PEO4YOU is a Taft Hartley plan. Taft Hartley plans pull businesses and sole proprietors together in order to improve rates through shared risk pooling. The money people pay for their health coverage goes into a trust and is regulated by ERISA laws. This requires that money in the fund only go out for medical claims and administration - not for executive profits. The main advantage of this plan is its premium stability where every business gets the same premium increases whether they are healthy or sick. Many clients report smoother claims administration and an enhanced customer service experience. Some clients have saved over 50% on their health premiums.

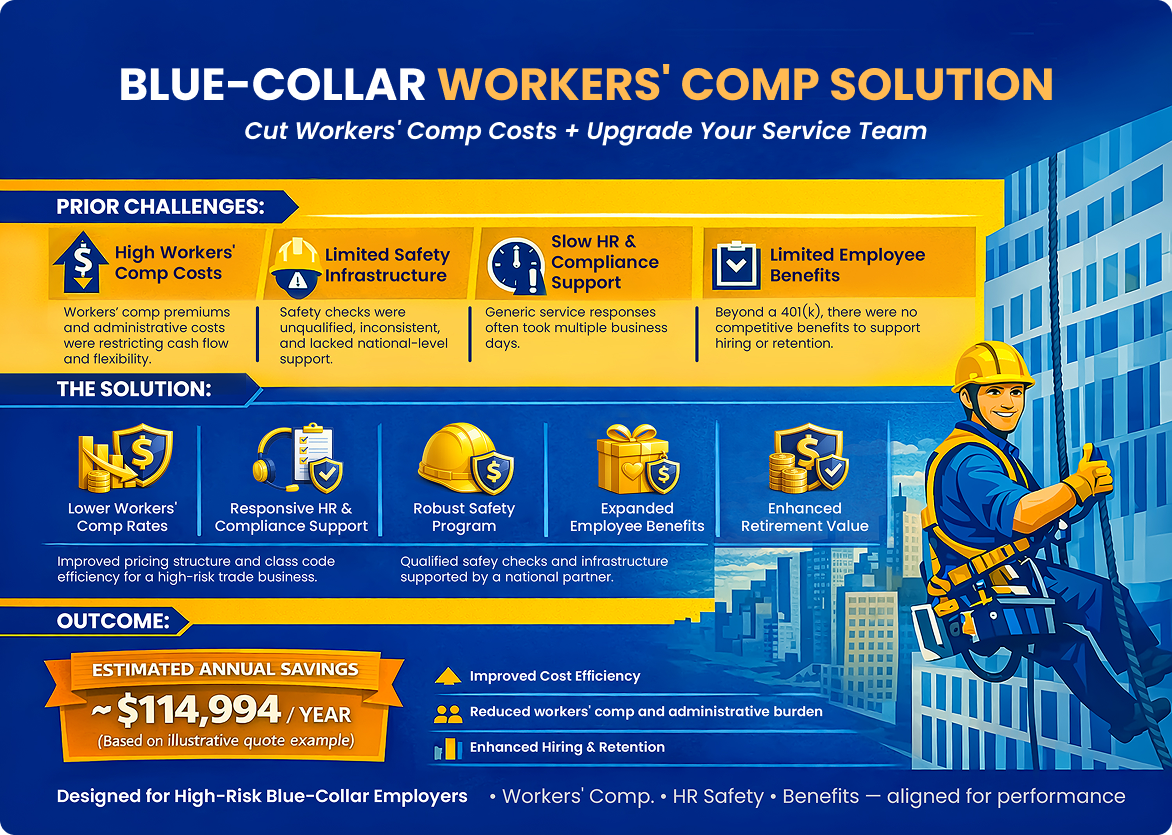

PEOs are a total business solution that help assist in 5 areas - payroll, HR, compliance, employee benefits, and (sometimes) workers’ compensation - which typically helps them outcompete comparable businesses not in a PEO. Due to their structure, they provide unmatched compliance risk management that cannot be duplicated outside of a PEO. For many businesses, they also provide unbeatable health rates and voluntary Fortune 500 employee benefits options without enrollment and participation requirements. Our recommended PEO partners all have client retention rates between 91.8-95% and do not interfere with how ownership wants to run their business. Some clients have saved as much as 52% on their medical through PEOs

Over the last decade, the popularity of self-funded plans has grown significantly as fully insured rates have skyrocketed. For businesses considered small groups, self funded options allow businesses to be rewarded with lower health-based rates that tend to be lower than fully-insured options. What makes these plans so effective is their customizability. Employers can choose their own TPA, pharmacy benefit manager, specialty med carveouts, direct primary care, etc. This level of customization can slash annual premiums with typical savings of 10-30%. 50% of employers with 20+ employees enrolled can expect savings of at least 25%.

For small groups, fully insured options are based simply on zip code and date of birth. As a result of not being able to determine rates in any other way, the carrier has to assume below average health. This tends to make fully insured advantageous for unhealthy groups. For large groups (ie 50+ FTEs), rates are still health-based. That said, unlike self funded plans, claims data tends to be not shared at all or highly delayed. The advantage for large groups is that the network and claims administrator are the same.