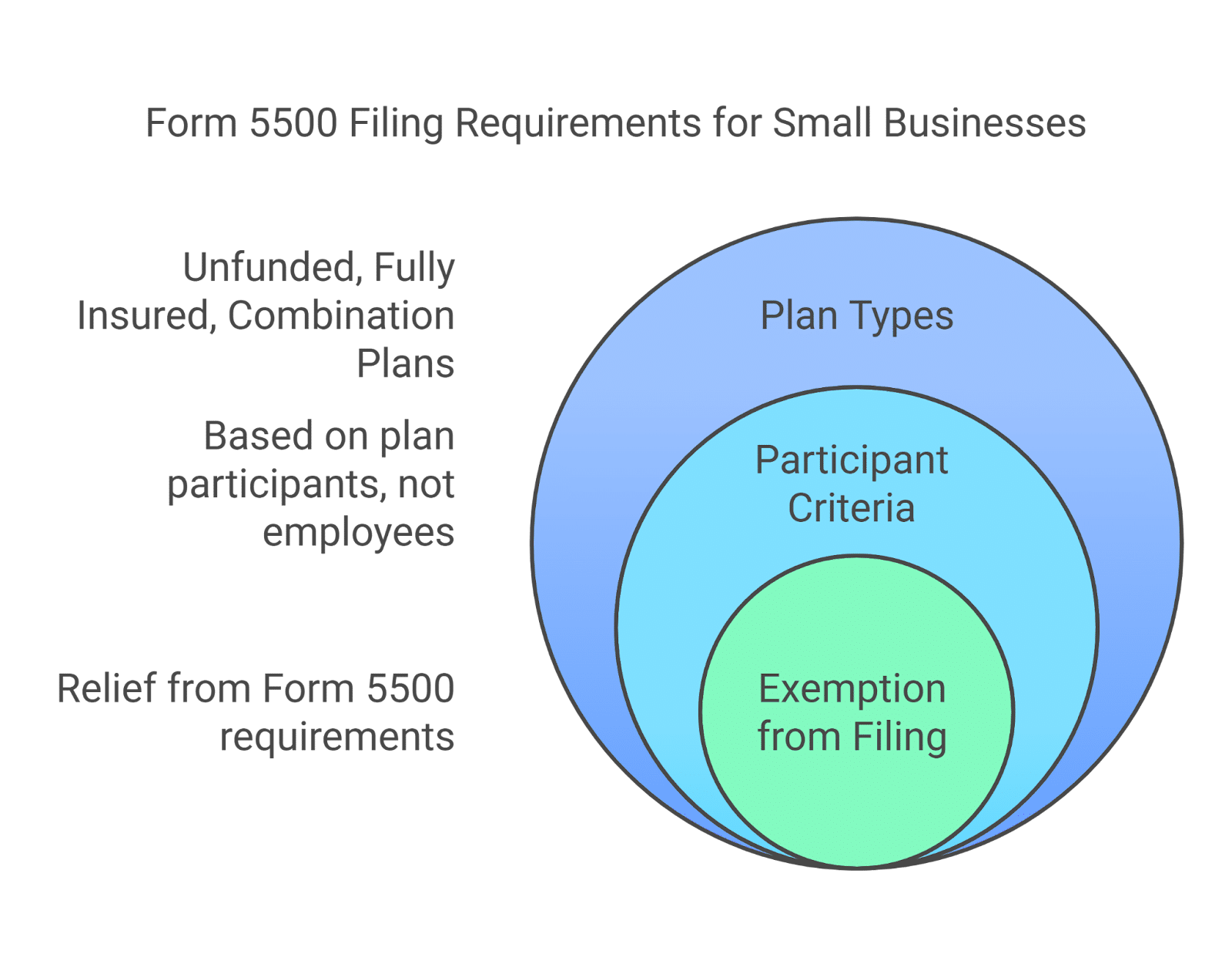

Are Small Businesses with Fewer Than 100 Employees Required to File Form 5500 for Health Insurance?

The requirement to file Form 5500 depends on the number of plan participants, not just the total number of employees. A participant includes:

- Current employees enrolled in the plan.

- Former employees are still covered under COBRA or retiree benefits.

- Beneficiaries receiving benefits under the plan.

Exemption for Small Businesses:

- If a welfare benefit plan has fewer than 100 participants at the beginning of the plan year and is unfunded, fully insured, or a combination of both, it may be exempt from filing Form 5500.

- Unfunded plans: Benefits are paid directly from the employer’s general assets without a separate trust.

- Fully insured plans: Benefits are provided exclusively through insurance contracts, with the insurance company assuming the risk.

- Combination plans: If a plan has both insured and unfunded components, it may still qualify for an exemption if no plan assets are held in trust.

Are Small Businesses with Fewer Than 100 Employees Required to File Form 5500 for Health Insurance?

The requirement to file Form 5500 depends on the number of plan participants, not just the total number of employees. A participant includes:

- Current employees enrolled in the plan.

- Former employees are still covered under COBRA or retiree benefits.

- Beneficiaries receiving benefits under the plan.

Exemption for Small Businesses:

- If a welfare benefit plan has fewer than 100 participants at the beginning of the plan year and is unfunded, fully insured, or a combination of both, it may be exempt from filing Form 5500.

- Unfunded plans: Benefits are paid directly from the employer’s general assets without a separate trust.

- Fully insured plans: Benefits are provided exclusively through insurance contracts, with the insurance company assuming the risk.

- Combination plans: If a plan has both insured and unfunded components, it may still qualify for an exemption if no plan assets are held in trust.

Understanding who must file Form 5500 for health insurance is especially important for small businesses evaluating their compliance requirements.

Exceptions:

- If the plan is funded through a trust or holds plan assets, the exemption may not apply even if the participant count is under 100.

- Employers should assess their specific plan funding arrangements and consult with a benefits advisor to determine their filing obligations.

Differences in Form 5500 Filing for Fully Insured vs. Self-Funded Health Insurance Plans

Fully Insured Plans

- Employers contract with an insurance company to provide health benefits.

- The insurance company assumes the financial risk of paying claims.

- Employers must file Form 5500 if the plan covers 100 or more participants.

- Must include Schedule A, which details:

- Premiums paid to the insurer.

- Commissions or fees paid to brokers or agents.

- Other insurance contract details related to coverage.

- Insurance companies typically provide this information to the plan sponsor.

Understanding who must file Form 5500 for health insurance is essential for companies offering fully insured plans.

Self-Funded Plans

- Employers assume the financial risk of providing health benefits directly.

- Instead of paying premiums to an insurer, the employer pays claims out of pocket.

- Must include Schedule H (Financial Information) if:

- The plan has 100 or more participants.

- The plan is funded through a trust.

- Schedule H requires detailed financial reporting of:

- Plan assets and liabilities.

- Income and expenses.

- Participant contributions (if applicable).

- If the plan is unfunded or insured and has fewer than 100 participants, it may be eligible to file Form 5500-SF (simplified filing version).

Employers must ensure they know who must file Form 5500 for health insurance, especially when considering funding arrangements.

Potential Penalties for Failing to File Form 5500

Employers must ensure timely filing to avoid penalties. The Department of Labor (DOL) can impose significant fines for late or missing filings:

- Up to $2,670 per day for failure to file.

- Delinquent Filer Voluntary Compliance Program (DFVCP) offers reduced penalties for voluntary disclosures.

- Employers should act promptly if they discover a filing omission to mitigate potential penalties.

- Late filings can also result in audits and increased scrutiny from regulatory agencies.

Knowing who must file Form 5500 for health insurance can help businesses avoid these penalties.

Who Must File Form 5500 for Health Insurance? How PEO4YOU Simplifies Compliance and Coverage Solutions

Employers need to understand the intricate requirements of Form 5500 filings to remain compliant and prevent expensive penalties. Who must file form 5500 for health insurance? It is essential to identify the entities required to submit Form 5500 for health insurance to meet all regulatory obligations.

Experienced intermediaries offer valuable assistance to businesses that need help managing their health insurance plans and meeting federal regulatory standards. PEO4YOU provides expert connections between clients and health insurance solutions designed to meet their unique requirements. Their services include:

- Helping businesses find the right healthcare coverage for employees.

- Acting as an intermediary between clients and health insurance companies.

- Ensuring compliance with ERISA and Form 5500 filing requirements.

- Providing customized benefits solutions to optimize employee offerings.

- Offering administrative support to reduce the burden of managing benefits and compliance.

By leveraging their expertise, PEO4YOU helps businesses navigate the complexities of healthcare offerings, ensuring that they not only provide comprehensive coverage to their employees but also remain compliant with all regulatory requirements. Their commitment to transparency, affordability, and dedicated support makes them a trusted partner for businesses aiming to optimize their health benefits while mitigating administrative burdens.