Small business owners who operate S Corporations (S Corps) need to know how health insurance payments work because it affects both their taxes and finances. Owners of S Corporations often ask whether their business can cover their health insurance costs. Health insurance payments from S Corps are permissible only when they conform to IRS regulations.

This guide examines the payment methods available to S Corp owners for health insurance, as well as the tax implications and potential deductions. This section will explain the different health coverage choices available for both S Corp owners and their employees.*

*This article is not meant as tax advice. Consult your CPA for tax advice.

Understanding Health Insurance for S Corp Owners

As a pass-through entity, an S Corporation allows its profits and losses to move directly onto shareholders' individual tax returns. Health insurance benefits provided by S Corps to employees are tax-free, but shareholders with more than 2% ownership face different rules.

Health Insurance Premiums for 2% Shareholder-Employees

The IRS requires S Corporations to include health and accident insurance premiums paid to 2% shareholder-employees in their wages for tax purposes. These health insurance premiums are exempt from FICA and Unemployment taxation under certain conditions.

The S Corporation handles payments for insurance premiums by paying the insurance provider directly.

An S Corporation can reimburse its shareholder-employee who paid medical premiums personally.

The premiums for a shareholder-employee should be reported in Form W-2, Box 1 under Wages, tips, other compensation, yet excluded from Boxes 3 and 5, which report Social Security and Medicare wages.

The reporting process enables shareholder-employees to deduct personal expenses on their tax returns.

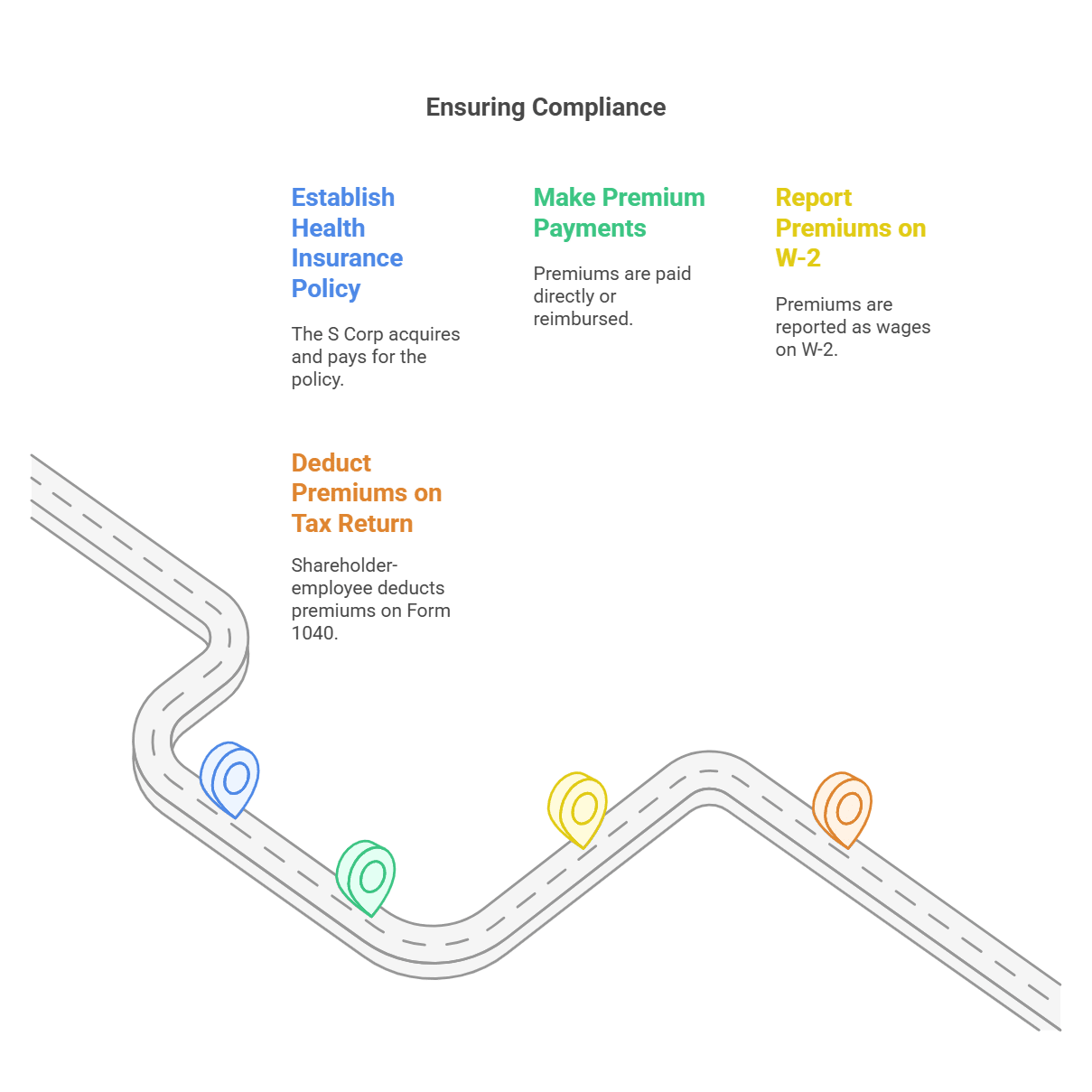

Steps to Ensure Compliance and Maximize Deductions

Follow these steps to allow your S Corp to cover your health insurance premiums while optimizing tax advantages.

1. Establish the Health Insurance Policy

The S Corp needs to establish the health insurance policy for its operations. This means:

The S Corp acquires the insurance policy under the business name and pays the premium costsor

Reimburse the shareholder-employee for premiums paid personally, provided the S Corp reports these premiums as wages on the shareholder-employee's Form W-2.

2. Make Premium Payments Through the S Corp

The business must either:

Send the insurance premiums straight to the provider, or

Compensate the shareholder-employee who pays them.

3. Report Premiums on Form W-2

Shareholder-employees must show their health insurance premiums as wages on their W-2 (Box 1).

This ensures compliance with IRS requirements.

4. Deduct the Health Insurance Premiums

Shareholder-employees can use their personal tax returns (Form 1040) to take a self-employed health insurance deduction according to IRC Section 162(l).

To qualify:

The shareholder-employee does not qualify for a self-employed health insurance deduction if they have access to a different employer-sponsored health plan, such as their spouse's employer-provided plan.

The permissible deduction is limited by the net income amount of the business.

When these requirements are fulfilled, the shareholder-employee may remove 100% of health insurance premiums from their personal taxable income, which diminishes their total tax liability.

S Corp Owners Can Explore Various Health Coverage Alternatives

Explore these alternative solutions if offering health insurance through your S Corp appears too complex.

1. Health Reimbursement Arrangements (HRAs)

Businesses use HRAs to provide employees with tax-free reimbursements for their medical costs.

HSAs benefit taxpayers who have high-deductible health plans.

Contributions to the account offer tax deductions, and qualified medical withdrawals remain tax-free.

S Corporation owners have the opportunity to participate in HSAs, unlike HRAs.

3. Taft Hartley Plans

Working with a Taft Hartley Plan enables companies to gain access to group health plans alongside additional employee benefits.

PEO4YOU provides small businesses with comprehensive health plans that comply with IRS rules while offering competitive rates.

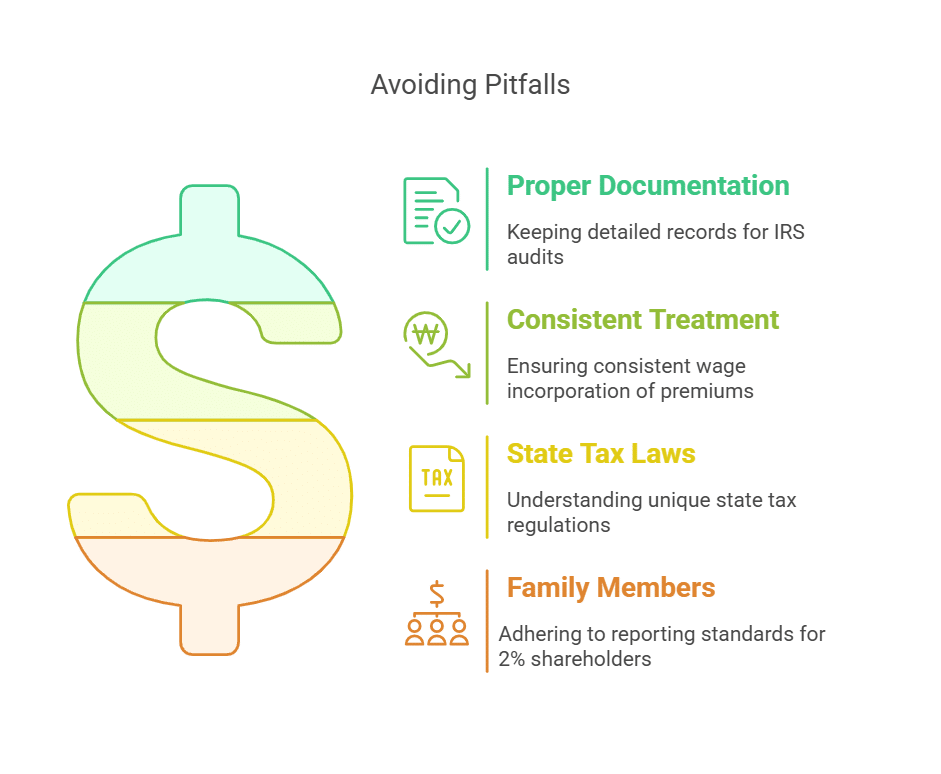

Common Pitfalls and Considerations

Be careful with these important considerations when arranging health insurance for an S Corp.

Proper Documentation: Keep detailed records of every premium payment and reimbursement to substantiate deductions during an IRS audit.

Consistent Treatment: Shareholder-employee wages must consistently incorporate premiums to prevent IRS complications.

State Tax Laws: Certain states impose unique tax regulations for health insurance deductions from S Corporations.

Family Members: The IRS considers family members employed by an S Corp who have an ownership stake of less than 2% to be 2% shareholders, requiring them to adhere to the same reporting standards.

Frequently Asked Questions

Can my S Corp pay for health insurance if I am the sole employee? Yes, under specific tax reporting conditions.

Does my S Corp need a formal health insurance plan? While not mandatory, the company must establish a policy.

Can I deduct S Corp-paid premiums if I qualify for my spouse’s employer-sponsored plan? No, shareholder eligibility for a spouse’s employer-sponsored health plan disqualifies them from deducting S Corp-paid premiums.

Can my S Corp provide group health insurance? An S Corp can offer group health insurance to all employees, including 2% shareholder-employees. However, for 2% shareholders, the premiums must be included in their wages for income tax purposes, though they are exempt from FICA and FUTA taxes.

Conclusion

Your S Corp has the capability to handle your health insurance costs, yet IRS rules mandate certain conditions.

The S Corp must establish the health insurance policy.

Premiums are included in W-2 wages.

Shareholder-employees are allowed to deduct health insurance premiums from their personal tax returns.

PEO4YOU serves as an ideal partner for small business owners who need assistance selecting health insurance options. their health insurance choices should turn toPEO4YOU to improve employee benefits at this moment.

March 1, 2026

PEO Honeymoon Rates: Spot Bait-and-Switch Pricing

Sam Newland

February 25, 2026

Medical Insurance Startup Strategies to Save Money and Keep Talent

Sam Newland

February 21, 2026

Best Dental Plans for Small Businesses That Keep Teams Smiling

Sam Newland

February 15, 2026

Blue Cross Blue Shield Employee Benefits for Small Businesses

Sam Newland

February 8, 2026

How Business Health Plus Helps You Offer Better Benefits

“We respect your privacy. Your contact information will be used solely for the purpose of responding to your inquiry and will not be shared with third parties.”

Click To Open Modal

Questions ?

Get In Touch We’re available 24/7

Floating Contact Form

Get In Touch—

We’re available 24/7

"*" indicates required fields

“We respect your privacy. Your contact information will be used solely for the purpose of responding to your inquiry and will not be shared with third parties.”

Question ?

Get In Touch We’re available 24/7

Floating Contact Form

Get In Touch—

We’re available 24/7

"*" indicates required fields

“We respect your privacy. Your contact information will be used solely for the purpose of responding to your inquiry and will not be shared with third parties.”

Thanks! We will be in touch soon. If you're looking to book a consultation now