You have 150-300 employees. You've been on ADP TotalSource for two or three years. The platform works, the payroll runs, but something feels off: your health insurance costs keep climbing, your dedicated HR contact changes every six months, and every benefit customization request disappears into a queue.

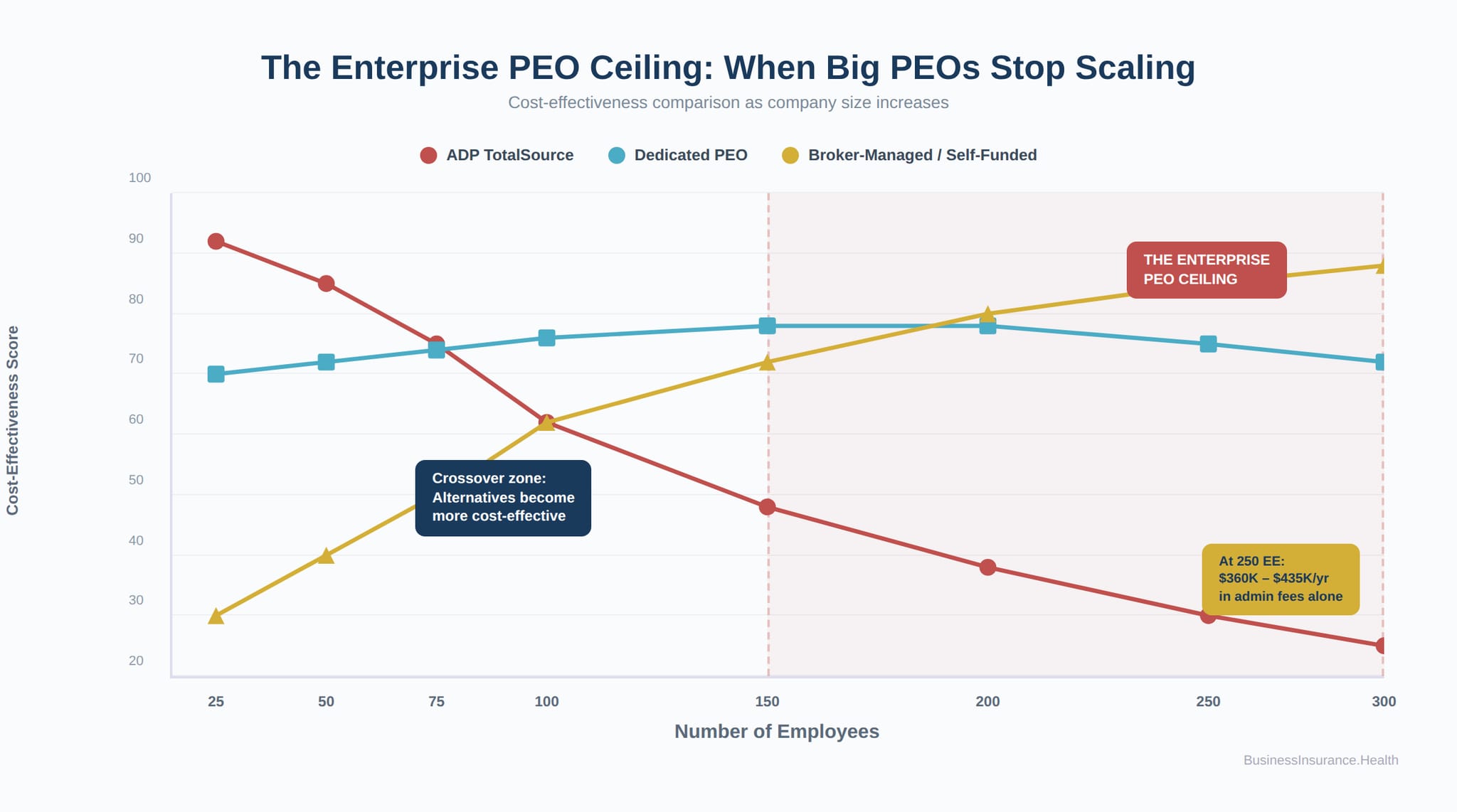

You're hitting what we call The Enterprise PEO Ceiling -- the point where a large PEO's standardized model stops fitting a mid-size employer's specific needs. At Business Insurance Health and PEO4YOU, we work with employers navigating this exact transition. The answer isn't always "leave your PEO." Sometimes it's "move to a different kind of PEO." And sometimes the right move is off the PEO model entirely.

In 2026, the employer health insurance market offers more alternatives than ever. The KFF 2024 survey found that average family premiums hit $26,993, up 6% year-over-year. For mid-size employers on ADP TotalSource, the question isn't whether you can find a better deal -- it's which alternative fits your company's trajectory.

ADP TotalSource is the largest PEO in the United States, serving over 700,000 worksite employees. Its scale is both its strength and its limitation. Here's what we consistently hear from mid-size employers at BIH:

Health plan options are limited. ADP TotalSource offers a curated set of health plans from select carriers. For a 20-person company, that's fine -- access to any carrier network is an upgrade from small group rates. But a 200-person company can negotiate directly with UHC, Aetna, Cigna, and BCBS for custom plan designs. The PEO's pre-built options become a constraint, not a benefit.

Admin fees don't decrease with scale. Whether you have 50 or 250 employees, the PEPM admin fee stays relatively flat. At 250 employees paying $120-$145 PEPM, that's $360,000-$435,000/year in admin fees -- more than enough to fund a dedicated HR team with broker-managed benefits.

Service quality varies. Large PEOs rotate account managers and HR contacts. Every rotation means re-explaining your company's culture, policies, and nuances. Dedicated-service PEOs and standalone brokers offer consistent personnel.

Transparency gaps. Many employers on ADP TotalSource don't know exactly what they're paying for health insurance vs. admin vs. workers' comp. The bundled billing model makes it harder to benchmark individual components. When we analyze ADP statements at BIH using the Benefits ROI Calculator, we frequently find 10-20% savings opportunities hidden in the bundled cost structure.

| Alternative | Best For | Savings Potential | Trade-Off |

|---|---|---|---|

| Dedicated PEO | 100-200 EE wanting PEO benefits with better service | 5-15% vs ADP | Smaller provider, less tech |

| Taft-Hartley Trust | 30-200+ EE in qualifying industries | 15-40% on health | Benefits only -- need separate HR/payroll |

| Level-Funded + HR | 50-150 EE with clean claims | 10-30% + surplus | More admin complexity |

| Broker-Managed | 150+ EE with HR capacity | Varies widely | Requires internal HR team |

| Self-Funded/Captive | 100+ EE with risk tolerance | 15-35% long-term | Claims volatility risk |

For employers evaluating option 2, see our Taft-Hartley health plan guide. For option 3, our level-funded insurance breakdown shows the math. For option 5, our captive insurance guide covers how employer-owned captives work.

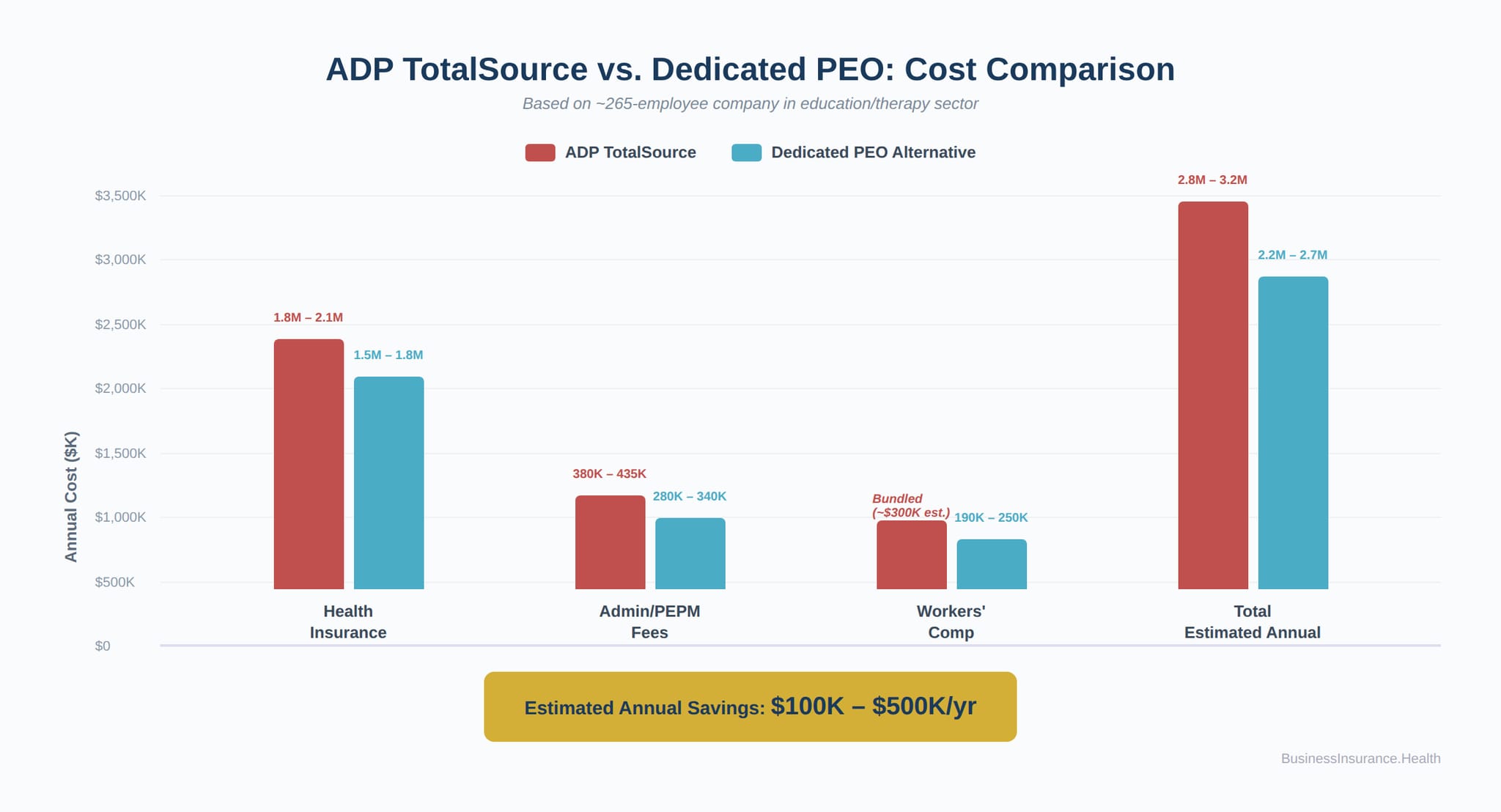

Here's an anonymized comparison from a BIH client in the education/therapy sector with approximately 200-300 employees:

| Cost Component | ADP TotalSource (Est.) | Dedicated PEO Alternative |

|---|---|---|

| Health insurance | $1,800,000-$2,100,000 | $1,500,000-$1,800,000 |

| Admin/PEPM fees | $380,000-$435,000 | $280,000-$340,000 |

| Workers' comp | Bundled (opaque) | $190,000-$250,000 (itemized) |

| Total estimated annual | $2,800,000-$3,200,000 | $2,200,000-$2,700,000 |

| Estimated annual savings | -- | $100,000-$500,000 |

BIH model estimate based on anonymized client scenario. Range reflects uncertainty in ADP bundled cost allocation and variation in alternative provider quotes. Actual savings depend on claims experience, carrier negotiations, and service-level requirements.

The key insight: even a modest 5-10% improvement in health insurance rates at this scale translates to $100,000-$200,000 -- enough to fund dedicated HR staff while still saving money overall. Use the BIH Premium Renewal Stress Test to model how different funding strategies would perform over your specific renewal horizon.

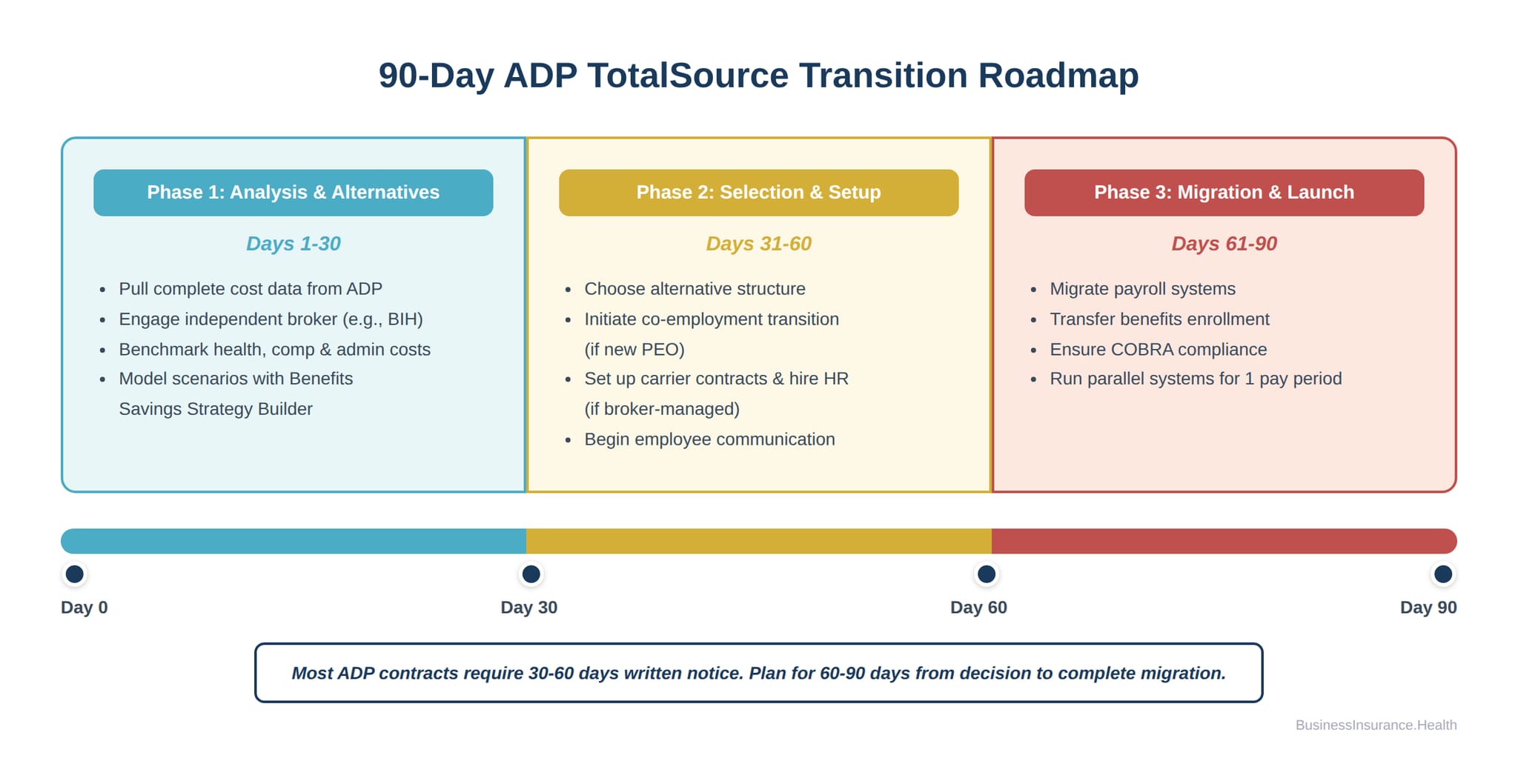

Days 1-30: Analysis and Alternatives. Pull your complete cost data from ADP. Engage an independent broker (like BIH) to benchmark your health, comp, and admin costs against alternatives. Model scenarios using the Benefits Savings Strategy Builder.

Days 30-60: Selection and Setup. Choose your alternative structure. If moving to a new PEO, initiate the co-employment transition. If moving to broker-managed, set up carrier contracts and hire or designate internal HR. Start employee communication.

Days 60-90: Migration and Launch. Migrate payroll, transfer benefits enrollment, ensure COBRA compliance for departing plan members, and run parallel systems for one pay period to verify accuracy. Most transitions go smoothly with 60-90 days of lead time.

For companies under 75 employees, ADP TotalSource often delivers strong value through pooled health insurance rates and integrated HR. For companies with 100-300+ employees, the value proposition weakens because you have enough scale to negotiate carrier rates directly and the admin fees become a significant line item -- potentially $300,000-$435,000/year that could fund dedicated HR staff.

All three are large-scale PEOs with similar strengths (technology, scale, carrier access) and similar limitations (standardized plan options, rotating account managers, opaque bundled billing). The differences tend to be in plan selection, geographic strength, and industry specialization. If your concern is the enterprise PEO model itself rather than ADP specifically, switching to Paychex or TriNet likely won't resolve the underlying issues.

Yes. Taft-Hartley multiemployer trusts are a health-benefits-only solution, so you'd need to arrange payroll and HR separately. But for employers where health insurance is the primary cost driver, Taft-Hartley savings of 15-40% can more than offset the cost of standalone payroll and HR. See our Taft-Hartley guide for eligibility details.

Dedicated-service PEOs -- smaller providers that specialize in specific industries or company sizes -- often deliver better service at lower cost for mid-size employers. BIH and PEO4YOU can benchmark your current ADP costs against dedicated alternatives to show the cost and service difference.

Plan for 60-90 days from decision to complete migration. The critical path items are carrier contract setup (if moving off PEO health plans), payroll migration, and employee benefit enrollment in the new arrangement. Most ADP contracts require 30-60 days written notice.

This analysis is provided for educational purposes and does not constitute financial or legal advice. Consult your compliance counsel and benefits advisor for guidance specific to your situation.

About the Author: Sam Newland, CFP®, has spent 13+ years in the employee benefits industry and founded Business Insurance Health and PEO4YOU to bring transparency to an industry that profits from complexity. His approach is simple: show employers the real numbers and let them decide.

Recent Posts

March 15, 2026

March 14, 2026

March 14, 2026

March 13, 2026

March 13, 2026

March 10, 2026

Get In Touch— We’re available 24/7

"*" indicates required fields

“We respect your privacy. Your contact information will be used solely for the purpose of responding to your inquiry and will not be shared with third parties.”

Click To Open Modal

Get In Touch— We’re available 24/7

"*" indicates required fields

“We respect your privacy. Your contact information will be used solely for the purpose of responding to your inquiry and will not be shared with third parties.”

Thanks!

We will be in touch soon.

If you're looking to book a consultation now

Affordable health and benefits plans for small businesses, freelancers, and independent contractors.

Copyright © 2026. Peo4you. All rights reserved.